Weak start to the year for US retail sales and manufacturing

January retail sales and manufacturing output were quite a lot weaker than expected, but we are coming off strong levels after upside surprises in late 2023. The outlook remains one of a slowing growth story as high borrowing costs, tight credit conditions and reduced support from pandemic-era accrued savings create a more challenging environment

Retail sales fall much more than expected

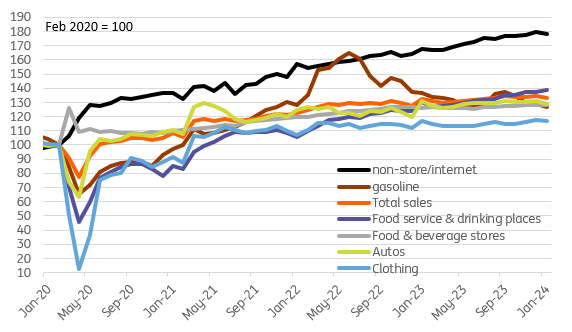

January’s US retail sales report looks soft, falling 0.8% month-on-month versus the 0.2% drop expected while December's growth rate was revised down to +0.4% MoM from +0.6%. The 'control group', which excludes volatile items such as autos, food service, gasoline and building supplies, has a better correlation with broader consumer spending trends – remember retail sales is only around 45% of total consumer spending – fell 0.4% MoM versus expectations of a 0.2% increase. With inflation coming in on the hot side earlier in the week, this implies consumer spending fell in real terms in January, which would be the first decline since August.

Looking at the details, the only components to post an increase in retail sales were furniture (+1.5%), food (+0.1%), department stores (+0.5%) and eating & drinking out (+0.7%). Autos fell 1.7%, which we had a good handle on due to the fall in volume sales already reported with lower gasoline prices prompted an identical sized fall in that component. Clothing and sporting goods both fell 0.2% with electronics down 0.4% and building materials falling 4.1% MoM. Even non-store (largely internet only stores) saw sales fall 0.8%.

Retail sales levels Feb 2020 = 100

More headwinds for the consumer

In terms of the path for consumer spending, we are a little nervous that pandemic-era accrued savings will provide less support this year as they are increasingly exhausted by households while consumer credit growth is slowing sharply as higher auto loan and credit card interest rates bite. This means the spending growth will have to be driven by incomes and if inflation is still running hot, spending power may not grow very much – note the cost of living adjustment for social security payments rose 3.2% in 2024 versus 8.7% in 2023 (impacting 71mn Americans) and minimum wage payments rise on average around 3% in 2024 in the 22 states that are increasing their minimum wage this year. Falling quit rates also imply slowing wage growth. We aren’t expecting a collapse, but a slowdown in spending growth looks likely.

Meanwhile, initial jobless claims came in lower than expected at 212k last week (consensus and the previous reading was 220k) while continuing claims rose to 1895k from 1865k (consensus 1880k). Anecdotally we are hearing of more lay-off announcements from major companies while the Challenger lay-offs series is also rising quite quickly, but this isn't showing up in the data as yet. These official claims numbers still suggests a cooling, but not collapsing labour market.

Industry sends mixed signals

Finally, we have had a couple of February regional manufacturing indices – from the New York and Philadelphia Fed regions. Both bounced back after recent weakness, but the implication nationally is probably minimal. This is a volatile series and had painted a much bleaker picture than the national ISM index reported in January – it rose to a 15M high. But that decent outcome hasn’t been reflected in today’s January industrial production report. The manufacturing sector certainly started the year on a weak footing with output falling 0.5% MoM versus expectations of a flat outcome – we had seen a bit of downside risk here due to falling hours worked. Mining output fell 2.3% MoM, but utilities output jumped 6% so in aggregate industrial production fell 0.1% MoM. This was weaker than the 0.2% consensus forecast while December's output was revised down a tenth of a percentage point to flat output. Weak consumer and industrial activity isn't great news, but somewhat counter-intuitively the strength seen in November and December will still help deliver a decent quarter-on-quarter annualised GDP growth of around 2% in our view.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more