What now for tax cuts after Trump’s healthcare failure?

- 19 July 2017

- FX Healthcare United States

Failure to repeal and replace Obamacare means tax cuts are likely to be delayed and diluted, putting more pressure on the USD.

What has happened?

Donald Trump’s efforts to repeal and replace Obamacare have failed. Republican Senate majority leader Mitch McConnell found himself short of the votes needed to get it passed and instead took the decision to repeal only, but with a two-year delay. In theory, this should give Republicans enough time to come up with the healthcare replacement that has so far eluded them. This will be voted on “in the coming days”.

Here, we look at the political knock on effects for tax, the Fed and the dollar.

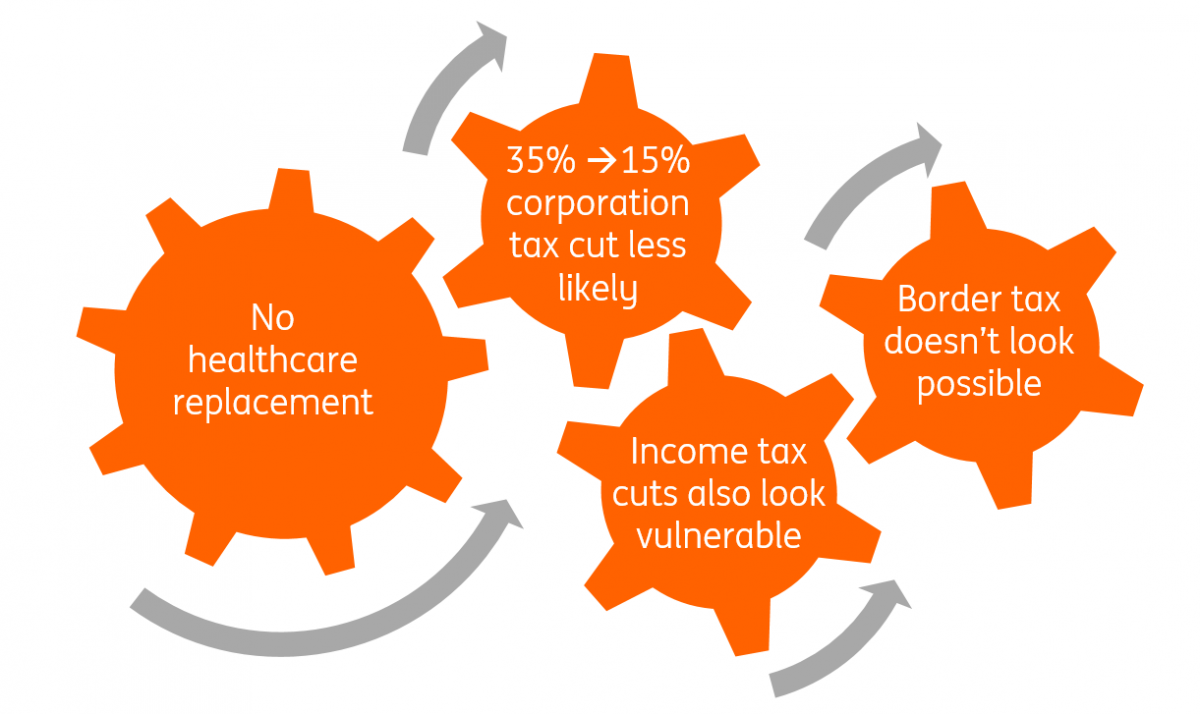

Healthcare reform matters for Trump’s tax plans

Given Donald Trump’s linking of healthcare reform with “meaningful” tax cuts, this development suggests that there is less scope for aggressive fiscal stimulus being approved in the near-term. At the very least it implies a dilution and delay. After all, healthcare reform was meant to save money that could help fund tax cuts.

Knock-on effects for tax

What are the challenges?

Healthcare and tax reform were President Trump’s two big action points. Failure on the first is likely to embolden opponents while hurting the credibility of the administration, which is already seeing plunging poll ratings. Former Republican Senate majority leader Trent Lott said defeat is a “blow to governing”.

At the very least this implies a dilution and delay to tax reform

Tax reform is going to be just as divisive within the Republican Party as healthcare reform. Some Republican moderates are unhappy about tax cuts for the wealthy while cutting spending on programmes that are essential to their constituents.

Meanwhile, fiscal hawks are concerned if tax cuts are not funded fully then it could lead to higher government fiscal deficits, which they will oppose. This is despite administration officials suggesting the tax cuts will be so stimulative that the additional economic output they generate will increase the taxable base, which will offset the effects of lower tax rates.

Adding to the complications is the Congressional Budget Office estimate that the US will hit its debt ceiling in October, which could make fiscal hawks more obstinate. It is also important to remember that the tax bill would not qualify for a simple majority if it is expected to add to the deficit over ten years. Therefore, it would need Democrat support or the tax cuts would need to be temporary.

