Germany’s housing slump finally looks to be ending

- 22 March 2024

- Real estate Germany

The German housing market seems to be bottoming out following a particularly sharp correction in real estate prices in 2022 and 2023. The recovery, however, looks set to be gradual

Interest rates are the main driver of housing market developments

Data on house price developments in Germany published today, Friday, illustrate the effect that the rise in financing and living costs - and the fall in demand for housing loans - has had on the German housing market. We'll get to that detail in a moment, but first some context.

As in many countries, Germany saw a significant rise in mortgage rates, and financing costs soared. At the same time, the cost of living also increased significantly, and wages just didn't rise fast enough to compensate for high inflation for a long time. As a result, affordability went well below the levels seen over the past decade, and demand for housing loans fell rapidly, down 9% Year-on-Year in 2022 and 37% YoY last year.

When interest rates are rising, the property market is usually one of the first markets to react, and that's what we've seen. Leading up to the actual first ECB rate hikes in July 2022, bond yields and mortgage rates started to increase. In July 2022, mortgage interest rates had already increased by almost 150bp, compared with January of the same year, when they stood at 1.4%. In November 2023, the average interest rate for a housing loan in Germany was 4.3%, the highest level since 2009. And although the ECB's next interest rate turnaround is just around the corner, the effects of the previous rate hike cycle are still being felt.

Average mortgage rates & demand for housing loans

More of a correction than a bursting bubble

So, to the latest data and according to the Federal Statistical Office, prices for residential real estate fell by 2% quarter-on-quarter in the fourth quarter of 2023, leading to house prices falling by 8.4% in the full year of 2023. It is the first annual price decline since 2007. Nevertheless, remember that house prices rose 30% between the second quarter of 2019 and the second quarter of 2022, so last year's decline in house prices should be understood as a correction rather than a crash.

The price of energy-inefficient properties has fallen much faster than that of energy-efficient ones

It isn't just affordability that's been playing a key role in house price falls; it's also a house's energy efficiency. Analysis of anonymised in-house data shows that while the fall in prices for energy-efficient homes with an energy label of A+ was quite limited last year at around -1%, prices for properties with the worst energy efficiency label of H fell by as much as 14%. And since the price of energy-inefficient properties has fallen much faster than that of energy-efficient ones, the price difference between properties with a good energy label and their unrenovated counterparts has also widened. Last year, a house with an energy label of A+ was around 40% more expensive than a house with an energy label of H. Back in 2021, the price difference was only 16%.

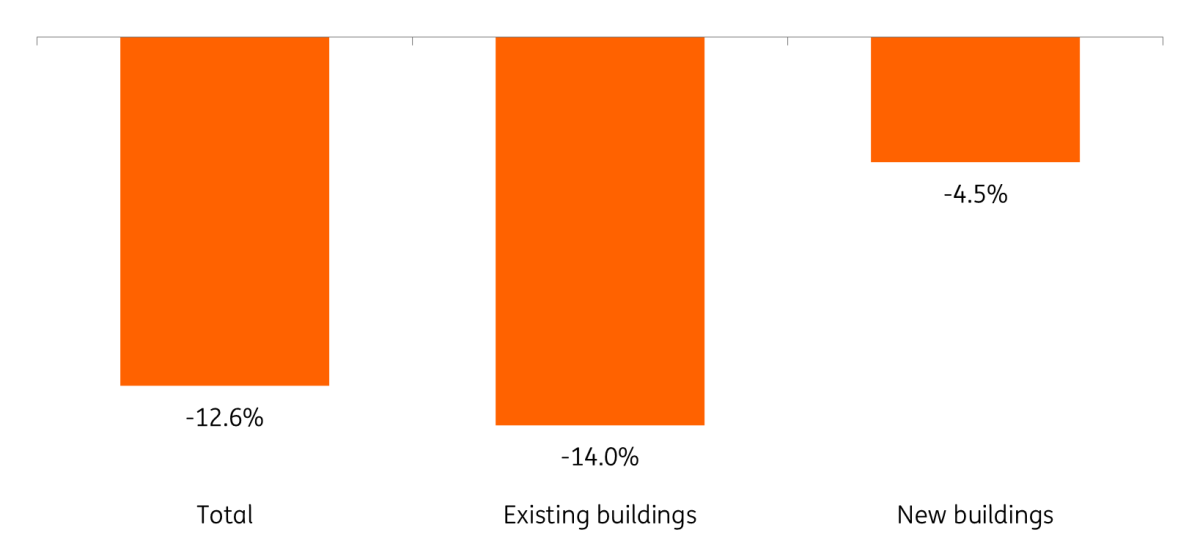

As the majority of the German housing stock was built before 1979, renovation activity has been limited in recent years, and as older buildings generally have a poorer energy label than new buildings, it does not come as a surprise that prices for existing properties have fallen faster than those for new buildings. By the end of the fourth quarter of 2023, prices for existing properties had fallen by 14% since they peaked in 2Q 2022. Prices for new buildings, which peaked a quarter later, had declined by 4.5%.

