Japan’s central bank: Best intentions, poor outcomes

- 21 March 2019

- Japan

To add to a long list of things considered cornerstones of Economics, which I suspect are well-meaning but misguided, let me propose central bank policies, as rates approach or pass zero. This is of particular note for the Bank of Japan, but the ECB might also want to pay attention

Growing debate in Japan about the central bank's policy

Pensioners committing acts of petty crime to get locked-up and receive food and shelter is a trend that is on the rise in Japan. Who's to blame? Could you perhaps point a finger at the Bank of Japan (BoJ)?

While that claim may sound outrageous, it might not be so crazy after all. But in giving it the benefit of the doubt, it requires you to accept that much of what you may ever have been taught or learned about economics was either wrong or at best, only partly right. That shouldn't be too hard a concept to swallow surely? A recent article by Jim O'Neill - he of BRIC fame - suggests the same, though without any detailed consideration (at least that's my view). We try to go one better here.

So how does all this relate to the Bank of Japan?

Negative rates may be doing more harm than good

It isn't such a big stretch to make the claim that the Bank of Japan's extended relationship over the years with unorthodox monetary policy, qualitative and quantitative easing, zero and negative interest rates and negative bond yield targeting, has failed to achieve what was intended - a consistent increase in price level inflation, and faster nominal GDP growth. At present, the central bank has an inflation target of two percent. Right now, they aren't even close, and few believe it'll ever be achieved.

The subject I will focus on is the non-linearity of the investment-savings decision as rates approach zero or turn negative. Believe me, it isn't as dull as it sounds

So why has it been such a big failure? There are many factors I could list here, but in this note, I will deal with only one of them. The subject that I will focus on here specifically, though acknowledging that there may well be many others, is the non-linearity of the investment-savings decision as rates approach zero or turn negative. Believe me, it isn't as dull as it sounds.

Most text-book economics is a big simplification

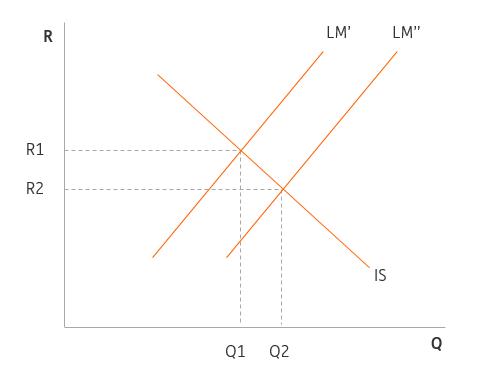

When you first get taught Economics, you will come across various versions of what is known as 'IS-LM' analysis. This combines the LM curve, which shows the relationship between the money supply for different interest rates and economic output, and the IS curve, which shows the substitution that occurs between investment and saving at different interest rates.

The basic notion is that at lower interest rates, people substitute investment (by which we mean any spending, which can include business investment) and saving (any part of your income that you don't save). This is called the IS curve, and in almost all textbooks, it is simplified - as is the LM curve - as a straight line. So as rates are lowered or the money supply increases (LM shifts right from LM' to LM'' as you can see in the chart below and output rises from Q1 to Q2.

This essentially is a boiled-down version of the thinking behind all central bank monetary policy - lowering rates or supplying more money with quantitative easing shifts out the LM curve, and (even if only for a short time before inflation or an appreciating currency erodes its influence) results in stronger growth and in the process, higher inflation.

Traditional IS-LM curve analysis

The problem is it doesn't work

The theory and the practice of this type of thinking worked reasonably well through most of the central bank era of inflation targeting, though it's worth reminding ourselves, that this era wasn't really that long, and that for much of the prevailing time, inflation was considerably higher than is typically the case these days.

I don't think it's my imagination, but the power of low rates to boost economic activity seems to have diminished

During the successive cyclical upswings and downswings, market bubbles and bursts, central bank interest rates have peaked and troughed at lower and lower levels, as have market bond yields.

I don't think it's my imagination, but the power of low rates to boost economic activity seems to have diminished. Now central banks talk about raising rates to have room to cut them, suggesting the level of rates are no longer the determining factor of output, even in the short term. Instead, only the rate of change seems to be important and even then, not very much.

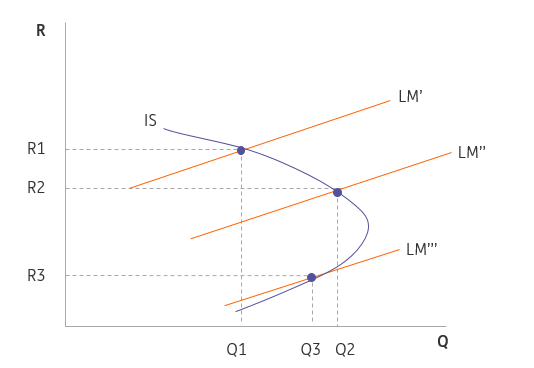

One explanation for this could be that as rates approach zero, the IS curve becomes non-linear. Indeed, for what I am about to describe, the IS curve becomes 're-curved'.

