Enjoy it while it lasts

- 3 July 2020

- Australia Singapore

Data reflecting the re-opening of economies will increasingly run into headwinds unless Covid-19 numbers begin to improve - that feels like wishful thinking

Data on the turn?

This will be a short note - and the main reason I am writing anything at all today is to direct you towards James Knightley's write up of yesterday's US labour report, which has given markets another boost.

In particular, scroll down to have a look at the chart of the Homebase jobs figures, a seemingly new set of figures in the arsenal of US labour market watchers (since my day anyway), and which cover many of the smaller firms that are not covered by the payrolls survey or ADP. Here, the news is not very good, with recent re-opening rollback actually leading to some further joblessness, not just a slowdown in the gains. A similar story is being told by the continuing unemployment claims figures, which drifted higher over the latest week.

The main point of this is to say that the positive economic momentum seen in the data and caused by the re-opening of the economy, could be running out of steam. And in some areas, it may actually be turning back on itself. If the re-opening is what has been powering the market recovery, we might well consider its implications for the weeks ahead if data now starts to soften.

Infection upsurge

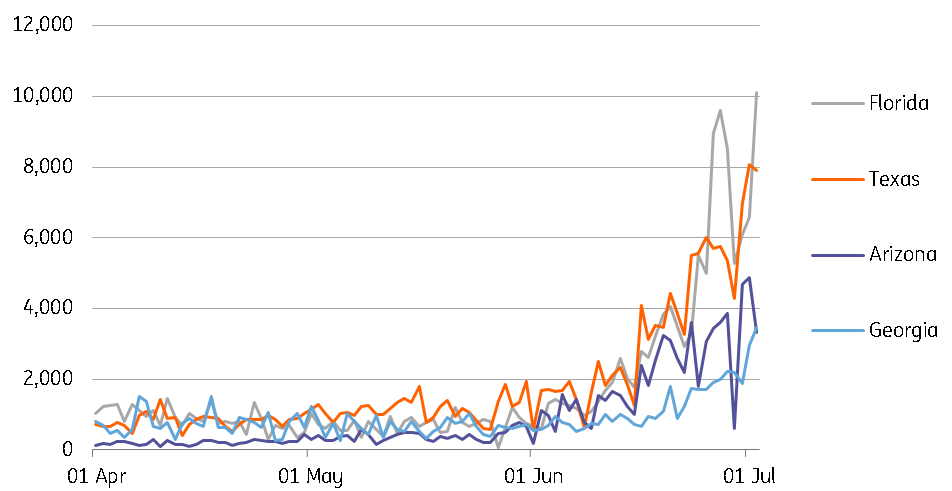

In the background of all of this is the Covid-19 new daily case figures, which topped 50,000 for a second consecutive day. While the new daily death trend remains on a downward slope, I expect markets to turn a blind eye to this. But it will become much harder to do this if new daily cases transform after a suitable lag into new daily deaths, as has been typical during this pandemic. Better ways of treating Covid-19 may be helping flatten the death trajectory, and the coming week will most likely show us if we have grounds for concern or not. The 4 July Independence Day celebrations may provide a new source of rising infections though, if social distancing measures are not adhered to, including mask-wearing.

US Covid-19 cases - new daily cases (selected states)

Asia day ahead

Most of the world will be releasing service sector PMI data today if it has not already done so. Australia has already released its CBA services PMI, which at 53.1 indicates that despite the Covid-19 problems in Victoria, the reopening in the rest of the country continues to allow recovery, even if at a fractionally slower pace than last month (previous PMI was 53.2).

Prakash Sakpal picks up some of the releases from the ASEAN region:

Singapore: June’s manufacturing PMI and May retail sales are today’s data line-up. The reopening of the economy from the Covid-19 circuit-breaker should nudge the PMI higher. However, as in most Asian economies, we don’t see it crossing the 50 threshold for expansion just yet. The PMI loosely tracks year-on-year GDP growth, which we forecast slumping to a record -9.2% YoY in 2Q.

Private consumption will be the main expenditure-side drag on GDP, as the retail sales data should stress. We are looking for a 52% YoY fall in sales, steeper than the 40.5% fall in April. Supermarket sales should continue to outperform non-essential consumer spending of all sorts, while big-ticket items like cars should remain a dominant pull on the downside, as also evident from the more than 90% YoY plunge in new registrations in May.

Thailand: June CPI inflation is due today. Relaxation of Covid-19 restrictions and return of pent-up demand underpins the consensus of slightly less negative inflation (-3.1% YoY vs. -3.4% in May). The risk is tilted on the downside though, with high base effects likely pushing food inflation into negative territory. Housing and transport prices have been the other sources of falling inflation recently and they remained in play in June. We expect inflation in the rest of the year to stay around -3%. There isn’t any easing space left for the Bank of Thailand though.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 3 July 2020

- This bundle contains 6 Articles