With a Little Help From My Friends: the importance of CDMOs will continue to grow

- 20 January 2026

Thanks to their flexible manufacturing capacity, CDMOs were among the few beneficiaries of the uncertainty created by the Trump Administration. Despite reduced uncertainty in 2026, we still expect the CDMO market to deliver robust growth driven by geopolitical fragmentation and growing consolidation in regional manufacturing hubs

Side A: key calls

- The global CDMO sector is expected to experience 9% growth until 2030.

- APAC will widen its lead over Europe as the second-largest CDMO market.

- Aside from growing fragmentation, factors driving growth are increased drug complexity and higher demand for weight-loss drugs.

Strong CDMO growth will continue for the foreseeable future

The branded pharma sector breathed a sigh of relief when it turned out that the impact of tariffs and most favoured nation (MFN) pricing proved relatively limited.

Contract Development Manufacturing Organisations (CDMOs), companies that offer outsourced services such as manufacturing, on the other hand, may have been disappointed. They were among the few beneficiaries of increasing uncertainty. But, even with limited tariff and MFN impact on the branded pharma space, we still foresee very strong growth for the CDMO sector until 2030. CDMOs have become increasingly important for pharmaceutical manufacturing. In 2014, pharma outsourcing to CDMOs was 34%. In 2023, that number was 49% (Pharma Advancement). This is primarily driven by an increase in biologics; 70% of that production is outsourced to CDMOs.

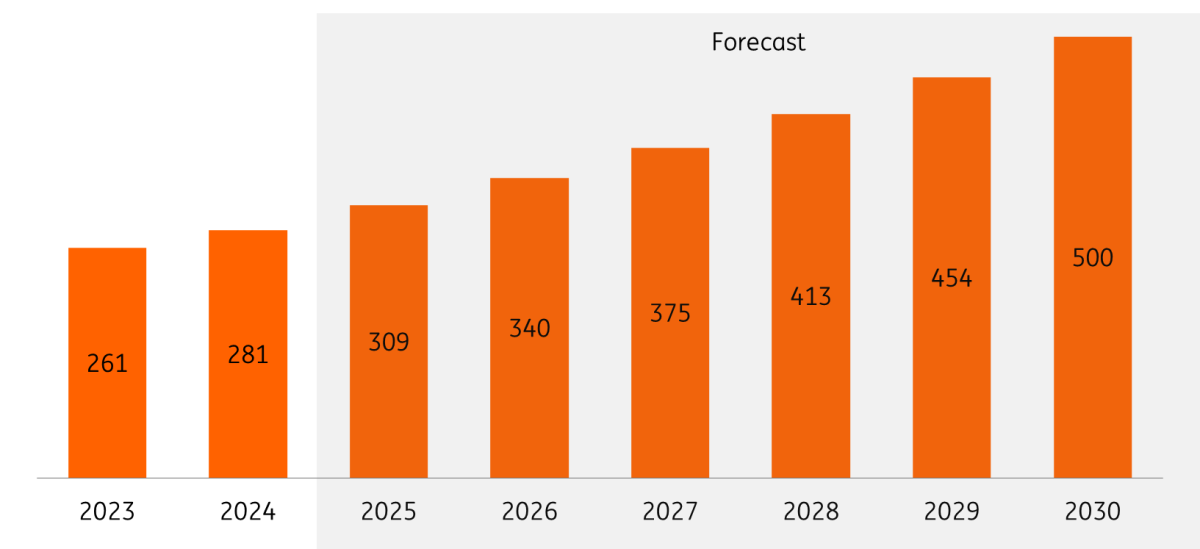

We therefore forecast a 9% compound annual growth rate (CAGR) until 2030 for CDMOs, which means that the market will hit $500 billion in 2030. This forecast is mainly driven by growing geopolitical fragmentation and increasing tensions. As a result, governments will incentivise local drug production (e.g. the European Critical Medicines Act) for national security reasons. This, in turn, means that we will see consolidation in regional manufacturing hubs, which will prioritise proximity to core markets over cost optimisation. This is a net cost for pharma companies, but a net benefit for the CDMO space, which is why we expect very strong growth.

Global CDMO market to experience strong growth until 2030

Size of the CDMO market in $ billion

Growth will also be driven by increased complexity and demand for weight-loss drugs

A few other factors drive strong growth in the CDMO space. First, the complexity of manufacturing processes has increased substantially. In recent years, we have seen a gradual shift from chemicals to biologics as well as an increase in precision medicine (i.e. the tailoring of therapies to specific patient subgroups) and technical innovation (e.g. peptides and conjugates), which means that manufacturing processes are increasingly complex. All of which increases demand for CDMO services.

Furthermore, innovators often lack manufacturing capacity, further increasing reliance on CDMOs. Second, the blockbuster demand for GLP-1s (or weight-loss drugs) is often met via increased investment in CDMOs, which further drives the positive outlook. In short, CDMOs are increasingly important from a strategic point of view as well as an answer to increased GLP-1 demand and more complex manufacturing practices.

Given increased demand and increased fragmentation, it is no wonder that M&A in the CDMO space will increase in the coming years. As we discussed in our article Come Together, 2026 will be a good year for M&A in biotech and pharma in general, and the CDMO market is no exception. European branded pharma companies, in particular, will look to CDMOs to make vertical acquisitions in the US to hedge themselves against more policy changes and produce in the world’s most profitable market, as we have seen with Novo Nordisk’s acquisition of sites from Catalent.

On the other hand, CDMOs are also looking to pharma for acquisition of sites (e.g. TMO’s acquisition of Sanofi sites). Further demand will come from CDMOs with less presence in the US to ensure a more balanced customer offering, and there is notable interest in assets from Asia, where CDMO companies are also rising in importance. Recently, we have seen Samsung and Fujifilm concluding partnerships with big pharma companies.

APAC is already a more important CDMO market than Europe, and the gap will widen

The global CDMO market is largest in North America, whose size is nearly equal to the combined markets of Asia Pacific (second) and Europe (third). We expect strong growth in all three geographies, albeit stronger growth in North America and APAC than in Europe. North America will see stronger growth than Europe because it is home to the most profitable market and has instituted several protectionist measures, which will keep investment in CDMOs high.

APAC will experience stronger growth for pharmaceuticals than in Europe and North America, and benefits from relatively low energy prices, cost and efficiency advantages on which it can build.

The forthcoming Critical Medicines Act has the potential to modestly spur additional growth in Europe by removing cost-based procurement for 243 critical medicines. However, in the absence of lower energy prices and more incentives for European manufacturing, we expect the gap between the US, APAC and Europe to widen in the coming years.

APAC is the second largest CDMO market globally

Share of global CDMO market per geography, in percentages

Side B: remaining questions

Geopolitical fragmentation is a key driver of CDMO growth, but it is unclear how long governments, and Europe in particular, will sustain and expand on localisation incentives, such as the Critical Medicines Act. If the Act is successful and Europeans start paying more for medication produced closer to home, then growth of the European CDMO space could surprise to the upside.

At the same time, we are wondering whether the growth drivers of the CDMO sector (GLP-1s, biologics, precision medicines and complex modalities) could turn into bottlenecks, and growth of the sector could potentially surprise to the downside. If CDMOs cannot scale smoothly (e.g. in terms of investment, construction or talent), these same growth drivers could create new bottlenecks rather than tailwinds.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Pharma’s 2026 hit list: The White Album

- This bundle contains 6 Articles