Bond rally continues as Mexico tariffed

- 31 May 2019

Arguments for a pause/correction are doing the rounds, but as of now, the rally in Treasuries remains in place helped by the surprise imposition of 5% tariffs on Mexico.

| 5% |

US tariffs on Mexican goodsRising to 25% |

Mexico tariffs stymie thoughts of a bond pullback

Perhaps helped by a smaller downward revision to 1Q19 US GDP, perhaps end-of-the-week / end-of-the -month short covering, or for possibly a million other reasons, US Stocks had a slightly better day yesterday, though it was marginal.

Bond bulls were maybe also beginning to feel a little jittery, with stories doing the rounds of technical factors that may put a dent in the bond bull run, if only for a few days. They might have been right. Certainly charts of the 10Y US Treasury note look overbought, though such conditions can persist for days, weeks even.

But the surprise imposition by the US of 5% tariffs on all Mexican goods to start on June 10 and be gradually increased up to 25%, has put the market in a risk-off mood, and that should ensure that the bull run continues today. The tariffs are in response to illegal immigration by Mexicans, and will not be removed until the US is satisfied that Mexico is tackling the problem.

Meanwhile, there is scant evidence of any movement on the US-China trade war, probably because the Mueller interview and subsequent reactions by the US President as well as these new tariffs on Mexico have taken the limelight. So with these issues dominating the headlines, I think the case for lower bond yields, lower stocks, and a slow grind stronger by the USD vs Asia currencies remains in place.

Korea in the spotlight

A slightly better than expected April industrial production figure for South Korea today (+1.6%MoM) pared the year on year rate of decline to only -0.1%YoY. If we ever had a chance of our BoK rate cut decision paying off today (and realistically, we never have) then this was probably the last nail in its coffin. The arguments for a cut remain overwhelming in my view. Weak growth, and seriously sub-target inflation. But the best we can probably hope for today is some dissent amongst BoK voters to tee us up for a July cut. Fingers crossed though, as there is nothing to be gained by waiting and plenty to lose.

Japanese inflation

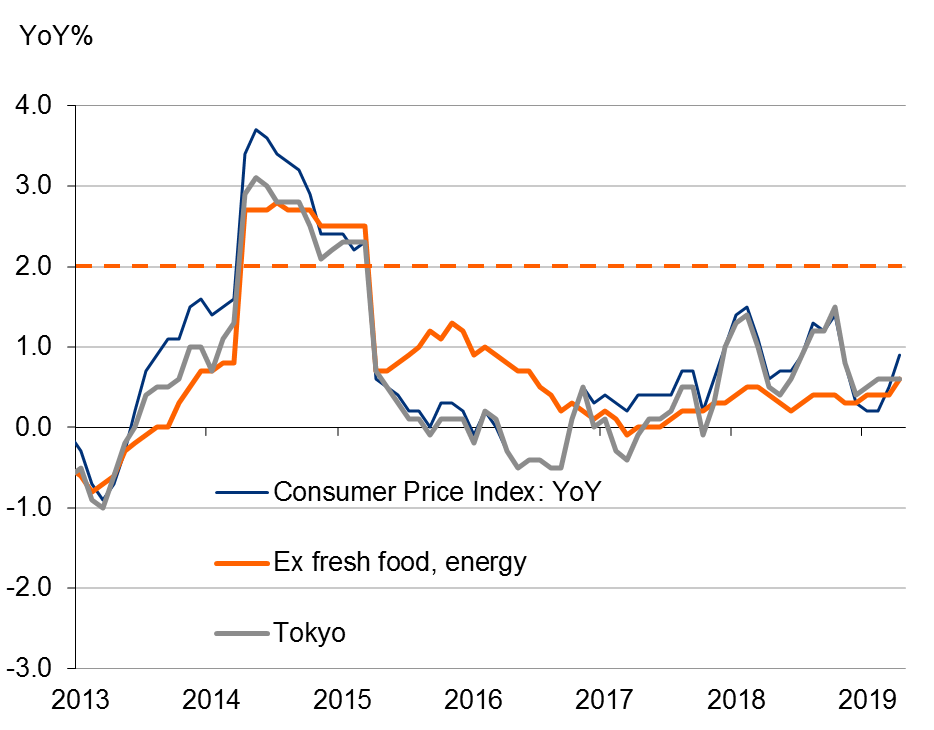

Japanese inflation drifts lower

Japan's inflation is only newsworthy to the extent that it has serially failed to come close to the BoJ's target. And even within the BoJ, it now seems as if 2% is being reconsidered as a sensible yardstick by which to set monetary policy.

This is a good argument to have, and one that is not irrelevant to many other OECD economies that are systematically failing to meet inflation targets, notwithstanding exceptionally accommodative monetary policies.

Tokyo inflation, which leads the national figures by one month, drifted lower in May, with the ex-fresh food and energy figure now at 0.8%. This has been a good run since 2017 though, and an uptrend may still remain in place, though 2% remains an unattainable target in my view.

India slows

(From Prakash Sakpal) Like pretty much everywhere else in Asia, India's growth appeared to slow in 1Q19, the final quarter of the financial year 2018-19 for which GDP data is due today. If so, our forecast of a slowdown of growth to 6.0% from 6.6% in the previous quarter will make it the slowest growth quarter in two years. While this will validate the Reserve Bank of India's two rate cuts this year, we don’t think the central bank would want to risk tempting the inflation genie by cutting rates again at the next meeting. We see no further downside in growth from here as RBI easing so far, together with a surge in election-related government spending and favourable base effects should help the recovery in the period ahead.

Rest of Asia - China PMIs

With the trade war in full focus, China's PMIs will get top billing amongst the other Asian releases today. The consensus has the manufacturing PMI dipping below 50 (just) to 49.9 from 50.1 last month, though the non-manufacturing index is thought likely to hold its ground at 54.3. Our China economist, Iris Pang sees a slightly different mix, with the non-manufacturing index slipping slightly, as dampened sentiment about the tech sector weighs on consumers, but the manufacturing index nudging up fractionally helped by government stimulus measures.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 31 May 2019

- This bundle contains 4 Articles