The stubbornly high cost of some European building materials despite cheaper energy

- 24 January 2024

- Manufacturing, Construction and Retail

It's been a torrid time for Europe's building materials producers, as construction projects have stalled significantly in the past couple of years. We think the worst will be over for them soon, but that's not the whole story. Despite lower energy costs, input prices remain stubbornly high

Building material production levels will bottom out in 2024

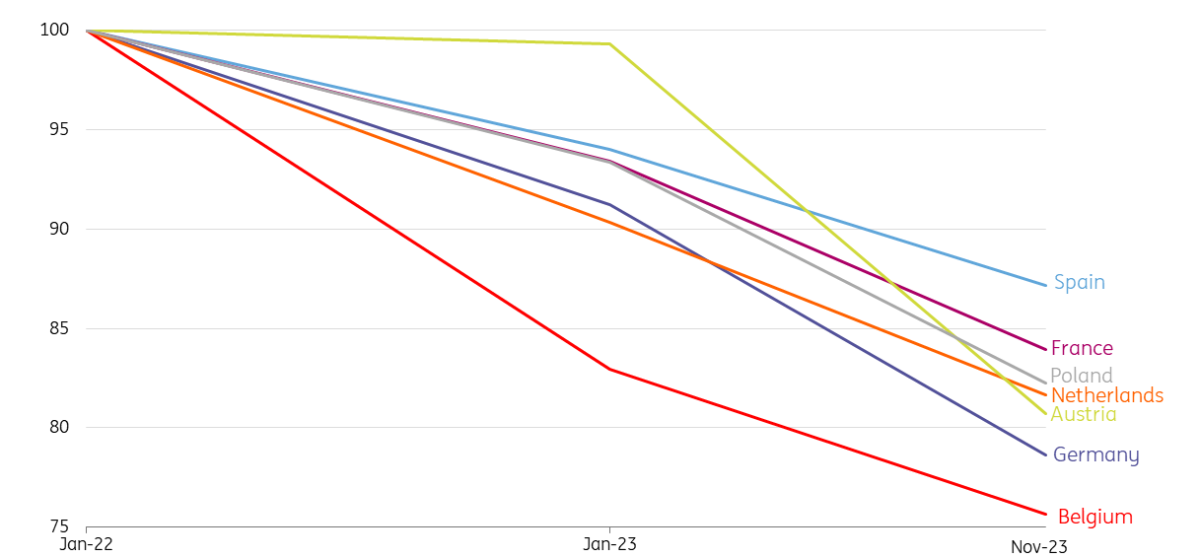

We expect 2024 to be a year of transition for the building materials industry comprising of concrete, cement and bricks. In most European countries, production levels tumbled in the past couple of years; volumes are down by almost 15% in Spain and by nearly 25% in Belgium compared with the beginning of 2022. We believe that those volumes will not start to recover until 2025.

Should European interest rates start to come down, as we expect, and we see sustained higher wages, we're likely to witness a turning point leading to more investments in new premises. However, building projects have a long lead time and the number of issued building permits was still declining in the third quarter of 2023. It will take some time before sales pick up.

Sharp drop building material production due to less new construction

Volume production building material industry (eg. concrete, cement & bricks), Index January 2022=100 SA

The beginning of the end of the decline

There are signs indicating that the worst is over. For instance, the confidence indicator for the EU construction sector is still negative but has slowly improved during the last few months of 2023. The confidence indicator for the building material sector has stopped decreasing. In addition, EU house prices rose again and increased in the third and fourth quarters of last year. This allows project developers to increase prices for new-build dwellings. Project plans that weren’t profitable due to higher building costs can now, at least in some cases, be lucrative again.

For example, local Dutch data support this changing trend. Project developers have seen their sales increase since summer 2023 after a period of decline, and sales of new homes are also on the rise again.

Producer confidence in building material sector is bottoming out

Producer Confidence indicator European Union, SA (monthly, latest data point Dec 2023)

