- Quick take

- 15 December 2021

- Australia

Australian employment surges on reopening

The end to lockdowns in Australia allowed 366,100 jobs to be created in November and the unemployment rate to fall to 4.6%. This will put a strain on the central bank's continued dovish message, though the market is arguably still pricing in too much tightening too soon

| 366,100 |

Job gainsNovember |

| Higher than expected | |

This shows the damage lockdowns do

Of the 336,100 job gains in November, which followed a decline of 46,300 in October, 237,800 were part-time. Only 128,300 were full-time.

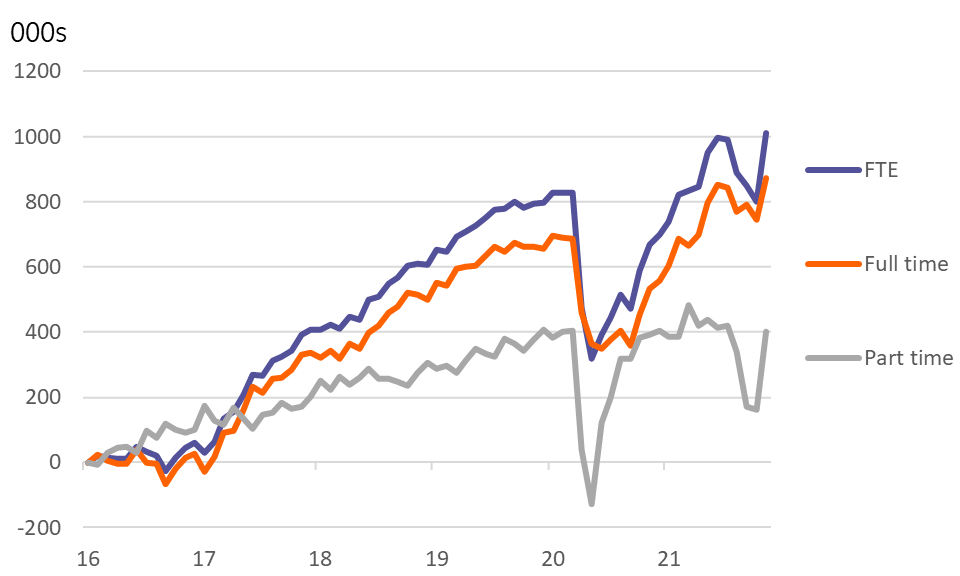

The chart below shows the cumulative change in jobs between part-time, full-time and our own measure of full-time equivalents (3 p/t = 1 f/t). What it shows is that even with the gains heavily concentrated in part-time jobs, full-time jobs have clawed their way back above their level prior to the latest lockdowns. Full-time equivalent jobs have done likewise.

Part-time jobs, which due to their lower hours will typically pay less and may also be less well remunerated on an hourly basis, are typically the first jobs to respond in a downturn or an upturn. We look for further, though smaller gains in aggregate job gains in the December figures. We also expect part-time jobs to be converted to full-time jobs, causing a reversal of the dominance of part-time jobs seen in November.

Cumulative Australian employment change (000s)

Unemployment rate drops to 4.6%

The drop in the unemployment rate to 4.6% takes it back to the level it was at in September though the unemployment rate still remains a little higher than the recent July trough of 4.5%. The latest decline in the unemployment rate comes despite a healthy rise in the labour participation rate (to 66.1% from 64.6% in October). We might have expected the return from lockdown to push the unemployment rate higher, as many of those not regarded as being in the labour force during lockdowns (the unemployed are required to be actively looking for work to be counted as such) would have returned, but may not have found work immediately. The fact that this did not happen (the numbers of unemployed actually fell sharply from 359,000 to 331,100) suggests that the underlying economy is really in pretty good shape and was able to readily absorb the influx of new job seekers. The dominance of part-time jobs may have helped here, though it may also point to strong gains in leisure and hospitality which will have been unduly hit during lockdowns.

The chart below also shows that much of the recovery in jobs growth occurred outside the major urban conurbations, which also suggests that there is still some healthy room for further gains in December. This should also set the scene for some further declines in the unemployment rate.

Cumulative employment by state (Index Dec 2016 = 0)

Whither wages?

One ingredient missing from today's labour market release is any indication of wages growth. Wages are a critical metric for the Reserve Bank of Australia (RBA), which has argued that it will take a long time before the unemployment rate falls sufficiently to merit any policy normalisation.

We will need to wait until 23 February for the 4Q21 wage-price index to be released. Wages growth was only 2.2% year-on-year, according to the 3Q21 figure. If wages growth continues at the same quarter-on-quarter pace in 4Q as in 3Q21, then this will take annual wage inflation for 4Q21 to 2.6% YoY. It's not clear if this is "materially higher" than the current rate - which is the hurdle the RBA has been using for policy tightening. Our guess is that they will want to see wages growth closer to or even above 3% to argue that there is any need to start unwinding their current monetary settings - though some further tweaks to the asset purchase scheme could occur well before rates begin to move.

In the meantime, financial markets continue to price in much more rapid tightening than the RBA is suggesting. Before this data was released, the 3m yield implied by bank bill futures was just over 1% at the end of 2022. This increased to 1.13% following this release. By comparison, the central scenario from the RBA still implies no rate hikes at all in 2022.

If the RBA's rhetoric is currently too dovish compared to the recent run of data, the market also seems to have got ahead of itself. Some convergence by both the RBA and markets towards the middle ground seems the most likely direction of travel in 2022. We are currently forecasting the first hike from the RBA in 1Q23, though we will review this in the New Year for a possible 4Q22 liftoff - also taking into account the US Federal Reserve's recent shift. Omicron risks are one factor why we are not rushing to change anything just yet.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more