- Quick take

Turkey: Primary balance improves in September

- 15 October 2018

- Turkey

The budget balance showed some improvement last month on an annual basis, with strong non-tax revenue generation despite a large expansion in both primary and interest expenditures

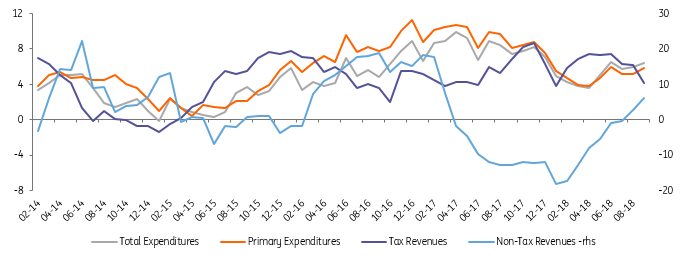

Evolution of revenues and expenses

(12M rolling, CPI Adj., YoY Growth, %)

In September, the central administration budget balance recorded a TRY-6.0 billion deficit, down from the same month of last year at TRY-6.4 billion. The monthly outcome shows strong revenues from non-tax items while primary spending maintained a strong growth rate, at 23.6% YoY (though slightly negative in real terms at -0.8%), and a 21.6% YoY increase (-2.3% real change) in interest expenditures on the back of an uptrend in yields. Accordingly, the primary surplus more than doubled to TRY+4.3 billion from TRY+2.0 billion.

The breakdown

- The impact of inflation should mean a roughly 20% or more increase in major budget items.

- The pace of real increase in tax revenues has lost momentum, turning negative at -5.5% in September vs 4.4% on a YtD basis, likely showing the impact of a deterioration in economic activity. Two other points also worth noting are the contraction in Special Consumption Tax income on petroleum & natural gas (reflecting the government’s decision to absorb some of the price shock from the weak currency and oil price spike via an automatic tax adjustment on gasoline prices) and plunge in VAT on imports (in dollar terms) following an ongoing contraction in import demand.

- On the revenue side, we also see a sharp recovery in non-tax revenues this year. This is due to a number of factors, for example, higher profit transfers from the Turkish central bank. In September, income from interest and fines almost tripled because of unexplained parts of this item (“other miscellaneous revenues”).

- On the expenditures side, capital expenditures and capital transfers saw a real increase of more than 20% in September and the first nine months of the year compared to the respective periods of 2017. However, larger shares in primary spending, personnel expenditures and current transfers have been the major drivers of growth on a monthly and cumulative basis.

Following fiscal easing since mid-2016, which has continued to be be evident in this year’s budget metrics, the medium term programme (MTP)- a key policy action from the government- anticipates strong fiscal performance and a return to fiscal discipline next year. Accordingly, the MTP shows the central administration budget balance-to-GDP ratio remaining under control and the size of the primary surplus-to-GDP is expected to gradually improve and return to pre-2016 levels in 2021.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more