- Quick take

- 15 June 2021

- Australia

Australia: Main policy decisions pushed out until July RBA meeting

The minutes of the 1 June RBA meeting showed as expected, Australia's Central Bank in a holding pattern as it awaits more data on the labour market, wages and inflation - no hints about any imminent changes in their stance.

Considerations for monetary policy

The meat of any central bank minutes usually comes at the end, with the "Considerations for monetary policy" section. That is certainly true for the RBA minutes, so we will start with that section before moving back to see what else is noteworthy.

And the main conclusion expressed in the latest policy-relevant section of these minutes was to push all of the important decisions back to the July meeting, where the RBA board would consider:

- "...whether to retain the April 2024 bond as the target bond or extend the target to the next maturity, the November 2024 bond" and also;

- "...the Board would decide upon future government bond purchases at the July meeting ahead of the completion of the second $100 billion of purchases in early September 2021".

The options for the bond purchase program were outlined as:

- "Ceasing purchasing bonds in September (other than to support the yield target if necessary)" - thought likely to be premature - so we can probably rule this one out..

- "Repeating $100 billion of purchases for another 6 months";

- "Scaling back the amount purchased or spreading the purchases over a longer period" and;

- "Moving to an approach where the pace of the bond purchases is reviewed more frequently, based on the flow of data and the economic outlook" (this sounds pragmatic, but has the disadvantage of being fiddly - central banks usually like simplicity and transparency).

By a process of elimination, we favour a version of 3), with either a smaller amount purchased over the next 6 months or spreading the same amount over 12m, which amounts to much the same thing if the smaller amount in the first 6 months is then extended a further 6m.

International and domestic economic developments

The international and domestic sections are usually a re-hash of things you already knew, so can often be glossed over. The only caveat to that this time being that in the international section, there are a couple of references to how Australia fitted in with the general global pattern.

Most notably in the latest minutes from the 1 June meeting:

- "...in most advanced economies, including Australia, spare capacity in labour markets was likely to contain underlying inflationary pressures for some time", which reinforces subsequent discussion about the monetary policy decision and the importance of seeing wage growth pick up to 3% sustainably, and;

- "The Australian economy was continuing to benefit from higher commodity prices and strong demand for resource exports, despite ongoing difficulties in the trading relationship with China. Members noted that the terms of trade were likely to be near record levels in the June quarter and remain high in the near term".

This last statement about terms of trade is one that would be consistent with maintained AUD strength and could indicate that the RBA is fairly relaxed with the current level of the exchange rate and could probably tolerate some limited appreciation.

The statement also makes the upbeat observation that the economy was "transitioning from recovery to expansion with more momentum than previously anticipated", though this is tempered by noting a number of uncertainties - the pandemic backdrop, the household spending/saving decision, and the effective stimulus from policy measures, to name a few.

Housing and labour markert

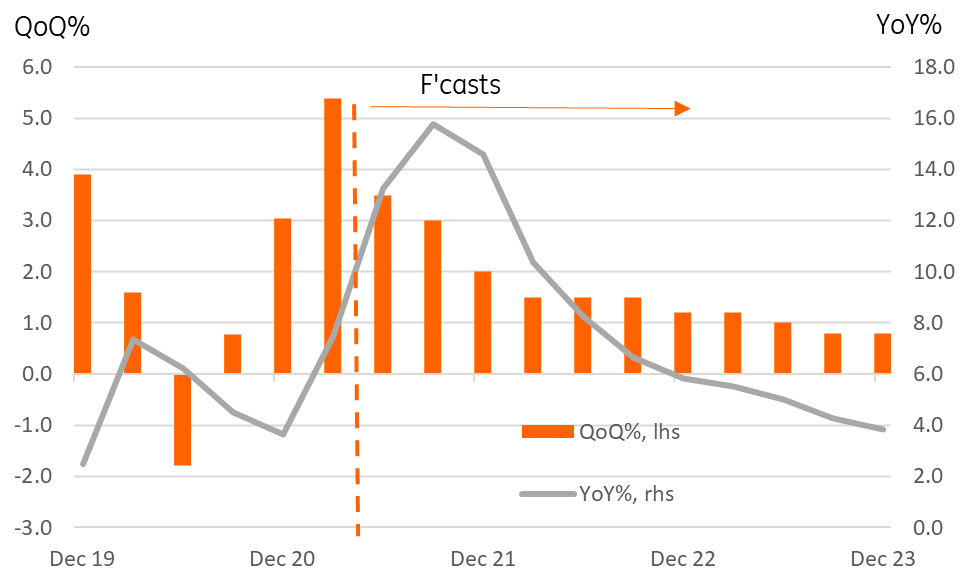

The domestic section of the discussion did give up a fair bit of space to the housing market, though was quite nuanced, noting some weaknesses in local rental markets despite the overall strength of this sector. New data out on house prices released today showed further acceleration, with a 5.4% QoQ increase taking the year on year rate to 7.5%.

Even with some moderation of quarterly house price increases in the coming quarters, house price inflation looks set to push well into double figures over the coming two quarters before it begins to ease lower again. So we will have to determine whether the RBA will view this as a "transitory increase" which in the current vogue of central bank terminology simply means a price increase that it can ignore.

On the labour market, on which the RBA puts considerable weight for their policy decisions, the main contention seemed to be that although labour shortages were appearing in some sectors and locations, there was still a substantial pool of untapped resources which should prevent wage pressure from rising substantially in the near future. The minutes further noted that there was not yet much evidence that any shortages were in fact leading to wage increases. Though this will certainly need watching as any change here could be pivotal to policy decisions.

Residential property prices (8-city weighted average)

Domestic financial markets

In terms of the domestic financial situation in Australia, perhaps the most interesting addition was the discussion about climate change, with members of the board noting "particular taxonomies could become very influential in global financial markets, and these will have an important bearing on the cost and availability of financing the transition to lower carbon emissions for Australia".

We are likely to hear more about this in the coming quarters. Other major central banks are putting sustainability at the centre of monetary policy and the RBA is unlikely to choose a different path.

But to re-iterate - on balance, this meeting was merely a preamble to the July meeting, which will bear far closer scrutiny.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more