WTO conference faces challenges as big players turn inward

- 23 February 2024

Measures facilitating trade are still outweighing those that restrict it globally, but the gap is narrowing for large economies (G20) and recent signs of looming protectionism on the side of the US and Europe are not encouraging for trade. However, given the general benefits, and the energy transition, it’s important for them not to overshoot

On 26-29 February, ministers of trade gather in Abu Dhabi for the 13th biennial WTO conference to discuss the way forward in global trade. It’s a pivotal moment for trade and comes amid considerable challenges and uncertainty. Strengthening supply chains, food security, implementing digital trade frameworks, geopolitics, protectionism and climate change are all on the agenda.

Trade is increasingly politicised leading to more protectionism

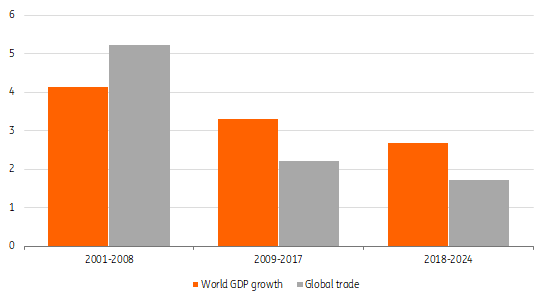

After a period of strong globalisation and expansion in the 1990s and in the run-up to the financial crisis in 2008-2009, we have entered an era of increased geopolitical tensions. While trade growth previously exceeded global GDP, it is now lagging behind. The composition of trade is changing, services are more important, and the pace is set to remain slower for longer. This is primarily due to geopolitics. Trade relations between the US and China have been subject to tensions while Russia’s invasion of Ukraine, and the trade sanctions associated with that, have impacted the direction of global goods flows. Houthi militant actions leading to the disruption of the Red Sea shipping route are the most recent example of geopolitical interference in trade. Meanwhile, recent disruptions due to the pandemic and extreme weather events have initiated a rethink of supply chains, and emerging initiatives to (partly) shift production elsewhere (including closer to end markets).

World trade has lagged global GDP for a while now

Average growth in global merchant goods trade vs global GDP over different time periods in %

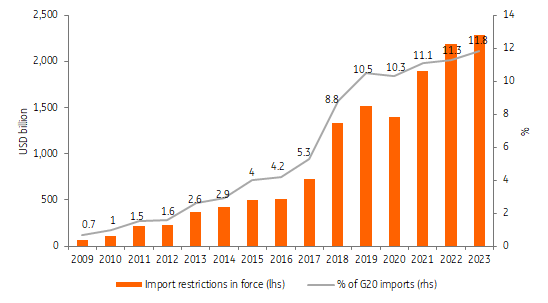

Calls for more self-sufficiency have grown louder while the number of protective measures has increased. From 2017 to 2022, the number of trade restrictions has nearly quintupled, according to Global Trade alert data. This means that companies active in or dependent on trade are finding more obstacles in their way. G20 economies, in particular, have become more restrictive lately. At the end of 2022, 11.3% of G20 imports were subject to restrictive measures on goods implemented by G20 economies since 2009. In 2023, this reached a new high (11.8% until 10/15/23), while export restrictions on food, feed, and fertilisers, persist amongst WTO members.

When looking at the value of world merchandise trade, the share covered by new trade-facilitating measures still exceeded new trade-restrictive measures between May 2023 and October 2023. But the gap is narrowing.

The impact of new restrictive trade measures by G20 countries is mounting

Cumulative trade coverage of G20 import-restrictive measures on goods in force since 2009

The energy transition leads to larger dependencies, but protectionism could slow greening

Global trade patterns are changing in the wake of the energy transition. Green technologies such as electric cars are creating new and larger dependencies. This is especially the case for raw materials (such as metals, including rare earths) and specific intermediates where China dominates production. In the EU and the US this is raising concern, with China gaining ground in multiple supply chains, such as for chips and batteries, that are essential for the transition. But despite efforts to ramp up their own chip and battery production, Europe, in particular, won’t be fully self-supporting and continues to rely on trade. In the meantime, there’s growing concern about distorting government support and potential dumping. As such, the European Commission launched a formal investigation against China and the US expressed similar concerns. But we should also acknowledge that mounting protectionism could lead to spiralling retaliation and slow down progress in greening the economy.

A balanced approach remains key as trade must flow…

Trade has been subject to conflicts for centuries, but it is also a lubricant for cooperation. Countries have crucial interests to preserve. It’s not only about fair competition, but values such as human rights, security and environmental aspects matter as well. Although the economic benefits currently seem to be subordinated to risks and geopolitical concerns, we shouldn’t forget that trade delivers net global economic benefits. Some level of specialisation usually pays off for both exporters and importers. Although we still expect global merchandise trade to grow in 2024, the reality is that support for free trade is diminishing. The costs of ongoing fragmentation could potentially reduce global economic output by as much as 7%, according to the IMF. And we should also realise that systemic changes – such as the energy transition – usually come with pain and gain. We need to make offers to progress and take businesses and the economy forward. Either way, it takes time to adjust.

The tendency in trade is increasingly protective, and there are clear arguments behind this. But in the interest of global prosperity and progress in the energy transition, we shouldn’t overshoot. The world’s policymakers are in a position to find a balanced way forward and offer more clarity. Businesses across the world will be interested in their common narrative.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more