For Asia, “too low” oil prices are “a thing”

- 8 March 2020

- China

Globally, oil is not a “tax” on income, it's closer to a “transfer” from producers to consumers - but even that is a simplification. For Asia, there is a price at which both consumers and producers are mutually “content” - deviations from this on either side can weigh on growth and this is where we are heading

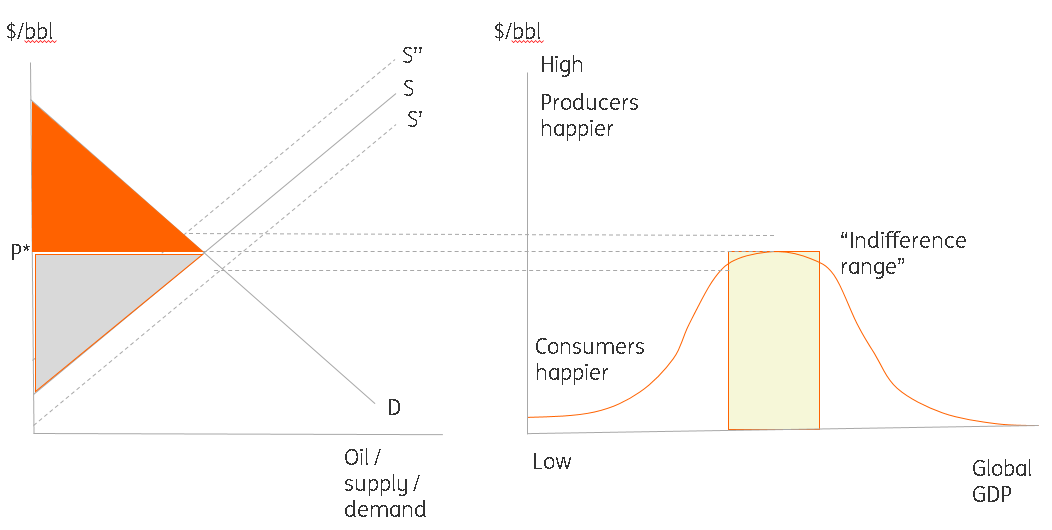

What is the "indifference" range for oil?

When I was a much younger economist, you would respond to swings in the price of oil by consulting one of the OECD "ready reckoners" printed in the back of the World Economic Outlook. This would tell you what a $5/bbl increase/decrease in the price of a barrel of oil would mean for your GDP and inflation forecasts.

Back then, when the DM world dominated the global economy and most of them were both oil-intensive in production and typically net-oil consumers, it sort of made sense. But even then, it required you not to care what was happening to producer nations. A more sophisticated view of oil prices emerged as the world changed and EM economies started to dominate global GDP. This required you to think of oil as a zero-sum game, where oil producers benefited from a rise in the price of oil, and consumers form a fall and vice versa.

This sort of thinking still prevails in many forecasting circles, but even this is a gross simplification.

Let me explain with a simple 2-country model of the world. Here there are just two economies, and one produces and sells only oil, and the other produces and sells only chocolate. When the price of oil is very high, the chocolate producers can't afford to buy very much, and producers lose out, and when the price is very low, the chocolate producers can buy loads, but it doesn't earn enough for the producers, who then can't buy chocolate. There is a price of oil at which producers can buy quite a lot of chocolate, and consumers can buy quite a lot of oil, both probably still grumble, which is why I refer to this as the "indifference range" for oil. Just by observation, and limited empirical analysis, I have viewed this range as about $10/bbl either side of $65/bbl.

Following the breakdown in OPEC+ negotiations at the end of last week, which Warren Patterson has highlighted in this note, crude oil prices are down around $36, and will almost certainly head lower in the days ahead unless someone changes their mind.

The "indifference range" for oil

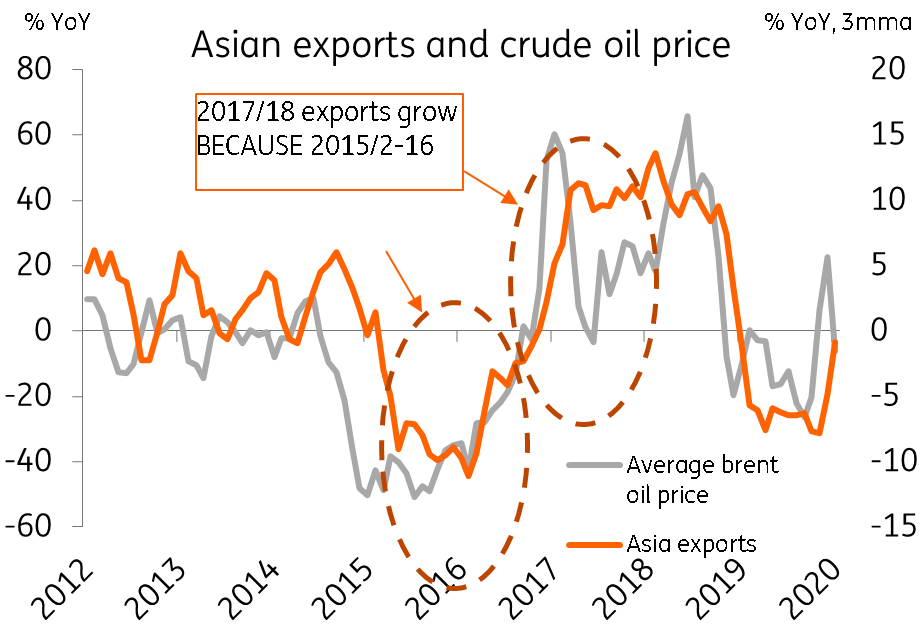

Crude oil price and Asian exports in practice

Well, that is so much for the theory, how about the practice? The chart below shows how swings in crude oil prices have preceded swings in Asian export growth, with the most notable plunge in recent history being 2015/16, which led to a big fall in Asian export growth, and then as oil firmed through 2017/18, helped their recovery. The chart is specified in terms of year-on-year changes, but it also works in levels ($/bbl) against the percentage change in exports. Oil prices are now plunging, following the breakdown of OPEC+ talks.

It is hard to see how this sort of shock could have come at a worse time for Asia. Even India, where we would normally expect an oil price decline to provide some support to the rupee, is unlikely to see much benefit, as it is embroiled in its own financial sector problems, with the collapse of a private bank at the end of last week. The MYR stands to lose too as the region's most notable oil exporter.

Oil swings and Asian exports ("indifference range" in practice)

Don't write off China's GDP after this quarter

Iris Pang provides some hope for Chinese GDP after what looks like it will be a horrific 1Q20 judging by the trade data released over the weekend.

Iris writes, "China has issued more than CNY 1 trillion of local government special bonds recently to finance infrastructure investment. The “new infrastructure investment” mentioned by the media, includes 5G investment, electric car charging facilities, electricity infrastructure. These are all planned infrastructure. The name “new infrastructure” highlights that this investment will not include property, which is in trouble from high leverage. We believe front-loading of planned “new investment” will support the recovery of the economy from 2Q20".

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

In case you missed it: Pandemic pandemonium

- This bundle contains 13 Articles