(For the mathematicians reading this, please let me know the proper term for the shape of the curve illustrated below, as a quick search on Wikipedia didn't throw up convincing answers).

IS curve at low or negative rates

The power of the market...

Geometry, like that shown above, can be fiddly. So how about a real-world explanation to describe why we may have a curve this shape and what the implications of this may be.

Consider people from my parent's generation, born in the 1930s. They worked and earned in a world where there was inflation, from the 1950s through 1990s, with positive and significant interest rates. Borrowing was costly, and servicing that debt ate up a lot of disposable income. Cutting rates really did free up a lot of spending power. A bit of inflation also helped deflate away the outstanding pile of debt, so real interest rates were the important measure for how tight monetary policy was.

Consider people from my parent's generation. Higher rates meant they were encouraged to save more to benefit from greater returns. But in the process, they would spend a little less - and this is how monetary policy worked

My parents could save, with even low-risk savings like bank deposits getting a non-trivial interest rate. And, thanks to the power of compounding, this helped grow their savings. Market returns were also higher, though of course, inflation was also a scourge on savers.

At the point of retirement, or of realising the value of a savings project for other purposes, not only would the pot of savings be considerably more than the sum of savings, thanks to non-trivial interest rates, but in the case of a pension, it could be harnessed to pay an income that might even be high enough to fend off starvation. Higher rates meant my parents would be encouraged to save more to benefit from these greater returns. But in the process, they would spend a little less, and vice versa. This is how monetary policy worked - and, for the most part, it did work.

...not really powerful any longer

Now take today's savers. A peak-earning person of middle-age looking towards a retirement date in the next ten years or so will look at the miserable rate of return on their savings, with bond yields and interest rates close to zero. In Japan's case, this is absolutely true or even generous as rates and bond yields can even be negative. In Europe's case, it is close to the truth, though bond yields still remain positive, they are in many cases very low. For these savers, a lifetime of saving may generate a savings pot of not much more than the sum of their savings.

Sure, inflation is low, but debt levels rose as rates successively fell, and borrowers now get no relief from higher inflation. Indeed, as rates have been cut towards zero, savings haven't always been reduced and substituted for spending. Instead, today's 50 - something will likely save even harder (resulting in Q3 in the chart above, where Q3<Q2).

The market is providing these savers with no boost in terms of compounded growth rates towards their pension goals and the projected income stream from the savings pot at retirement age will also be effectively zero, requiring the pot itself to be spent to support retirement income. The 50-something today may have to save many times as much as the same demographic 30 years earlier, and faces a poorer income in retirement. No wonder they save even harder as rates fall.

What does this all mean?

What this tells you is what most pensioners in Japan would likely tell you, namely, that running ultra low, even negative policy rates and bond yields is in net terms, doing more harm than good, even if there are some beneficiaries in the corporate world - but don't even get me started on zombie companies and productivity.

Keeping rates low to maintain a weak currency may also hurt these individuals. Pensioners spend disproportionately more of their incomes on food than working families - much of which is imported. So their savings incomes are squeezed, and then their cost of living rises as the yen depreciates. Double whammy - which is why a spot of shoplifting, even if apprehended, can seem a reasonable trade-off to an increasing number on the edge of poverty in old age in Japan.

What this tells you is that running ultra low, even negative policy rates and bond yields is in net terms, doing more harm than good

Were the Bank of Japan (or dare I suggest the ECB) to actually abandon its current, and arguably failed policy efforts, it may find, higher rates aren't met with collapsing consumer spending, but the exact opposite. Yes, I dare say the yen would appreciate a bit and the headline CPI inflation rate would fall even further. But Japan seems to be managing quite well with an inflation rate of practically zero, and I don't believe households would start to panic if their incomes actually stretched further in real terms, even if that did mean a negative growth rate for the headline CPI index.

Why now?

Although this is the precisely the sort of unorthodox thinking that would get me kicked out of the monetary policy setting committee of most central banks, a recent quote from Japan's finance minister, Taro Aso suggests that some members of prime minister Shinzo Abe's government are also having a re-think about Bank of Japan's targets. "For the general public, there isn't a single person out there saying it's outrageous that we haven't reached 2 percent inflation". He recently added: "You have to think about the possibility that things will go wrong if you focus too much on 2 percent".

It looks as if the Japanese government is coming round to my way of thinking on the non-linearity of the IS curve as rates approach or pass zero, but the central bank might take a little longer. This sort of unconventional thinking is anathema to most central bankers and may take a little time to percolate. They would rather apply unorthodox policy remedies based on orthodox thinking, even if they don't seem to be working.

But in bravely taking the lead on this, Japan's central bank could provide a very useful lead to other central banks around the world who are clinging on to zero or negative interest rate policies, without much sign of any benefit. You know who I'm talking about...

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

What’s happening in Asia ?

- This bundle contains 9 Articles