- Opinion by Padhraic Garvey, CFA

A list of worries that risk flipping much worse

- 27 March

- Rates

A week ago we wrote that the marketplace was flashing Amber, and should things not improve, there is the prospect of flicking to Red (here). We're still in that place, but if anything, even closer to a lurch to Red. We need a positive delta soon in order to change the market mindset. We head into week five of the war in more hope than expectation. Here's the lowdown

The realisation has dawned that there is no quick 'off switch' to this war, and that's being reflected in the rates discount

President Trump’s recent efforts to calm things were nothing more than a flop, as Iran countered with their own requirements and conditions for an end to hostilities. The Strait of Hormuz is the real battle of contention right now, as it’s a pain point that Iran knows it can hurt the US with. As we commence week five of the conflict, we’re in a stand-off mode between the two sides, and, meanwhile, the lobbing of munitions from both sides continues. The US has options, ranging from 'the benign' – pulling back and declaring victory, to 'the malignant' – placing troops on the ground to help force open the Strait. There are many other options in between, of course, but the game of interpretation takes place between these two extremes.

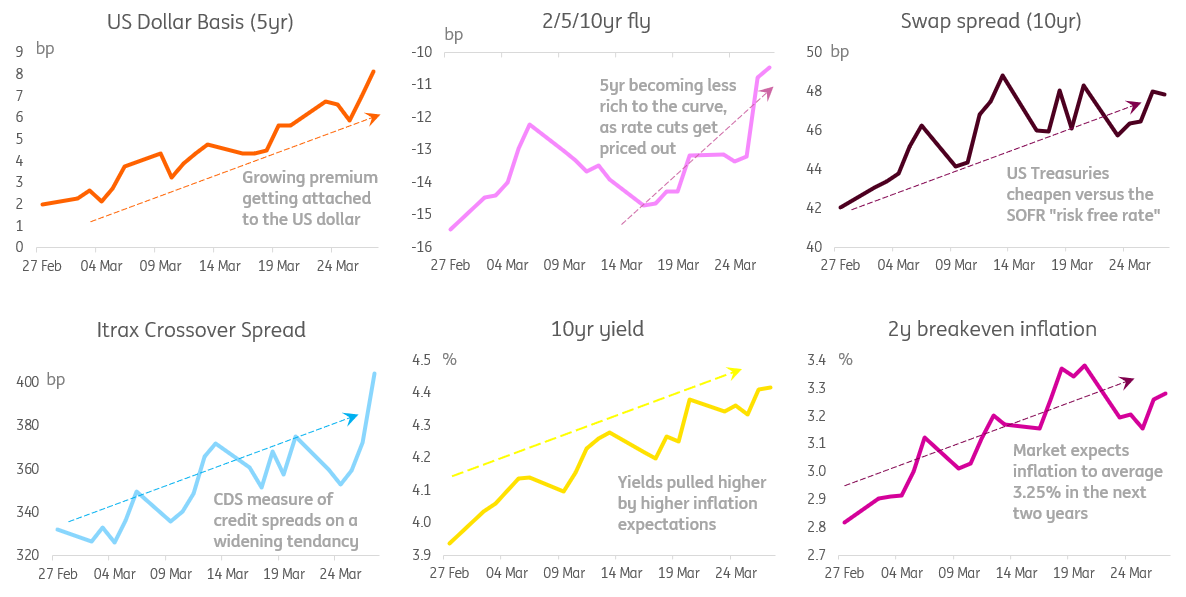

We’ve had a re-elevation in inflation breakevens, alongside a re-ratchet higher in the price of oil. Front-end breakevens are discounting US inflation approaching 4% in the coming quarters (vs 2.5% CPI inflation now). In consequence, Fed interest rate cut expectations have evaporated, and if anything, the market now attaches a greater probability to a hike than a cut as the next move. The structure of the Treasury curve is still pricing cuts, given that the 5yr area continues to trade rich versus the 2yr and 10yr interpolation. But that richness is significantly less than it was. And market rates have been on the rise. The 10yr yield got close to 4.5% before easing lower a tad. That's quite a move from sub-4% just before the war broke.

The equity market has morphed to a clearer risk-off phase. The only silver lining is that credit spreads today are at or below their 5yr averages. But another interpretation is we’re on a journey wider if things don’t calm in a material fashion in the coming weeks. The yield curve has squeezed flatter and higher, and the prognosis ahead is for even higher yields, at least until this thing sees a material positive change in sentiment.

We're left with a whole series of arrows pointing resolutely in a troubling direction.

A dashboard of pain coming from the Rates Market

Things to watch – barometers of things beginning to boil out of control (USD basis and swap spreads)

And then there is a quirky basis premium being attached to the US dollar (on cross-currency swaps). This was practically zero before the war broke. It’s now just below 10bp, albeit still not particularly high. In previous crises, it’s been a barometer of stress, and has been multiple times the current level. Various patches to the capacity to get hands on US dollars over the years have dampened basis re-widenings during periods of stress. We’re not anticipating a spiral wider, but it's absolutely one to watch.

The other one to watch is the swap spread, and here we like to look at the 10yr tenor. It’s now just short of 50bp; so, the 10yr Treasury yield is 50bp above the 10yr 'risk-free' SOFR rate. Basically, it’s the price the US Treasury needs to pay over and above the risk-free rate as a cost for fiscal untidiness. Should Treasuries come under specific selling pressure from a credit perspective, it will show up here. The danger level would be 60bp, or even the approach of it.

The market price action in rates is broadly centred on a pricing in of more and more risks coming from a longer war

Adding some flavour, we’ve seen three Treasury auctions come and go in the past week, and they were all awful. It’s indicative of a market that requires a discount to get business done. There has been some selling of fixed income, and in particular high yield. But it has not been dramatic, as there is still demand out there. The selling itself has not been the driver of market movements, as it’s been relatively tame. Rather, the market is steadily re-pricing the aforementioned risks that’s driven the bulk of the price action.

The market environment craves a positive delta. Even a clear sign that things are getting less worse would be a good starting point. As it is, we are slavish to the whims of key decision makers. There is a huge relief trade to be had here, on a path-switch to a quicker resolution in the war. But until then, the risk remains for a large lurch in a bad direction.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more