Building material industry more volatile than construction sector

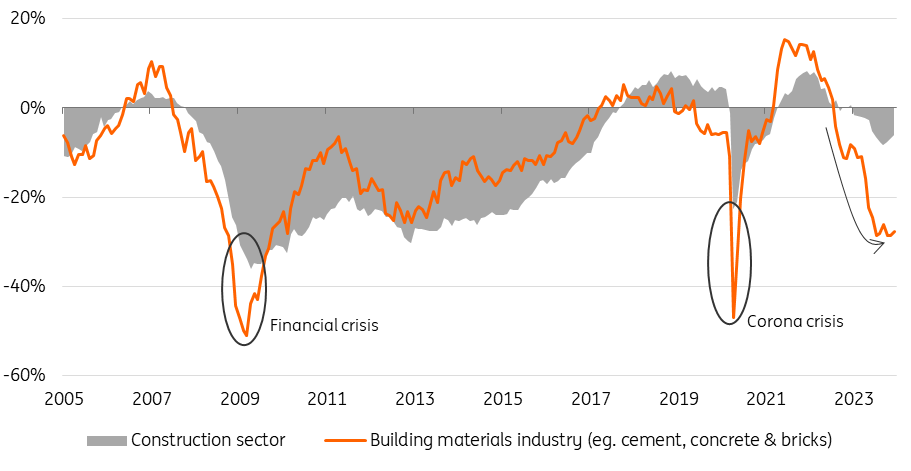

The developments in the building material industry are closely related to the construction sector. Yet, this industry is more vulnerable to economic shocks. There are two reasons for this. Firstly, building material companies generally have higher fixed costs as they have invested more in machinery and factories than construction companies. This makes building material companies less agile; therefore, they have more difficulties scaling down during an economic downturn. Secondly, building materials deliver relatively more supplies for the construction of new buildings and, to a lesser extent, for renovation.

In general, the construction of new buildings is more volatile than renovation. Consequently, building material firms are now more negative than contractors as new building production faces larger obstacles than the renovation market. We saw the same developments during previous setbacks: building material companies were more pessimistic than construction companies at the beginning of the Covid-19 pandemic and the earlier financial crises.

Building material prices are decreasing

The prices of many building materials peaked during the summer of 2022 and have steadily fallen since. The cost of timber and plastic inputs for construction companies have particularly fallen back but they're still higher than their pre-Covid levels. This is due to weakening demand as economic growth is sluggish and construction volumes, especially of new buildings, are declining. The diminished supply chain disruptions after Covid have also eased the upward price pressure. However, the current trade impact of attacks on merchant ships in the Red Sea is just one example of the continued vulnerability in supply chains and could threaten further new price increases.

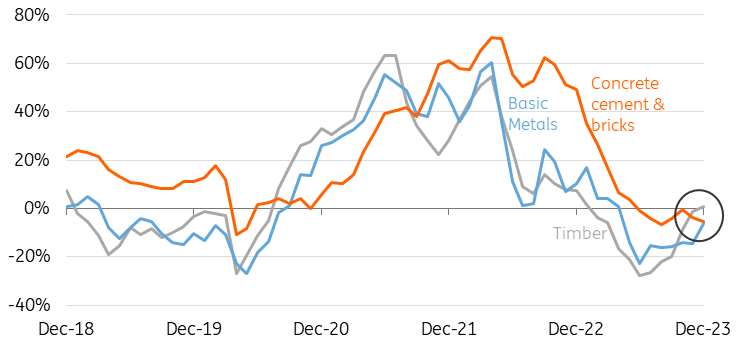

Concrete, timber, plastics and steel prices are declining

Producer Price Index, Index January 2020=100, European Union

Prices of concrete, cement and bricks remain sticky

Building materials such as concrete and cement peaked during the summer of 2023 and have only undergone a marginal decline. The cost of these materials has benefited from declining energy prices as these are very energy-intensive to produce. You might expect significant price drops here, too, not least because demand from contractors is declining as new construction volumes decrease. Yet, output prices of these building materials have only come down marginally, by less than 1% in November 2023 compared to half a year earlier. And here are two reasons why concrete, cement and brick prices remain sticky:

Other input prices shot up

As energy prices decreased, the costs of other materials, such as sand, stone and clay, rose significantly. Although these materials are abundant, environmental regulations can make quarrying difficult, for instance, which squeezes supply. The cost of these materials has increased by nearly 25% in the past two years. These price hikes are smaller than the energy price fluctuations, but they more or less offset the energy price reductions in the last year for building material production.

Clay and sand are more essential components for the production than energy. We estimate that they account for two-and-a-half times more than energy costs.

Sharp price increases of stone, sand and clay

Price development: quarrying of stone, sand and clay (Index May 2020=100)

Concrete, cement and bricks' prices are less vulnerable than timber and steel

Timber and steel prices react relatively quickly to changes in the market. If stocks of suppliers and wooden building materials increase, we can see price declines within just one to two months. The (global) market for these products is very competitive, so changing purchase prices are quickly passed on.

Building materials such as concrete and cement are heavy and voluminous. That's why they're often traded on relatively small local markets, resulting in less competition. This gives the suppliers of these products more market power, which usually results in both higher prices and lower price volatility. They do not have to pass on price reductions of raw materials or energy costs directly because of the relatively limited competition. As a result, the output prices of these products rise - and fall - at a slower rate compared to building materials such as wood, which are traded in more competitive markets.

Small price decreases expected for concrete, cement and bricks

Balance of manufactures in European Union which expects to increase/decrease output prices (over next 3 months)

Few producers expect price declines

It looks like the strong price movements in building materials has come to an end. Only a small majority of steel, concrete, cement and brick suppliers expect to lower their sales prices. However, for metals shipped in containers, the Red Sea conflict poses an upside risk. The price fluctuations for timber also seem to be over. On balance, less than 1% of EU timber companies planned to increase their prices in December 2023.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more