- Report

July Economic Update: From yesterday to tomorrow

- 2 July 2020

The reopenings have led to a sharp rebound in activity, but new localised Covid-19 outbreaks have cast a renewed cloud over the global economic outlook for the second half of the year. Discover the latest views and ideas from ING's economists and strategists in our July update

Inside this edition

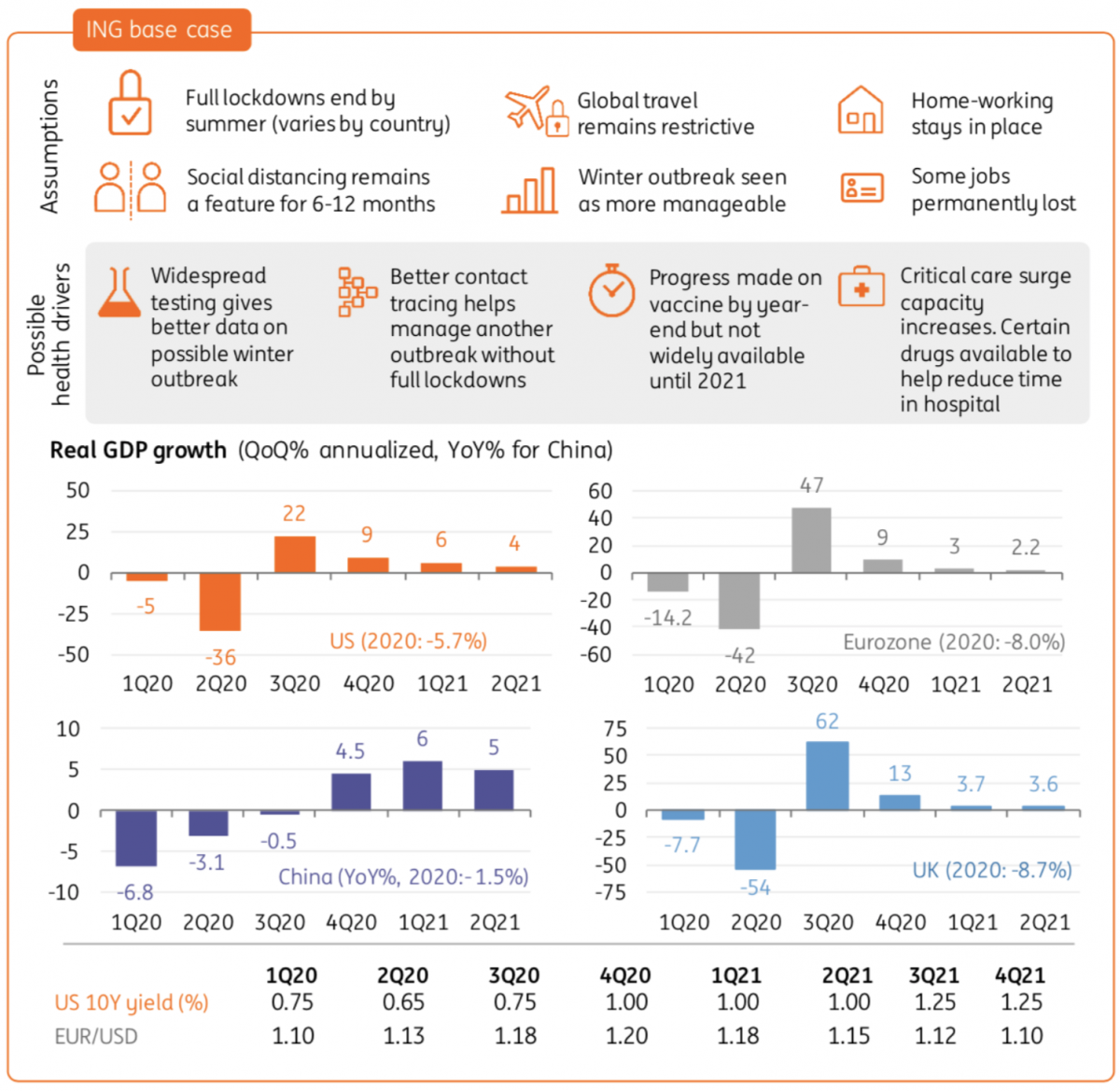

US: The wrong direction

- Covid-19 infections and hospitalisations are on the rise in many states, leading to fears that the recovery could falter in response to renewed restrictions and consumer caution. In the absence of a vaccine, the Federal government will need to provide more support to keep the economy on the recovery track

Eurozone: a deceptive ‘V’

- Recent indicators point to a V-shaped recovery, but that won’t last very long. With the European Central Bank trying to appease the German Constitutional Court further rate cuts look unlikely, though an increase in the Pandemic Emergency Purchase Programme is still in the cards

China: Covid-19 adds pressure to exports

- Domestically-driven growth has been faster than foreign-driven exports and manufacturing. It seems that occasional Covid-19 clusters have not disrupted domestic demand too much. As such, we have revised our PBoC policy forecast to no more rate cuts for the rest of 2020

Asia: India and Indonesia riding up the Covid-19 curve

- First China, now India and Indonesia – two more of Asia’s largest economies face their worst recession in decades, thanks to Covid-19. But the divide in the market's perception is reflected best by the performance of their respective currencies. The rupiah is one of the best performers in the EM space while the rupee hasn't been appreciating very much since the rally started

Latin America: Recession deepens fiscal challenges

- Covid-19 continues to spread across Latin America but, given the mounting economic costs of stay-at-home orders, governments are easing social isolation guidelines. Robust economic policy responses should help lessen the recession but will leave behind severe fiscal challenges that should alter intra-region relative performance post-pandemic

FX: Markets leave lockdowns behind them

- This month, we’ve been tasked with looking at the effects of lockdown exits on FX markets. The truth is there that does not seem to be a strong relationship there. Instead, FX markets are being driven by the abundant liquidity story. As summer progresses, however, we expect US elections to make their mark. Both themes are dollar negative, in our opinion

Rates: Warning signs that equities might have it all wrong

- Most financial instruments are present values of a discounted stream of future income. For equities that is earnings. For core bonds, it is coupons, plus principal payback. For high yield, a spread is added to compensate for the non-systemic risk. The equity discount is upbeat. The rates discount is ominous. The HY one is in between. Something must give

US Politics: Troubling times for Mr President

- President Trump is languishing in the polls both nationally and in the swing states that are key to winning the electoral college and re-election. Democrat rival Joe Biden is keen to keep this a referendum on Donald Trump, but the President has other ideas and is going on the offensive

CEE: Gradual recovery but no deflation

- It seems that Central and Eastern European economies are through the worst and a gradual recovery lies ahead. Despite the sharp fall in growth, there aren't any deflationary pressures as these economies were running hot prior to the Covid-19 crisis. All this is likely to translate into limited monetary easing ahead, but Poland remains very dovish

ING's base case

Source: ING

Included in the following bundle

Bundle

3 July 2020

Reopening vs resurgence

- This bundle contains 8 Articles

Bundle

2 July 2020

July Economic Update: From yesterday to tomorrow

- This bundle contains 10 Articles

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more