What we think the Bank of England will do next in four charts

- 27 September 2017

- United Kingdom

The Bank of England may be keen to exit emergency mode, but a big series of rate hikes is unlikely

November hike looking likely, but don't expect much after that

The Bank of England's increasingly hawkish tone means that a rate hike increasingly looks like a question of "when" and "how much", rather than "if". And on the former, the choice of the phrase "next few months" to describe rate hike timing puts November firmly on the table. However, Brexit, borrowing and a lack of domestically-generated inflation mean we're not expecting a rate-hike run.

It seems the Bank is very keen to get out of "emergency mode" as the initial shock of Brexit subsides. It also seems that the committee is taking a leaf out of the Bank of Canada's book, by taking a more forward-looking approach to policymaking given the lags involved with tightening policy. But there's also likely a desire to avoid being left in the dust by the global race to tighten policy, as a result amplifying the pound's weakness.

But whilst we're now pencilling in a November hike, we think the chances of a series of hikes thereafter are low. Here's why...

Economic outlook still points to ongoing sluggishness

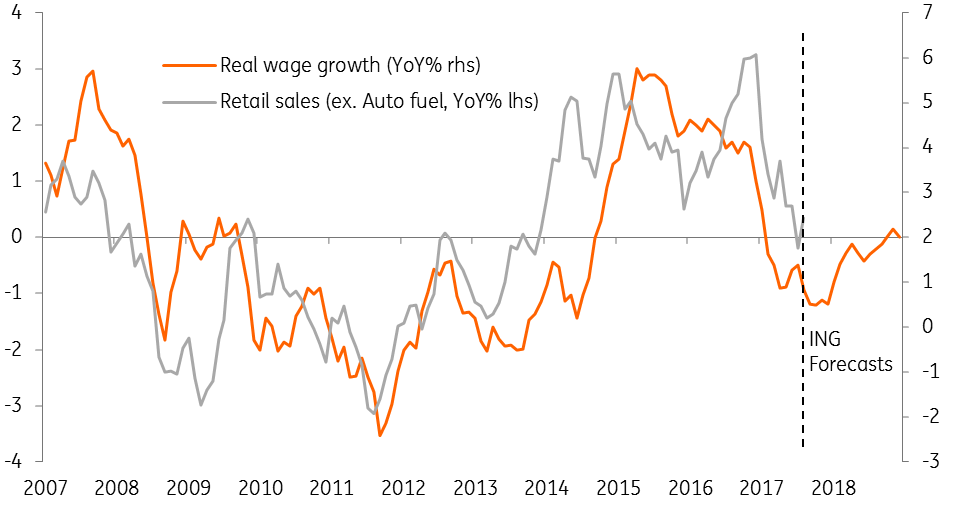

When it comes to the Bank of England, the thing that has analysts and investors scratching their heads is the fact that the economic outlook has not changed noticeably in recent months. The Bank has pointed to a tentative pick-up in wage growth of late, but we suspect this may just be the unwinding of some temporary factors that the BoE has previously pointed to, such as the apprenticeship levy and pension changes. With growth still sluggish and cost bases rising for firms via higher import costs, we doubt wages will takeoff from here - or at least not to the degree the Bank forecasts.

The household squeeze also still appears to still be hitting consumption, despite a tentative pick-up in retail sales in August. And whilst the real wage squeeze may have reached its worst, the gap between headline inflation and wage growth looks set to stay fairly wide into early next year, keeping pressure on spending.

So at this stage, there's certainly a risk that economic and wage growth misses the Bank's forecasts, meaning any steps towards higher rates will be, at least initially, fairly tentative.

Few signs of inflation once currency impact stripped out

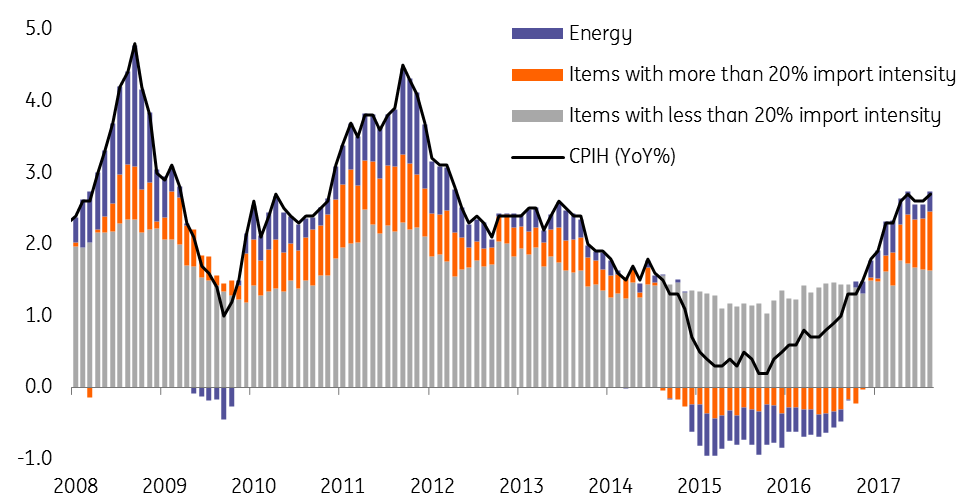

Bank of England hawks often point to having "limited tolerance" to above-target inflation this year. But if the inflation basket is deconstructed by import intensity - that's the proportion of a particular good that is based on imports - it's clear that without the effect of oil or sterling's fall, inflation would be noticeably lower.