House price development up to 4Q 2023 since the respective peak

What’s next for the German housing market?

Over the past few months, the deep marks left by both high financing costs and the rise in material and labour costs of recent years have become increasingly visible.

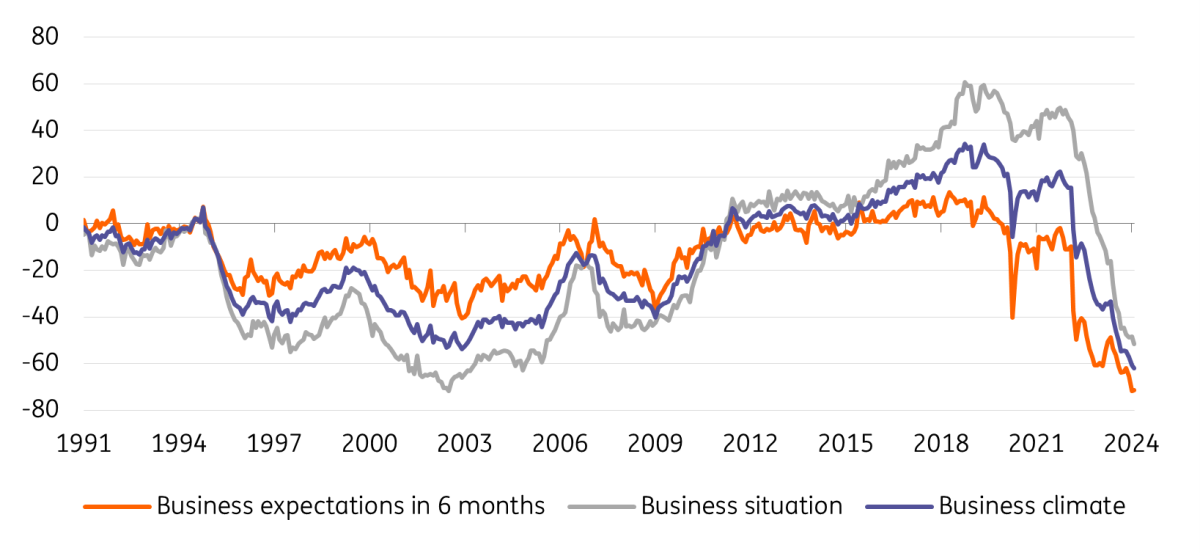

Sentiment in the residential construction sector reached an all-time low in February. The current situation was assessed to be at the worst level for almost ten years, and the expectations component continued to paint a gloomy picture for the year ahead, following an all-time low in January. Building permits for residential property have already fallen by almost 27% in 2023 compared to the previous year, and with order books thinning out and insolvencies in the sector on the rise, there is no hope of an imminent recovery.

Ifo business climate index in the residential construction sector

This tense situation in the construction sector is creating additional headwinds for the German housing market this year. It is likely to lead to a drying up of supply, which is expected to exert upward pressure on prices while also weighing on volumes. At the same time, the economic outlook remains weak and economic and geopolitical uncertainty is high. Even if real wages rise faster this year than the 0.1% increase recorded in 2023, households' willingness to spend is likely to remain limited. The propensity to save is still at high levels, which suggests that any additional income is likely to end up in savings accounts and not necessarily in real estate investments.

A strong housing market rebound is unlikely

The European Central Bank's looming rate cut cycle has already pushed down mortgage rates a little. However, we don’t expect a further easing of financing costs unless the ECB surprises with an aggressive rate cut cycle, quickly reversing the hikes since July 2022. At the same time, economic uncertainty and a small increase in unemployment could still hold back new demand for housing.

High construction costs and unfavourable affordability make a strong rebound of the entire market unlikely. Nevertheless, as the market finds a new equilibrium and Germany still has a structural deficit in housing supply, prices could rebound without a significant improvement in volumes.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more