Will house prices continue to rise forever?

- 11 September 2017

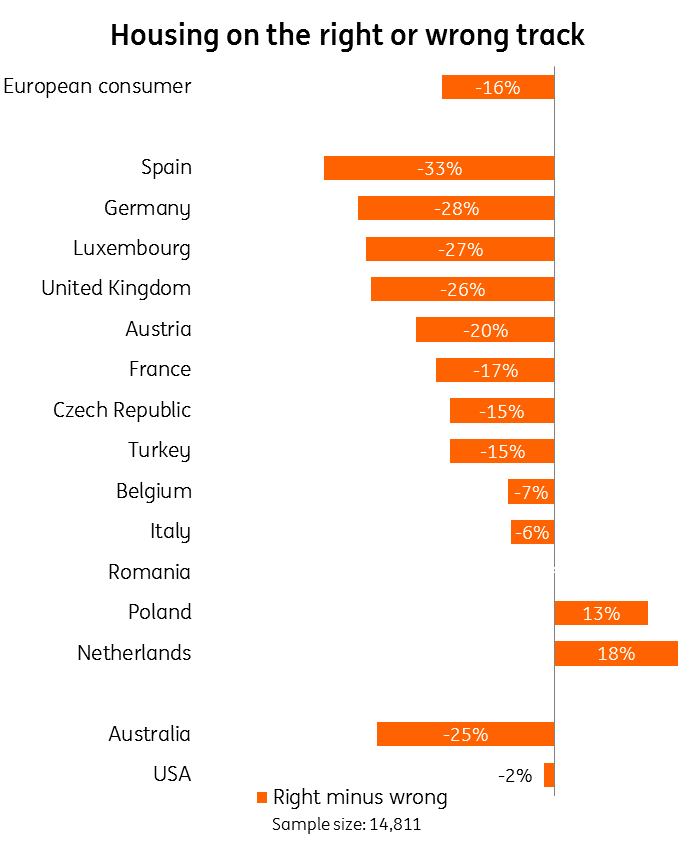

House prices are high, and many expect them to continue rising. Four in ten of those who thought about their housing costs the last time they moved ended up paying at the top end or more than they planned. And one in five find it difficult to pay their rent or mortgage each month, so it’s little wonder that 45 percent in Europe believe housing is on the wrong track.

These are the main findings of the sixth ING International Survey Homes and Mortgages 2017 in which 15,000 people in 15 countries were surveyed.

The story behind the figures

We could argue the toss about these figures. For example, it’s hardly surprising many push their budgets to the limit when it comes to housing, and while one in five find it difficult to pay the rent, that implies four in five don’t.

The history of housing markets is filled with bursting bubbles yet many remain oblivious to the risks.

But this misses the point. There is widespread concern about housing in many countries, and many people appear to be pushing their finances to the limit to get the housing they want or need.

The idea that this occurs only in a few countries could not be further from reality. The survey shows similar concerns in many countries. Arguably the situation is worse in Spain, Germany, Luxembourg, the UK and Australia but better in the Netherlands and Poland. Comments from ING’s economists in many of the countries surveyed suggest these concerns are felt most keenly in larger cities –a opinion supported by an IMF blog post from December 2016.

Caught in a trap

The idea that many people consider housing to be expensive but still expect house prices to continue to rise could be rational. Demand for housing can exceed supply for a long time, especially in the main cities. However, one in three also agrees with the statement that ‘house prices never fall.’ That’s where alarm bells start to ring.

The history of housing markets has many examples of falling house prices - either quickly or on a sustained basis. Yet many appear oblivious to the risks they are exposed to when taking their housing cost to the limit. Those who buy are more vulnerable. Digging into the survey data 45% of those owning a home either outright or with a mortgage bought at the top of or above what they planned. For renters it’s 35%.

But what are people meant to do? Everybody must live somewhere. It appears new houses cannot be built fast enough to meet demand, so housing sets to remain expensive for a long time.

If so, the ability of central banks to raise interest rates may be limited by the ability of households to withstand any further increase in housing costs. But the greater tragedy is that many people’s prospects will remain constrained by high housing costs.

For more Homes and Mortgages trend analysis and other ING International Surveys, visit our sister site eZonomic's here.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more