Like all measures of core inflation, It's not 100% foolproof - certain things, like airfares, have a low import intensity but are highly sensitive to the pound's value. But it's a decent enough rule of thumb and in this case suggests that core inflation would be just 1.6% without the pound's depreciation.

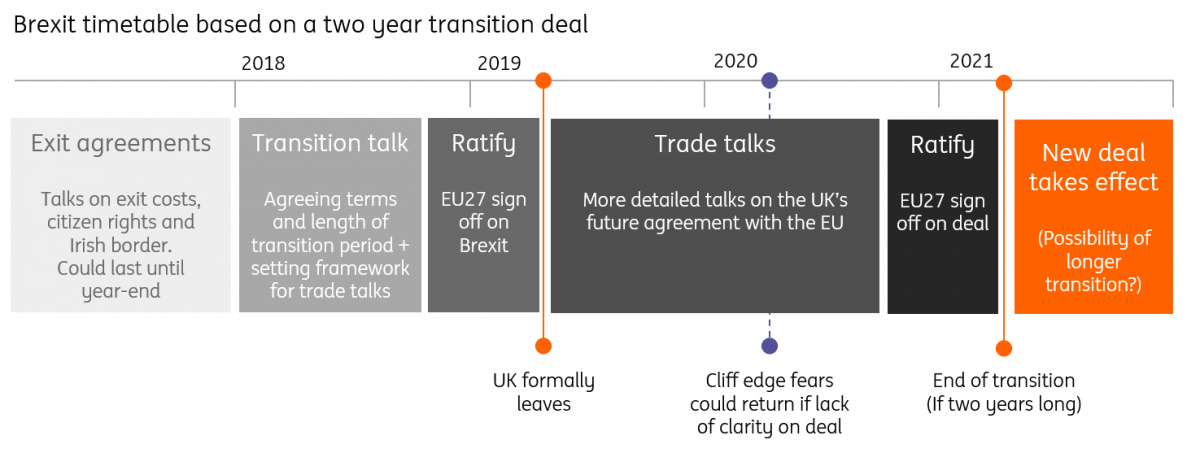

Brexit uncertainty still elevated, despite transition deal hopes

The fact the UK government is increasingly coalescing around the idea of a two-year transition deal could help unlock some hiring and capital spending by firms.

That said, there are still plenty of obstacles to be overcome in the negotiations before a transition period is signed and sealed. Without concrete agreement on the trading environment and length of the transition, some firms will inevitably have to remain cautious. To take one example, the airline industry will want clarity very soon on their ability to continue flying freely between the UK and Europe if they are to start planning schedules, hiring and selling tickets for 2019.

There's also a risk that cliff edge fears could still make a comeback. In the same way businesses will need advance warning of the form the transition will take, they will also need to know what the UK's ultimate trading relationship will be well in advance of the transition coming to an end. If the post-Brexit overlap is indeed two years, then this deadline could come into focus pretty quickly after the UK formally leaves the EU in 2019 - though of course the transition timeframe could be longer or extended.

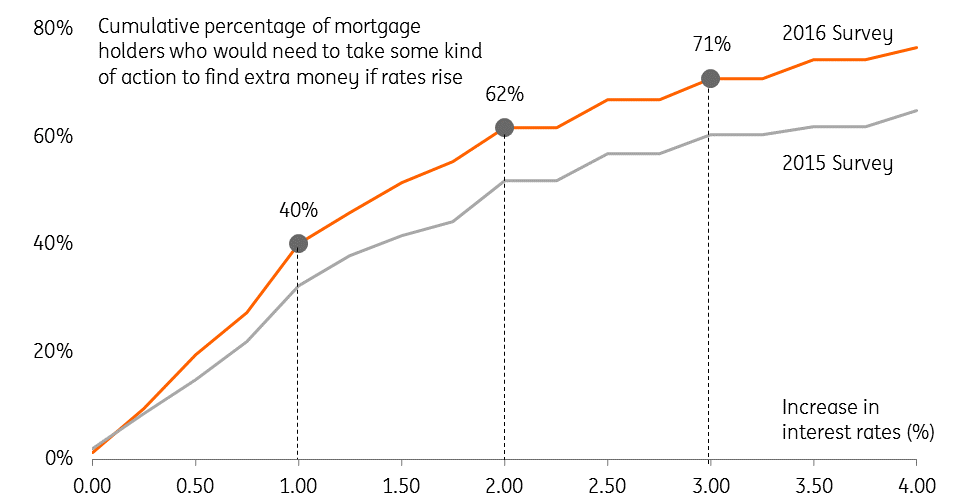

Household borrowing a key reason to tread carefully

Consumer spending has been on a rollercoaster ride since Brexit - surging into the end of 2016 before coming to a standstill in the first half of this year. But there's been one constant through all of it: borrowing. Unsecured lending, fuelled in no small part by car financing, has continued to rise at a near-10% rate and has underpinned spending as real incomes have fallen.

This a major consideration when hiking interest rates. A survey by the Bank of England at the end of 2016 found that 40% of variable/tracker mortgage holders would need to take "some kind of action to find extra money" if interest rates rose by 1% from current levels. With consumer spending already fragile, the Bank will be keen to tread carefully as it begins hiking rates

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more