- Quick take

Australia: Rate hike forecast is hanging by a thread

- 30 August 2023

- Australia

The headline inflation rate has now fallen below 5% which will encourage thoughts that the RBA tightening cycle has peaked - though progress over the next few months will be harder. Our final 25bp rate hike call for 4Q23 is hanging by a thread

| 4.9% |

July CPI inflationYoY% |

| Lower than expected | |

This was much lower than expected

We were not expecting Australian inflation to fall markedly this month. Large electricity tariff hikes were going to be part of today's figures, and incorporating these into our forecasts, it looked more likely that inflation would at best fall only a little, or more likely, would remain roughly unchanged with an outside chance that it actually rose a bit.

So the fall in inflation to 4.9% YoY in July from 5.4% was a shock, albeit a welcome one.

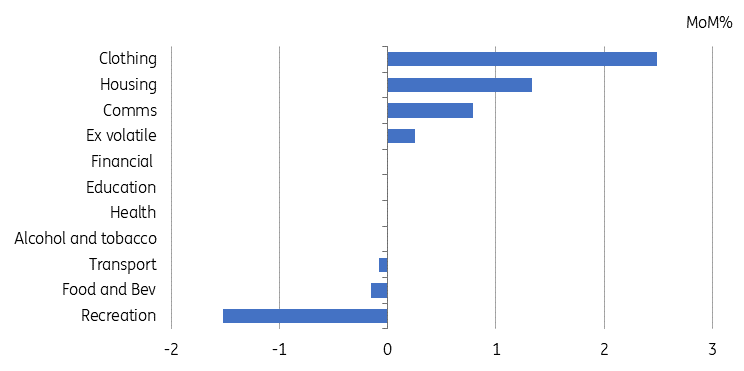

We did see the housing component rise by 1.3% over the previous month, up from 0.3% MoM in June, and this will have been where the electricity tariff increases will be evident. But declines in food and beverage prices as well as holidays (part of the recreation subindex) look to have offset all of that and more, and there was a large rump of the CPI basket, especially on the service side (education, health, finance) where prices apparently did not move at all in July, which will have helped pull the average for the whole basket down.

Australian CPI MoM% change by component

Progress over the coming months may be slow

From a month ago, the CPI index rose only 0.25%, which if maintained over the medium term, would bring the inflation rate back within the RBA's 2-3% target range over the coming 12 months. But month-on-month increases really do need to stay down at these sorts of rates or lower, since base effects, including this month (last year's July CPI index rose 0.7%MoM) have been doing a lot of the hard work in bringing inflation down recently.

Over the next three months, the corresponding 2022 monthly increases were all 0.3%, so if July's CPI increase is maintained for the next three months, we will see inflation falling only by a further 0.1-0.2pp. Any upside deviation from this, and inflation may start to edge higher again, and for that reason alone, we are holding on to the final 25bp rate hike in 4Q23, but we admit, we are a lot less comfortable with this view than we were yesterday.

A final rate hike for the RBA looks more doubtful

If, in addition to a decent run of inflation date over the next month, we also see some corroboration from the real economy, for example, a repeat of last month's softer labour market data, then we will almost certainly trim out the final cut. At that point, the question will change to consideration of when and how the RBA might begin to row back from its current restrictive setting. Will this be a modest reduction to take policy rates back to a more neutral setting in the face of a fairly soft landing, or will it be cutting more aggressively to shore up a more rapidly slowing economy?

In truth, we don't know the answer to this. Our expectation is for the former scenario, but there are a great many moving parts to this, including how the external environment (China and the United States in particular) shape up. And we won't be ruling out more downbeat scenarios until we have much more evidence to support the soft-lending hypothesis.

The AUD quickly shrugged off the weaker inflation print. Broader USD trends will probably be more important in the coming months for the AUD than any marginal changes to RBA policy expectations.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more