- Quick take

- 21 February 2024

- Indonesia

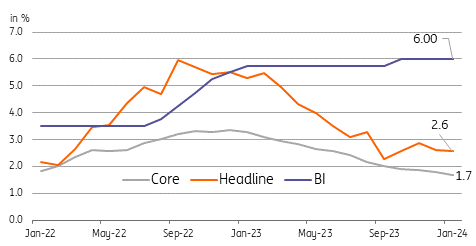

Bank Indonesia stays on hold but points to easing by second half

Indonesia's central bank kept policy settings untouched today but gave clear signals it was open to easing before the end of the year

| 6.0% |

BI policy rate |

| As expected | |

BI extends pause in February

Bank Indonesia (BI) kept policy settings unchanged, a move widely anticipated by market participants. The central bank expects global growth to be resilient in 2024, driven by the US and India, while also staying upbeat on domestic growth prospects.

BI forecasts Indonesia’s GDP growth to settle between 4.7-5.4% year-on-year this year, maintaining its previous forecast. BI also indicated that it was bracing for a current account deficit this year with the shortfall expected to hover around 0.1-0.9% of GDP.

BI shared that today’s decision to pause was in line with its focus on delivering stability, especially for the FX market. Keeping rates at 6% would help support the rupiah and, in turn, limit imported inflation pressures.

And although inflation has remained relatively stable of late, BI had recently shifted to a slightly lower inflation target of 1.5-3.5% (down from 2-4%), which could explain the extra caution BI is exercising in retaining policy rates today.

BI on hold today but gave clear signals that rate cuts would be carried out before end of year

BI on hold for now, cuts to follow

Despite reiterating that the central bank would retain its current stance for the time being, BI Governor Perry Warjiyo shared that he does remain open to cutting policy rates sometime in the second half of the year.

Meanwhile, it also appears that the BI would prefer to let the Federal Reserve begin its rate cut cycle first, before following with a set of its own rate reductions.

With BI expecting the Fed to cut by roughly 75bp in the second half of the year, we expect BI to follow shortly after and reduce its own policy rate by roughly the same magnitude.

We believe any rate cut by BI will remain contingent on both the Fed initially cutting policy rates and the Indonesian rupiah managing to maintain some level of stability. If we get both, we believe BI can begin to move into easing mode and deliver an added push to growth momentum.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more