Will the Russia-Ukraine conflict cloud Indonesia’s growth outlook?

- 22 March 2022

- Indonesia

Indonesia's growth outlook was upbeat at the start of 2022, but have things changed since the conflict in eastern Europe began?

GDP grew 3.7% in 2021. Is a sustained recovery viable?

Indonesia’s economy grew 3.7% in 2021 driven in large part by consumer spending bouncing back during periods of low daily Covid infections. Government officials expect GDP growth to settle between 4.7-5.5% this year. Is this likely given the current challenges faced by Indonesia? We’ll take a quick look at what we can expect this year, especially in light of the latest geopolitical developments in eastern Europe.

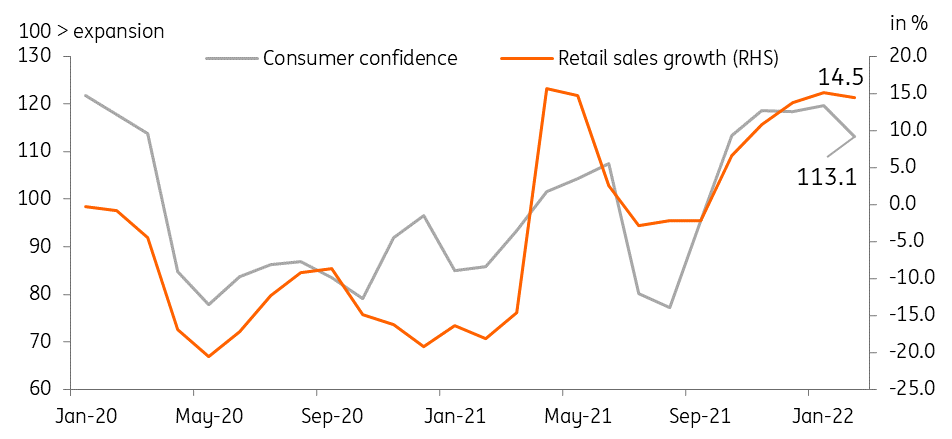

Retail sales track consumer sentiment

What’s going well?

Consumer confidence improved considerably in the fourth quarter of 2021 likely due to new daily Covid cases sliding below 1,000 by November. This pickup in consumer sentiment was reflected by the sharp rebound in retail sales. This shows that household consumption has remained dependable, especially during periods of successful Covid mitigation. Thus, it will be important for authorities to gain control over the virus as this could allow a steady recovery for retail sales and overall household consumption.

What’s not going so well?

Indonesia’s recovery gained momentum at the end of 2021 but the recent Covid wave will likely dampen Indonesia’s growth prospects, with manufacturing just one of the sectors impacted. Health officials have refrained from implementing strict lockdowns during this most recent wave and yet we note the slip in manufacturing momentum as a result of the surge in cases. Furthermore, the increase in Covid cases appears to have also dented consumer confidence, with the latest reading in March sliding to 113.1 from 119.7 at the start of the year.

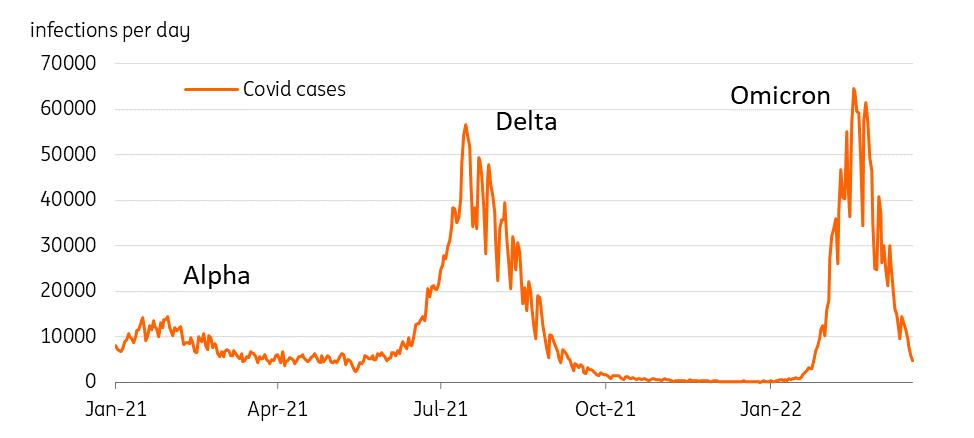

So, despite positive developments at the turn of the year, growth momentum may have slowed somewhat because of Indonesia’s vulnerability to virus outbreaks. Indonesia’s vaccination rate remains one of the lowest in the region (56.2% of the total population is fully vaccinated) and until authorities improve this metric, growth prospects will always be weighed down by the emergence of new variants.

