April Economic Update: Cheer up! The gloom is mostly set to fade

A sense of gloom has been hanging over markets for the past few months. However, the situation may already be starting to improve with progress on US-China trade talks and tentative signs of stronger activity from major economies. So while we are becoming a little more optimistic, market caution is likely to linger for a little while longer

A sense of gloom has been hanging over markets for the past few months, reflecting trade tensions, softer activity data and political strife. However, the situation may already be starting to improve with progress on US-China trade talks and tentative signs of stronger activity from major economies. Nonetheless, politics are never far away, with European parliamentary elections and Brexit creating uncertainty. We are also waiting for President Trump’s decision on possible auto tariffs. So while we are becoming a little more optimistic, market caution is likely to linger for a little while longer.

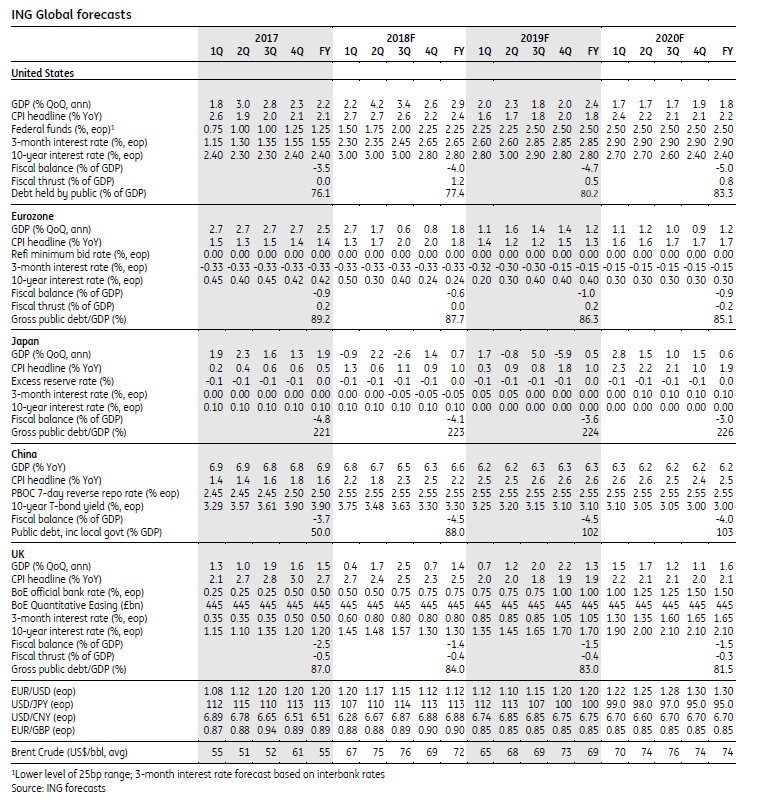

The US yield curve inverted and interest rate cuts are being priced in from the Federal Reserve as fears of an economic slowdown gripped financial markets. This largely reflects some mixed domestic data and worries about demand from China and Asia. However, we are more upbeat, with clear signs that 1Q GDP growth may be significantly stronger than initially feared, while a robust labour market should underpin consumer sentiment and spending.

We would also argue that the yield curve is not as powerful recession predictor as it has been in the past. Moreover, if we see a positive resolution to US-China trade tensions this may lift more of the gloom and lead to a re-pricing of the path for interest rates.

While first-quarter Eurozone growth was weak, March data seems to suggest a rebound is in the offing. With improving consumer sentiment and international trade off lows, the second quarter could come a bit stronger, provided that a ‘hard Brexit’ is avoided. Inflation continues to surprise to the downside, justifying continuing monetary stimulus. Reports of the European Central Bank contemplating a two-tier system for excess liquidity, thereby helping the banks, are perhaps a bit premature. We believe this scheme will only be put in place if an additional rate cut would be considered.

Nobody knows for sure where Brexit will take us over coming days, but talk of a long extension to the Article 50 period is growing. That would continue to put pressure on investment, not just because of the uncertainty, but also because firms may have to restart their contingency planning. The chances of a 2019 UK rate increase are fading, but don’t rule one out completely if a Brexit deal can be approved by MPs relatively soon.

China’s fiscal stimulus has begun to work. Manufacturing PMI showed activity expanded in March. We believe this is in large part thanks to the fiscal measures taken over recent months. Continued support from fiscal policy will likely be required to maintain activity even if a trade agreement with the US is reached.

Japan’s economy continues to disappoint on both growth and inflation, though the latter presents few genuine problems except presentational for the Bank of Japan, and a debate about the logic of continued negative rates and money printing is beginning to gather volume. We have dropped out the consumption tax hike from our forecast.

The markets see a US rate cut as probable. If the next move in the Fed funds rate is down, then history also shows that the 10yr can trade 25-50bp through in anticipation. At the same time, we believe the pessimism about growth is a tad overdone.

Unless Eurozone growth can prompt a re-rating of European equities or longer-tenor debt spreads move substantially against the dollar, it is hard to see EUR/USD breaking out of a 1.10-15 range in the next 3-6 months. We are thus downgrading our end 2019 and 2020 forecasts to 1.18 and 1.25 respectively.

Download

Download report

5 April 2019

What’s happening in Australia and around the world? This bundle contains 9 Articles

"THINK Outside" is a collection of specially commissioned content from third-party sources, such as economic think-tanks and academic institutions, that ING deems reliable and from non-research departments within ING. ING Bank N.V. ("ING") uses these sources to expand the range of opinions you can find on the THINK website. Some of these sources are not the property of or managed by ING, and therefore ING cannot always guarantee the correctness, completeness, actuality and quality of such sources, nor the availability at any given time of the data and information provided, and ING cannot accept any liability in this respect, insofar as this is permissible pursuant to the applicable laws and regulations.

This publication does not necessarily reflect the ING house view. This publication has been prepared solely for information purposes without regard to any particular user's investment objectives, financial situation, or means. The information in the publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Reasonable care has been taken to ensure that this publication is not untrue or misleading when published, but ING does not represent that it is accurate or complete. ING does not accept any liability for any direct, indirect or consequential loss arising from any use of this publication. Unless otherwise stated, any views, forecasts, or estimates are solely those of the author(s), as of the date of the publication and are subject to change without notice.

The distribution of this publication may be restricted by law or regulation in different jurisdictions and persons into whose possession this publication comes should inform themselves about, and observe, such restrictions.

Copyright and database rights protection exists in this report and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All rights are reserved.

ING Bank N.V. is authorised by the Dutch Central Bank and supervised by the European Central Bank (ECB), the Dutch Central Bank (DNB) and the Dutch Authority for the Financial Markets (AFM). ING Bank N.V. is incorporated in the Netherlands (Trade Register no. 33031431 Amsterdam).