- Report

February Economic Update: Stick or twist?

- 8 February 2019

A substantial softening in the Federal Reserve’s rhetoric on monetary policy, coupled with encouraging signals from the US-China trade talks have boosted market risk appetite, but we are approaching key dates that will be critical for the global economic outlook. Read more in our latest economic update

A dramatic softening in the Federal Reserve’s rhetoric on monetary policy, coupled with encouraging signals from the US-China trade talks have boosted market risk appetite, but we are approaching key dates that will be critical for the global economic outlook. Will President Trump stick with what he has won already or will he gamble for a bigger victory to take to the electorate for the 2020 election? The odds of the latter are rising. If we do see an escalation of trade tensions, the global growth story will deteriorate, having broad-based implications for financial markets and currencies.

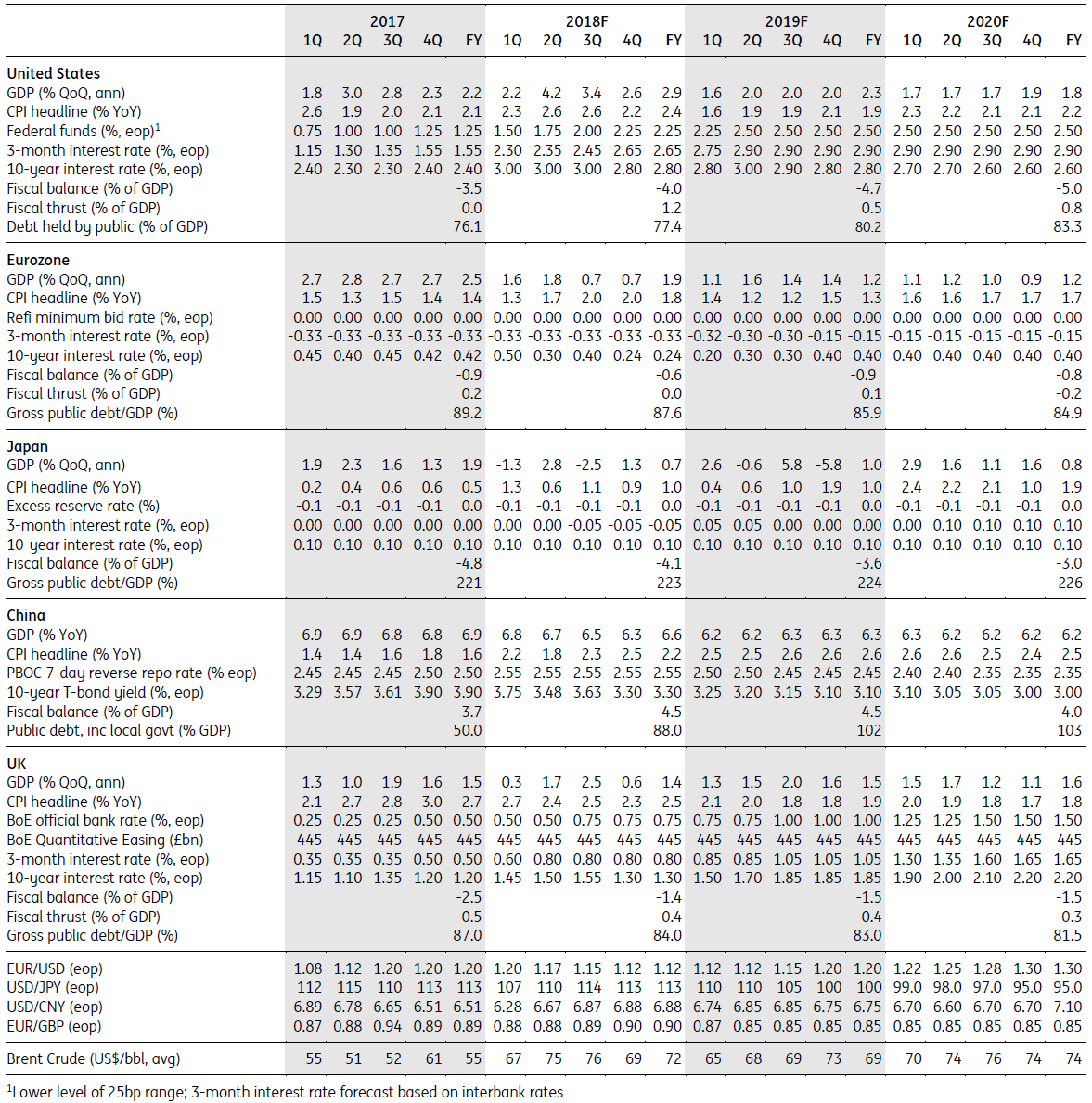

The US economy remains in good health with the government shutdown having ended, employment rising strongly, pay picking up and the Federal Reserve signalling that they are in no hurry to tighten monetary policy further. This Goldilocks story has boosted both US equities and bond markets. Assuming a benign global trade story, the prospects of a Fed rate hike remain strong.

Even though this is our official base case for now, we are increasingly considering a more negative trade scenario. If President Trump chooses to move more aggressively he could win additional concessions from both China and the EU but this is likely to come at the cost of weaker near-term growth. If this scenario were to come true, it is possible that US interest rates have already peaked for the year.

The Eurozone continues to grow, albeit at a more subdued pace. A reversal of some one-off effects could bring slightly higher growth in the second quarter, but risks to the downside remain. US tariffs on European cars could yet be another brake on growth, in addition to the Brexit uncertainty. We don’t see inflation picking up much, so there’s little need for monetary tightening. On the contrary, we believe the ECB is likely to decide on new longer-term liquidity operations to avoid a tightening of credit conditions.

The Brexit impasse in the UK shows no signs of breaking. The EU is refusing to budge on the Irish backstop, while Prime Minister May is still reluctant to push for a cross-party solution. One way or another, an extension to the Article 50 negotiating period looks increasingly inevitable, which would prolong uncertainty for businesses.

The Chinese economy is weakening on several fronts and not just due to the US-China trade war. In response, the government is looking for ways to boost consumption. Tax cuts may not be enough, to avoid a softening in the labour market. Even worse, the People’s Bank of China has continued to let USD/CNY follow the dollar index, and a stronger yuan could end up offsetting some of the stimulus.

We have identified a change in rates market psychology; it shows that rates are peering down, but we’d prefer to bet against this as a tactical view. Structurally there will indeed be rate cuts at some point down the line. But to accelerate towards this, a deeper deterioration would be required. It’s worth remembering the current risk-on mood is implicitly pushing against this too.

The Fed pause and the US: China trade truce has improved the external environment and allowed under-valued currencies to recover. As long as the trade truce holds, we expect this positive environment to continue and the dollar to stay gently offered. However, a serious risk event this month is the threat of US tariffs on auto imports. If they materialise, EUR/USD would retest the 1.12 lows.

ING global forecasts

Included in the following bundle

In case you missed it: Trade truce withering away

- This bundle contains 8 Articles

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more