Indonesia remains susceptible to potential Covid waves

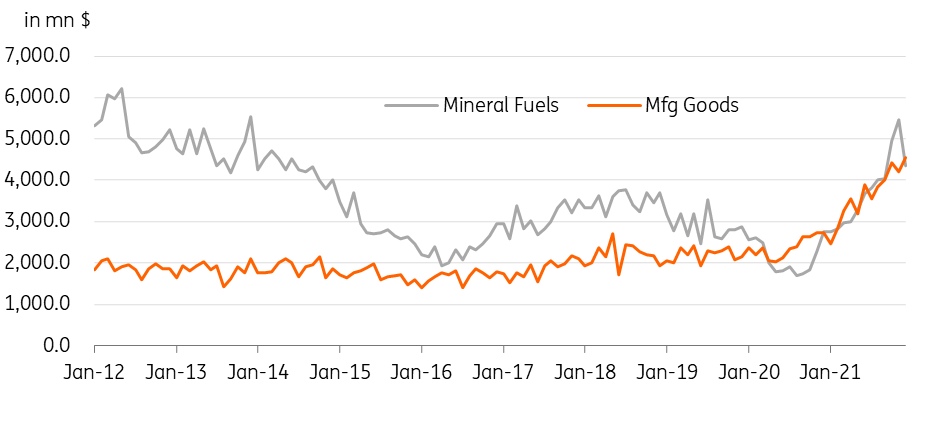

The wild card: export shift to manufactured products

One strategy that Indonesia aims to pursue as part of its Covid recovery strategy is to accelerate its shift away from a reliance on consumption and focus on growing its manufacturing sector. In turn, a dynamic manufacturing sector would drive the maturity of the country’s export base from raw materials (commodities) to higher value-added manufactured products. Earnings from finished products would bring in fresh flows of foreign currency, providing a new source of support for the currency and at the same time opening up job opportunities for a host of supporting industries. We have noted the strategic shift over the past few years (2012 to present), and we would likely need to see this trend continue to ensure a more sustainable and robust recovery. Already we’ve witnessed manufactured goods equal exports of mineral fuels and we can expect finished products to eventually outstrip mineral fuels after prices for commodities normalise.

Shifting gears: Indonesia bets on switch to manufactured goods for export recovery

Fallout from the crisis: more than meets the eye

At face value, Indonesia’s relatively low exposure to Russia and Ukraine suggests that its recovery prospects won't be impacted by the war. Indonesia exports palm oil, coconut oil and cocoa butter to Russia, while it sends Ukraine palm oil, nickel and margarine. Meanwhile, Indonesia imports the bulk of its wheat and iron from Ukraine while bringing in iron and fertilisers from Russia. When taking total trade into account, exports and imports from these two countries look negligible – however, commodities such as wheat (food security) and iron (raw materials) remain integral to Indonesia’s recovery. Furthermore, the net impact of the continued fighting has moved global prices of commodities across the board from food staples to raw materials and energy. Therefore, even if Indonesia’s direct exposure to Ukraine and Russia remain relatively modest, we expect headwinds to emanate from surging global commodity prices that will likely add to already budding inflationary pressures.

