Why is the Riksbank thinking about ‘hedging’ its FX reserves?

Alongside a 25bp rate hike and faster quantitative tightening, Sweden's Riksbank said yesterday it would consider ‘hedging’ FX reserves. Hedging FX reserves is difficult to conceptualise, but the central bank has done a good job of explaining its thinking. If approved, it could be selling $6bn through the $/SEK forwards market this autumn

Hedging FX reserves?

One does not often hear of a central bank wanting to hedge its FX reserves. As the Riksbank admits, FX reserves are there to deliver i) FX liquidity support to the local banking system, ii) meet its commitment to the IMF, and iii) FX intervention. So why on earth would a central bank want to be hedging a stock of highly liquid, highly rated FX assets which are held for financial stability purposes?

The answer to that question, ironically, is financial stability purposes. But we're talking about the financial stability of the Riksbank itself, rather than the local financial system. At the heart of the story is the issue of the revaluation of its FX reserve portfolio running through the balance sheet.

Last year, the Riksbank’s annual report showed balance sheet losses of around SEK80bn ($7.5bn) largely driven by sharp falls in the prices of government and covered bonds acquired during various bouts of quantitative easing. Of course, the Riksbank was not alone here; the Swiss National Bank (SNB) lost a staggering CHF132bn ($138bn) given the huge size of its balance sheet relative to GDP.

But why is the Riksbank considering hedging its FX reserves when the SNB is not? This looks to be a function of risk appetite. A few years ago, the Riksbank took the decision to switch to self-funded FX reserves instead of receiving around half of its FX reserves from the Swedish National Debt Office (SNDO). Those FX reserves had been generated through regular SNDO FX debt issues.

The trade-off for self-financed FX reserves was that i) it removed debt refinancing risk and separated the Riksbank’s and the SNDO’s balance sheets, plus improved Sweden’s debt to GDP ratio against ii) the Riksbank taking the losses through its balance sheet should the FX reserve portfolio suffer large losses. At the time, the Riksbank felt that it had large enough buffers of loss-absorbing equity capital and took the decision to switch to a self-financed reserve model.

The problem it seems is that last year’s heavy losses in its bond portfolio made a big dent in its loss-absorbing equity capital. Going forward, the Riksbank remarks that a recovery in the Swedish krona back to early 2022 levels would deliver a SEK60bn loss on FX reserves. We are not accounting experts here, but the accounting footnotes in the annual report suggest that an unrealised loss that is larger than the gains in the revaluation account (currently SEK48bn from prior years' FX reserve gains) would have to be run through the profit and loss account. Why the Riksbank is more sensitive to equity capital losses than other central banks we are not so sure, but that is the core message coming through in their communication.

This is not disguised FX intervention

When this story broke yesterday, some questioned whether it was some disguised form of FX intervention to support the weak krona. The context here is a krona at record lows and a Riksbank now firmly of the opinion that current EUR/SEK levels are a problem for the Swedish economy.

However, the Riksbank has only announced an inquiry into the issue of currency hedging – through FX forwards and FX swaps – and is not looking at outright sales of its FX reserves. Those reserves will still be there and available for use.

Instead, we read the announcement at face value – namely a measure to improve financial stability by protecting the Riksbank’s balance sheet.

The SEK is very undervalued on ING's medium term BEER* model

The main message and some market implications

Perhaps the strongest message from this announcement is that the Riksbank thinks the Swedish krona is going to rally and is prepared to take action. By currency hedging FX reserves, the Riksbank is prepared to forsake any re-valuation upside and protect against the devaluation downside of its FX reserve portfolio falling against the krona. We agree that the krona is very undervalued on a medium-term basis, but remains vulnerable over coming months as long as interest rates are going higher and Sweden’s real estate sector is exposed.

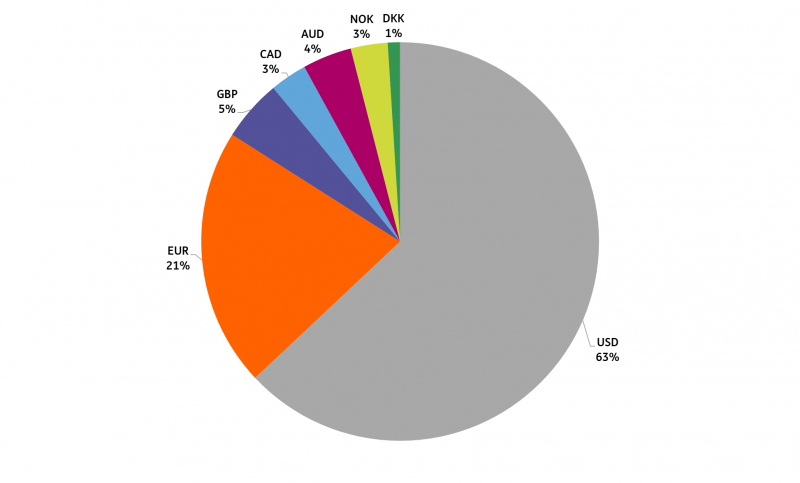

In terms of some practical implications, the Riksbank has said that it is starting an inquiry into currency hedging and will have concluded its work by the early autumn. If it goes ahead it has said it will be looking at hedging around 25% of its SEK400bn FX reserve portfolio. The Riksbank has also said that 63% of its FX reserves were in dollars at the end of April. Using current USD/SEK exchange rates, that could mean that the Riksbank will be looking to hedge around $5.8bn of its dollar exposure and $9.2bn of its total FX exposure from this autumn onwards. Typically a currency hedge on such exposure could be enacted through, for example, selling USD/CHF three months forward and rolling it.

In its various press releases, the Riksbank has said it could be looking to hedge its FX reserves via the FX forward and FX swap market. Presumably, the Riksbank would want to scale into any hedges to avoid disrupting the market, but $6bn would be a lot to put through the FX spot and forward markets – where Scandinavian FX markets have long suffered for lack of liquidity.

Depending on the state of the global and SEK markets at the time, an early autumn decision to push ahead with currency hedging of reserves could well have an impact on the SEK spot and forward markets e.g., weighing on spot USD/SEK and narrowing the three month forward points, which currently stand at around five big figures.

The currency composition of Sweden's SEK400bn FX reserve portfolio - as of April 23.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more