What to expect from June’s Fed minutes

- 5 July 2017

- United States

The major risk is that the Fed signals when it will start unwinding its balance sheet

Release time

The Fed will release its June minutes at 1900 BST (2000 CET) on Wednesday 5 July

When the balance sheet unwind will begin

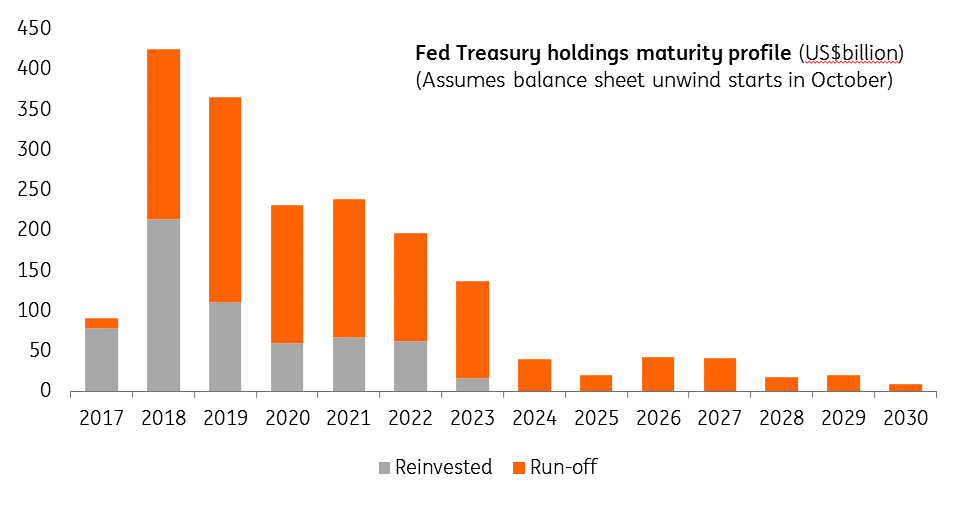

We learnt at the June meeting that the Fed will unwind its balance sheet by allowing a capped amount of treasuries/MBS to roll off the balance sheet each month.

The plan is to start the process with US$10bn per month in balance sheet shrinkage – US$6bn from Treasuries, US$4bn from agency & MBS – rising by similar amounts at three-month intervals over 12 months until the monthly ‘caps’ for Treasuries and MBS reach US$30bn and US$20bn, respectively.

We expect the Fed to start unwinding the balance sheet in December

The only real remaining question is when, and there's a risk that we get the answer in today’s minutes. The Fed has moved faster than many thought on releasing its plan, and there have been some suggestions that the process could commence as early as September.

But while we certainly wouldn't rule this out, we think the Fed will look to get another rate hike under its belt in September before commencing the balance sheet unwind in December.

This is partly because the Fed is keen to get the Fed funds rate comfortably above zero before unwinding its balance sheet. This maximises the room they have to add future stimulus via rate cuts, rather than reverting to abruptly pausing balance sheet reduction - thereby keeping the shrinking process "passive" and "predictable".

How the unwind will alter the Fed's treasury maturity profile

How many times the word "transitory" is used

"Transitory" is the Fed's latest buzzword and was used a whopping nine times in the previous set of minutes to describe the weaker 1Q GDP and recent inflation readings.

On growth, it's hard to disagree. Business surveys remain robust – the strong pick-up in the manufacturing ISM index providing the latest example – and the higher frequency spending data points to 2Q GDP growth in the 3% region. It also looks like the first quarter fell foul of the perennial "residual seasonality" issue - whereby the seasonal adjustment factors applied at the start of the year appear to over-depress growth figures.

When it comes to inflation, however, the "transitory" argument has looked less compelling recently. The Fed's preferred core PCE inflation measure has come off a cliff in recent months, hitting 1.4%, and wage growth has also lost some traction of late.

We're still relatively optimistic that both will turn around. The 7% fall in the dollar since December is likely to keep the pressure on core inflation. We also think it is a matter of time before the tight labour market exerts further upward pressure on wages.

But this is likely to take time, and that means that markets are likely to remain sceptical about the Fed's hiking ambitions right up until the September meeting. Expect the Fed to navigate this issue in part by citing other factors – chiefly the recent easing in financial conditions and “rich” asset valuations – as extra justification for hiking.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more