What will OPEC+ do?

- 29 November 2019

It’s that time of year again, with OPEC+ set to descend on Vienna for their semi–annual meetings on 5-6 December. There is growing consensus that OPEC+ will need to take further action going into 2020, and the outlook for the year ahead will depend largely on what they agree

How has OPEC performed?

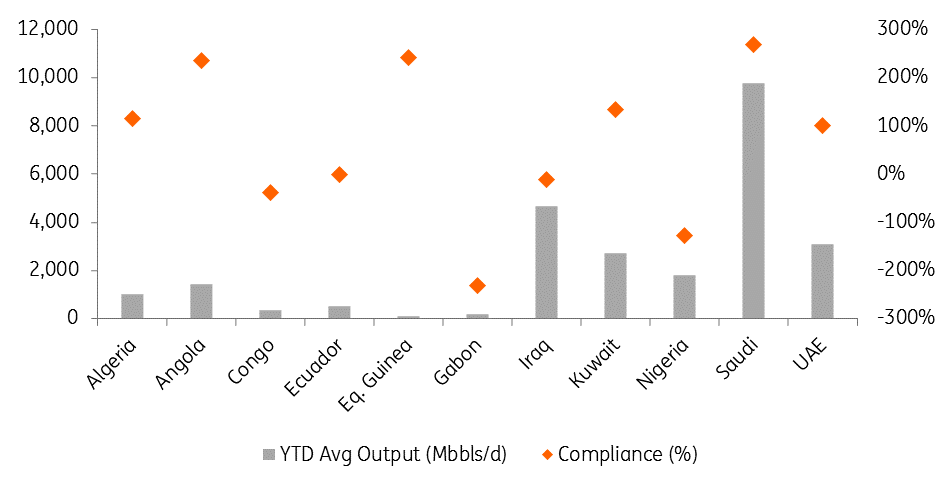

OPEC as a group has done well this year, sticking with their production cuts. Year-to-date, OPEC compliance has reached around 137%. This strong overall compliance does however mask the lack of individual compliance by some members. Saudi Arabia has carried the deal, producing around 500Mbbls/d below their agreed quota, which has helped to tighten the market. This has made up for some of the poor compliance seen from the likes of Nigeria and Iraq. Over the course of this year both countries have in fact increased oil output. If we were to assume that Saudi Arabia produced at its quota level this year, compliance for OPEC-10 would have been just 70%. Moving forward, there will be pressure on these two nations to comply. It would be hard to imagine other producers even contemplating deeper cuts, when Iraq and Nigeria have produced a combined 280Mbbls/d in excess of their quota level year-to- date.

Non-OPEC member Russia has also struggled to fully comply with the deal. Output over the first 10 months of the year averaged 11.25MMbbls/d, leaving compliance down at just 76%. There have been more recent reports that Russia wants to discuss the way its cuts are calculated. Russia includes condensate production in its crude oil production number. However, with strong growth in gas output, condensate production has also increased, making it difficult for Russia to comply with the deal.

The largest OPEC declines have come from a member who is exempt from cuts. Iran has seen oil production fall by around 1.17MMbbls since October 2018- the reference month for cuts for those members in the deal. The driver behind this fall has been the effectiveness of US sanctions limiting exports of Iranian oil. Looking to 2020, we expect that Iranian output will remain stable at around 2.1MMbbls/d.

Turning away from supply, a factor which has made the life of OPEC+ even more difficult is the disappointing demand growth seen this year. At the start of 2019, it was forecast that demand over the year would grow by 1.4MMbbls/d, while now the IEA is estimating that demand will grow by just 1MMbbls/d. This slowdown shouldn’t come as too much of a surprise with ongoing trade uncertainty, coupled with the slowdown that we have witnessed in a number of economies.

Despite tepid demand growth, OPEC+ has managed to draw down global inventories by almost 1.8MMbbls/d over 3Q19, and we estimate that inventories will decline by around 500Mbbls/d over 4Q19.

OPEC compliance over 2019

The 2020 outlook

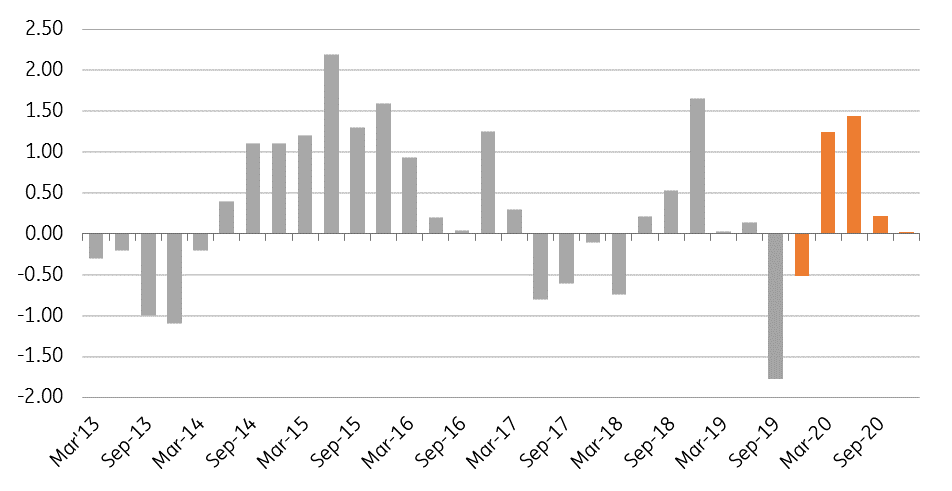

Looking ahead to 2020, and the stock draws that we have seen for much of this year are expected to reverse in 1H20, despite the fact that the current OPEC+ deal is set to expire only at the end of March 2020.

Currently our balance sheet is showing that the market will see a surplus in excess of 1MMbbls/d over 1Q20 and around 1.4MMbbls/d in 2Q20. While an extension to cuts will help to deal with a large part of the surplus in 2Q20, it does little to help the surplus over 1Q20. In order to eat into this, we will need to see stronger compliance and deeper cuts.

However a key assumption for this surplus is that US oil production will grow by close to 1MMbbls/d over 2020. Given the slowdown that we have seen in drilling activity this year, there is growing uncertainty over how strong US production will in fact be over the course of next year. Lower than expected US production growth over 2020 is a key upside risk for oil prices.

Quarterly global oil market balance (MMbbls/d)

How will OPEC+ respond?

Uncertainty around US production growth does make the decision for OPEC+ more difficult in terms of how much longer and deeper they would need to cut. In the current macro environment, they would not want to over cut, as this does raise the risk of demand destruction.

We believe that OPEC+ will agree to extend the current deal through until the end of June 2020. It becomes a lot more difficult to judge whether they will make deeper cuts over 1Q20. Our balance sheet suggests they need to, but it is hard to see which producers would be willing to cut more. Oil companies in Russia are keen to keep the deal as it is for now, and postpone any potential decision until March.

If other producers are able to get some reassurance that non-compliant members will step up their game, then there may be some room to cut more, but it will be a struggle to cut as much as our balance suggests is needed.

What does this all mean for prices?

The outlook for prices over 2020 will depend largely on the outcome of the OPEC+ meeting. Leaving the deal as is would likely put significant pressure on prices, and we would not be surprised if ICE Brent trended towards the US$50/bbl region in the short term under this scenario. An extension of the current deal through until mid-2020 would also likely see downward pressure on prices in 1Q20. In order to keep ICE Brent trading around the US$60-65/bbl area in the near term, we believe we would need to see deeper cuts- possibly as much as 1MMbbls/d.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more