March Economic Update: In like a lion, out like a lamb?

A deal between the US and China appears close, which could see markets rethink their ultra-cautious expectations on US central bank policy. Concerns about global growth could start to fade too. But a handful of stumbling blocks could yet scupper a deal. Meanwhile, the threat of a ‘no deal’ Brexit, and tariffs on EU cars, means uncertainty will remain high

March is shaping up to be a big month for geopolitics. A deal between the US and China appear close, which could see financial markets rethink their ultra-cautious expectations on US central bank policy. Concerns about global growth could start to fade too. That said, a handful of stumbling blocks could yet supper a US-China deal. Meanwhile, the threat of a ‘no deal’ Brexit, and tariffs on EU cars, mean the uncertainty facing policymakers and investors will remain high.

The Federal Reserve has adopted a more cautious approach to monetary policy since the start of the year. Trade tensions, the turmoil in equity markets and tighter financial conditions are cited as 'cross-currents' that are creating uncertainty, and in an environment of low inflation, the Fed can afford to be 'patient'.

However, these tensions appear to be easing. Borrowing costs have fallen back, equities have recovered all their losses, and there are positive signs regarding a potential US-China trade deal. With the jobs market roaring ahead, higher pay and rising inflation pressures mean that there is a strong case for a summer interest rate rise. This remains at odds with financial markets, which are pricing in a prolonged pause with an eventual rate cut in 2021.

Sentiment indicators have begun to stabilise in the eurozone having continuously declined since the start of 2018. However, any rebound looks to remain muted as a trade war with the US and a chaotic Brexit remain significant risks, keeping uncertainty high. What’s more, core inflation has fallen back below 1%, nipping any expectation of monetary tightening in the bud. In fact, the ECB has now extended its forward guidance of stable rates up to the end of 2019 and has also announced a new series of TLTROs to avoid a tightening in credit conditions.

The UK Prime Minister faces an uphill struggle to get her deal approved by Parliament, despite hints that her opponents may be shifting their position. That means an extension to the Article 50 negotiating period now looks inevitable, but if this delay is kept relatively short, the threat of ‘no deal’ will remain. That will keep the pressure on the economy, further reducing the chances of a rate hike this year.

China’s government has provided a set of targets for 2019. Almost everything was as expected, especially the new GDP growth target. The government is relying a lot more on fiscal stimulus rather than monetary easing. A repeat of previous guidance on the exchange rate mechanism may mean the yuan will continue to follow the dollar index.

The 10-year German yield at a mere c.20 basis points bears no reflection on the Germany economy. So how can we make sense of this? To keep it plain and simple, it is a measure of fear. That fear is a combination of two elements. First, there is the ‘macro’ fear that the current slowdown could become more severe. But by far the most significant element is an existential fear about the European project itself, and not enough attention is being paid to this. The EU elections in May could prove pivotal.

In FX, we continue to look for further USD outperformance vs the low yielding G10 currencies in coming months. The Fed will deliver a hike, while the likes of ECB or BoJ will remain dovish /neutral. The duration of the Article 50 extension will matter for GBP price action, with longer extension being more positive for GBP than shorter. In the CEE FX space, our top pick remains HUF.

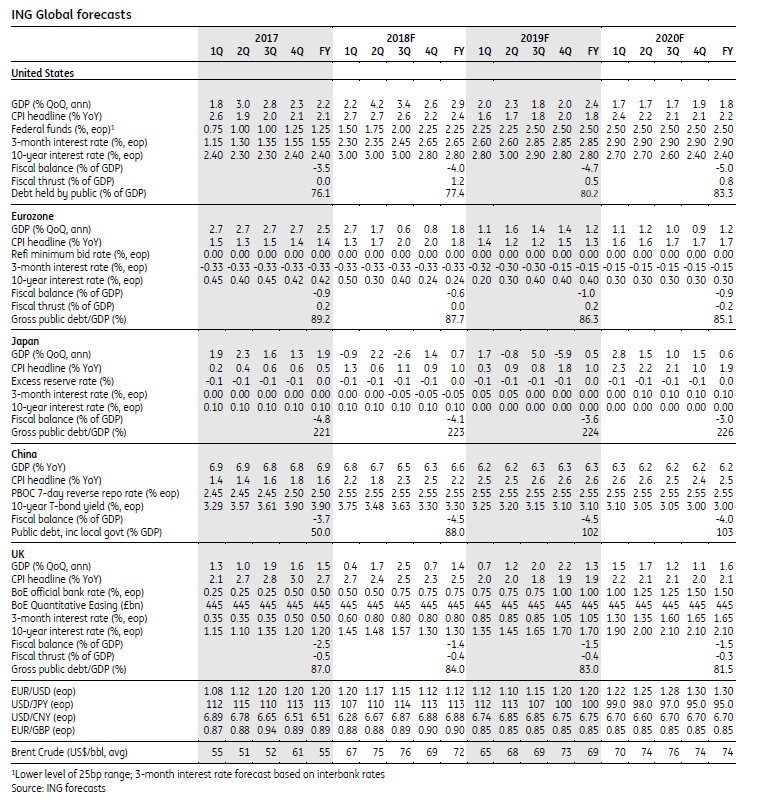

ING Global forecasts

Tags

March Monthly UpdateDownload

Download report

8 March 2019

March Economic Update: In like a lion, out like a lamb? This bundle contains 9 Articles"THINK Outside" is a collection of specially commissioned content from third-party sources, such as economic think-tanks and academic institutions, that ING deems reliable and from non-research departments within ING. ING Bank N.V. ("ING") uses these sources to expand the range of opinions you can find on the THINK website. Some of these sources are not the property of or managed by ING, and therefore ING cannot always guarantee the correctness, completeness, actuality and quality of such sources, nor the availability at any given time of the data and information provided, and ING cannot accept any liability in this respect, insofar as this is permissible pursuant to the applicable laws and regulations.

This publication does not necessarily reflect the ING house view. This publication has been prepared solely for information purposes without regard to any particular user's investment objectives, financial situation, or means. The information in the publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Reasonable care has been taken to ensure that this publication is not untrue or misleading when published, but ING does not represent that it is accurate or complete. ING does not accept any liability for any direct, indirect or consequential loss arising from any use of this publication. Unless otherwise stated, any views, forecasts, or estimates are solely those of the author(s), as of the date of the publication and are subject to change without notice.

The distribution of this publication may be restricted by law or regulation in different jurisdictions and persons into whose possession this publication comes should inform themselves about, and observe, such restrictions.

Copyright and database rights protection exists in this report and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All rights are reserved.

ING Bank N.V. is authorised by the Dutch Central Bank and supervised by the European Central Bank (ECB), the Dutch Central Bank (DNB) and the Dutch Authority for the Financial Markets (AFM). ING Bank N.V. is incorporated in the Netherlands (Trade Register no. 33031431 Amsterdam).