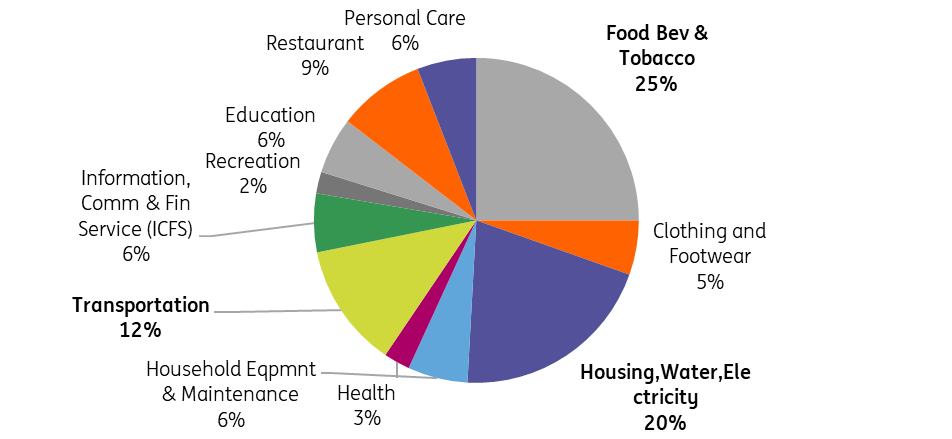

Price pressures in Indonesia were muted in 2021 given soft domestic demand, settling below target for the year. Prior to the Russia-Ukraine conflict, we had projected inflation would revert to target but now we expect inflation to quicken at a much more pronounced pace. Indonesia’s CPI basket is heavy on food (20.5%), utilities (5.8%) and transport (12.4) and a blow-up of imported global commodity prices linked to these sectors could mean that 43.2% of the CPI basket is susceptible to a spike as well.

Transport costs have remained relatively subdued but this is largely due to fuel subsidies that are in effect. Government authorities have not announced plans to increase these subsidies and may in fact be reluctant to do so given their overarching goal to lower the deficit to GDP ratio back to 3% by next year. Meanwhile, food inflation may be impacted by pricier grains and feedstocks, with trade sanctions and the mad dash to secure staples driving up the price of global rough rice by more than 20% year-on-year. A jump in food prices will likely spill over to the rising cost of services (restaurants) and weigh heavily in driving headline inflation past the comfort levels of the central bank. Faster inflation will be one more headwind to domestic consumption, complicating the recovery given that household spending accounts for roughly 65% of total economic activity.

Aside from sapping consumption momentum, higher inflation will also likely force Bank Indonesia (BI) to hike rates sooner than expected. BI Governor Perry Warjiyo previously indicated that any adjustment to the policy rate would have to be driven by concerns about inflation and to a lesser extent by currency stability. The impending pickup in inflation due to commodity price spikes could nudge both inflation and the currency to levels past the central bank’s comfort zone, resulting in a round of monetary tightening sooner than expected. A steady rise in borrowing costs in turn may offset recent gains in bank lending growth, adding one more complication to Indonesia’s recovery plans in 2022.

Indonesia inflation: heavy on food, transport and utilities

Banking on manufacturing but bracing for a fallout from the conflict

Indonesia’s economic recovery at first glance appears to be on solid footing in 2022. A decent pickup in mainstay consumption will be the likely main driver for GDP with the upside for growth provided for by the manufacturing sector. Downside risks remain, however, given Indonesia’s low overall vaccination rate, which could leave the population vulnerable to another Covid surge should new variants surface.

Meanwhile, the fallout from the ongoing conflict is also a potential downside factor with inflation likely becoming an issue once again in 2022. A sharp uptick in prices could force the central bank to hike sooner than hoped for, a move that could dampen the nascent recovery of investment, just as imports of capital goods had returned to pre-Covid levels. All in all, we expect GDP growth to settle at 4.4%, slightly below the official target of 4.7-5.5% as faster inflation induced by geopolitical developments and a round of central bank tightening caps the growth potential.

Market implications? Possibly higher rates and a surprisingly resilient currency

With inflation tracking higher due to both supply side (rising global commodity costs) and demand side (improved economic conditions), we expect Indonesian bond yields to edge higher. Inflation is now expected to hit 3.6% for the year, peaking at 3.9% by the third quarter. Already, we’ve seen the 10-year local bond yield crest 6.7% despite support from the central bank. We believe that rising inflation and a round of tightening from the central bank will be enough to nudge long-end rates to peak at roughly 7.05%, especially with the US Federal Reserve taking on a more pronounced hawkish tilt.

Meanwhile, the Indonesian rupiah (IDR) will likely face some depreciation pressure in the coming months given the possible financial market outflow related to the Fed rate hike cycle. However, unlike past episodes, we have noted a relatively more resilient currency with IDR benefiting from positive export dynamics as higher global commodity prices translate to higher export earnings. Thus, we are likely to see only a mild depreciation episode for IDR in 2022, especially if Bank Indonesia pushes ahead with a modest tightening cycle of its own.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more