April’s rebound in Polish production offsets dismal March reading

We opted not to revise our Polish economic growth forecast for 2024 down after a dismal industrial reading in March – which has proved to be the right decision. April brought a bounceback and confirmed that an industrial recovery is underway, even if not impressive. We still see Poland’s economy expanding by 3% this year

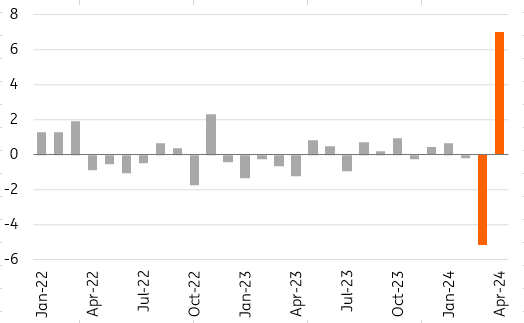

Industrial output rebounded in April after weakness seen in March

Polish industrial production rose by 7.9% year-on-year in April (ING: 6.2%, consensus: 5.6%), following a 5.6% YoY decline (revised) in March. Seasonally adjusted data shows a 7.0% month-on-month increase in production, meaning that manufacturing has recovered from the March decline. Averaging over the last two months indicates that the recovery in manufacturing is progressing. Alternative data also indicates that the rebound has continued and the exceptional weakness seen in March was a one-off.

The high volatility of industrial production data in March and April was due to calendar effects. The weak performance in March was a consequence of two fewer working days and an early Easter. In contrast, April this year had two more days than the year before, which boosted industry data.

In April, production growth was recorded in the vast majority of industrial divisions (31 out of 34), with declines occurring in the manufacture of electrical equipment, mining and metal production. There was solid growth in the production of consumer goods, both durable (12.9% YoY) and non-durable (9.9% YoY). This allows us to be more optimistic about the outlook for consumption, where we expect to see a steady improvement. The production of capital goods grew at slightly slower pace (7.6% YoY).

High volatility in industrial output data induced by calendar effects in recent months

Industrial output, MoM SA

PPI deflation to ease in the coming months

Producers’ prices remain in deep deflation. In April, the PPI index fell by 8.6% YoY (ING: -8.2%, consensus: -8.3%), following a decline of 9.9% YoY (revised from -9.6%). Compared to March, producer prices rose by 0.2%, mainly driven by higher prices in mining (+4.2% MoM), while price levels were broadly stable in other areas. The main part of the downward adjustment in the level of producer prices is probably behind us. The following months will bring a gradual reduction in annual deflation, and by 2024/25, we should already see an increase in PPI on an annual basis.

Our outlook

Given the high volatility of production due to calendar effects, the state of the economy is easier to assess by looking at the last two months together. The picture that emerges from the March and April data suggests that the recovery continued in the first and second quarters of this year, but at a moderate pace. The performance of domestic manufacturing is overshadowed by the problems of the German economy, which is under increasing competitive pressure from other countries.

Despite the unfavourable external environment, we remain optimistic on Poland's economic recovery. We refrained from downward revisions of annual GDP forecasts after the weakness seen in March, and April's rebound confirmed that the economy is on the recovery track. Real disposable income growth (at a pace not seen in more than two decades) should be the main driving force behind consumption in 2024. In our view, the rebound is very likely to be driven by a recovery in domestic demand rather than an improvement in foreign trade, as the cyclical improvement in Germany is there but is slower than in other eurozone economies.

Despite the strong zloty, weak external demand and decelerating public investment, we project GDP growth to amount to 3% this year and accelerate in 2025 thanks to stronger investment activity.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap