Trade delay

- 6 November 2019

After yesterday's encouraging news on trade, now the disappointment - any phase 1 trade deal now looks unlikely to be signed until December. Is there more than just a venue issue here?

Is this more serious than just a venue question?

Yesterday, I chatted through the market implications of what looked to be some fairly positive noise on a possible phase-one trade deal, with what I hope were some interesting if not entirely relevant asides on the best sort of pork pie and James Bond Movies.

Today, as is depressingly common these days, yesterday's news turned out to have little substance. Maybe it was floated to take the sting out of today's suggestion that any such deal might now not be signed until December?

There has been an ongoing struggle to find a venue for the signing of such a deal. The US seems to be out. China may not want to be seen as the co-erced partner in any deal by signing in the US, at least without a state visit taped around it. That does not seem to be on the cards - something like that would normally take months to organize. So Switzerland or Sweden are now being touted as "neutral" countries to observe a deal being signed.

But the location of any deal ceremony is considerably less important than any willingness to sign a deal at all. Or to the substance of any such deal. China has been quite open about what it wants for such a deal - with a rollback of existing tariffs top of its wish list. Yesterday we cited reports that the US was indeed considering such rollbacks.

This morning, as well as the widely reported deal delay, one of my colleagues in the US has outlined the hostility to the removal of tariffs from high-ranking officials in the US administration, one of whom was speaking at an event in NY. Reading that this morning, I now suspect our rather cautious attitude to any trade deal, which I indicated might need revision yesterday, may not need much of a tweak after all. The question really is, do we even get a December deal? Or does this keep being pushed back, like a Brexit deal?

Markets have responded in a muted fashion so far, but in the opposite way to yesterday. Namely: gold is up, copper down, Brent crude is down. USDCNY looks stable but is now trading at around 7.0, and the INR is looking weaker again.

This story looks set to run and run. This is good news while Brexit developments are on hold pending the election. It gives me something to write about.

I'll also let you know how my postal vote application goes. It has been a week now. Nothing in my letterbox yet.

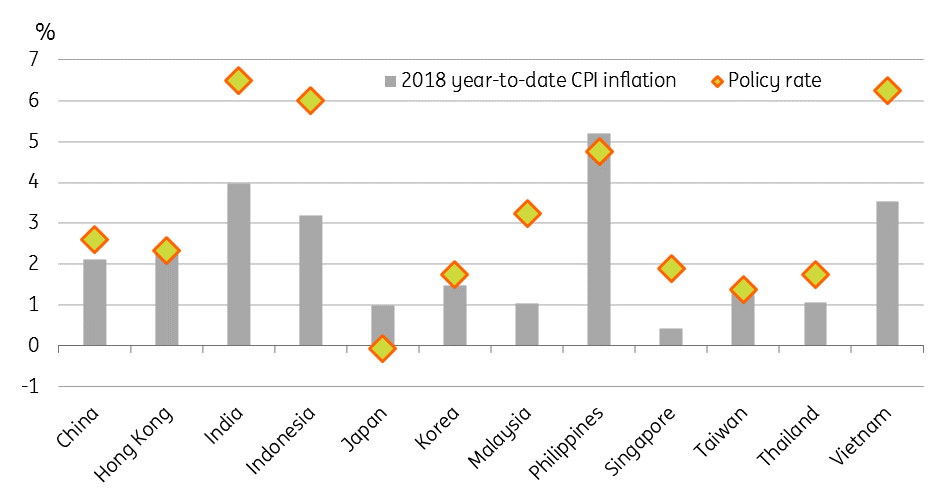

Does Asia have room for more monetary stimulus?

Monetary policy - out of room

Following Austrian Central Bank Governor Holzmann's comment yesterday that monetary policy in the Euro area had run out of room, let me turn my thoughts to whether the same is true for Asia. But first, for those with Bloomberg access, do please read Daybreak's Cameron Crise today. He is always excellent, but especially on the money today regarding central bank policies and the harm they are doing.

As for Asian monetary policy, the fact that one of Asia's most hawkish central banks, the Bank of Thailand cut rates 25bp yesterday would suggest that there is still room for monetary policy easing here in the region. But if that comment is true in an absolute sense, in a more nuanced sense, I'm not so sure.

Consider yesterday's BoT cut. Do we imagine it will make a big difference to insipid Thai growth? No. Do we imagine that it will deliver more than a temporary softening to the Thai Baht (THB)? No. And so we hold out hope for much more easing fro them? Again no.

There are a few economies in the region where there is still some room for some monetary stimulus. Indonesia is one. Malaysia is perhaps another, Vietnam too. But the list is getting shorter, and the gap, as measured by "real interest rates" is narrowing, and likely to shrink further as helpful base effects fall away from inflation over the coming months to remove some of the downward bias to the current inflation numbers.

But if we have learned anything from the period running up to and following the global financial crisis, it is that what we may have considered barriers to policy in the past no longer apply. Perhaps we should no longer consider negative real rates the "floor" to policy in Asia. Maybe. But if so, and we embark on a journey to the nominal zero rate bound, then I'm afraid that this will simply confirm the point of the Austrian central bank governor now applies in Asia. Monetary policy will have run out of room.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 7 November 2019

- This bundle contains 3 Articles