Trump will want to get fiscal policy sorted before the mid-term primaries

What about timings?

Now that healthcare is not going to progress, there is the opportunity to produce a tax bill by September. There is the risk of a lengthy discussion, as with healthcare, but there appears to be a consensus that it could get approval late 2017/early 2018 assuming the challenges already mentioned can be overcome.

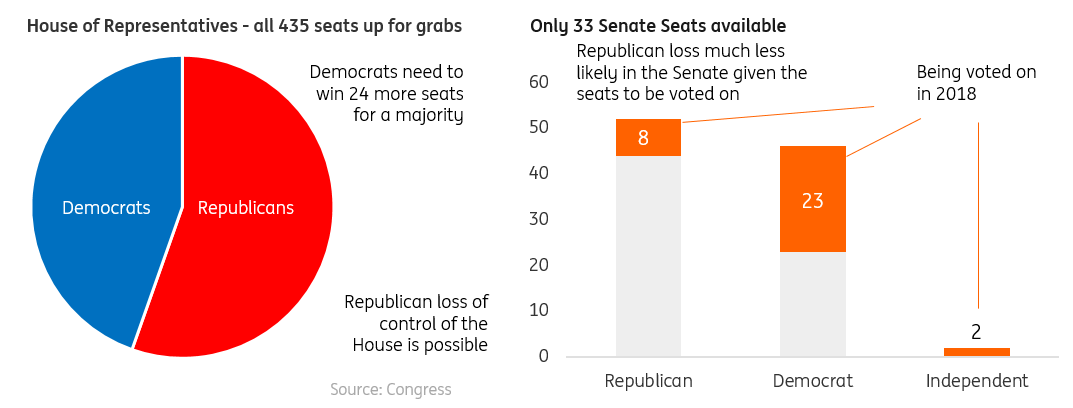

It has to be done before the primaries ahead of the November 2018 mid-term elections. Given President Trump’s low approval rating, which is unlikely to be improved by the healthcare failure, he will want to see action on tax.

Otherwise, he may feel there is the real threat that Republicans might lose the majority in the House, which would severely limit his ability to pass legislation in the second half of his Presidential term.

Mid-term elections: Healthcare & tax troubles could make life harder for Trump

December Fed hike looks more likely

President Trump has pinned his hopes of strong growth on meaningful tax cuts so if they are going to be smaller in magnitude; then growth forecasts will be lowered.

However, over recent months there has been creeping doubt over their likely timing and scale, including within the Federal Reserve. As such, it is unlikely to alter the market’s outlook for the path of Fed policy given it was already extremely doubtful of the Fed’s own prediction of four 25bp rate hikes between now and the end of 2018.

We are still forecasting three 25bp rate rises, but it makes it more likely that the next Fed rate hike will be in December rather than September. It should not necessarily impact on the timing of the Fed’s balance sheet reduction programme, which could start as soon as September.

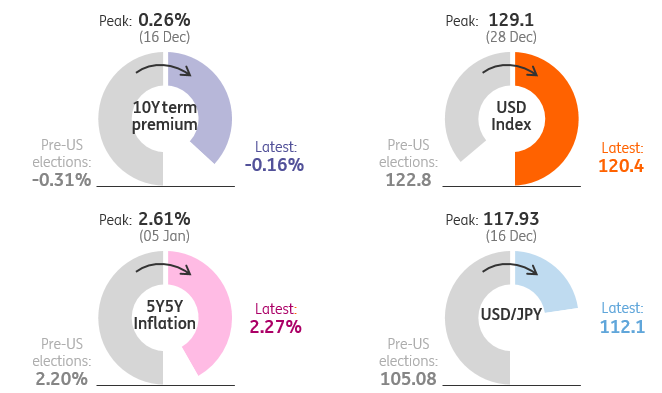

US bond markets seem to have little faith in ‘Trumpflation’

Markets have all but priced out any hopes of US fiscal stimulus coming through in 2017 and the narrative seems to be that this is more of a 2018 story, if anything. Of concern is the negative term premium on the US 10-year yield and lower long-term inflation expectations – both suggest that we have returned to the status quo ‘lowflation’ world we had been familiar with in the US economy before last year’s Presidential elections.

The USD is likely to remain on the back foot

The USD’s fall from grace has been quite spectacular, with the trade-weighted index now below pre-Trump levels. As the rest of the world plays monetary catch-up, narrower interest rate differentials – as well political troubles at home – means that the USD is likely to remain on the back foot. Having said that, things look to have overshot in the near-term, and there is a chance that markets are currently overly pessimistic on the US – and too optimistic on recovery prospects elsewhere. A bit of a ‘normalisation’ in expectations could put a floor under dollar selling.

Our US reflation dashboard

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more