Weak pricing in Czech industry among mounting uncertainty

Soft pricing in the Czech industry, along with increased global uncertainty, could lead to delayed investments and more modest wage increases. Meanwhile, prices in agriculture continue to grow. A rate reduction in May is likely, given the risks to global expansion having repercussions for the Czech economic outlook

Subdued industrial pricing likely to dent profit margins

Industrial producer prices dropped by 0.3% in March on a yearly and monthly basis, weaker than the market consensus. Agricultural producer prices gained 2.2% MoM, yet their annual growth slowed down to 8.2% in March from 9.3% previously. Construction prices rose 0.6% MoM and were 3.0% higher than in the previous year. Prices of market services added 0.9% MoM and quickened in annual terms to 3.7% in March.

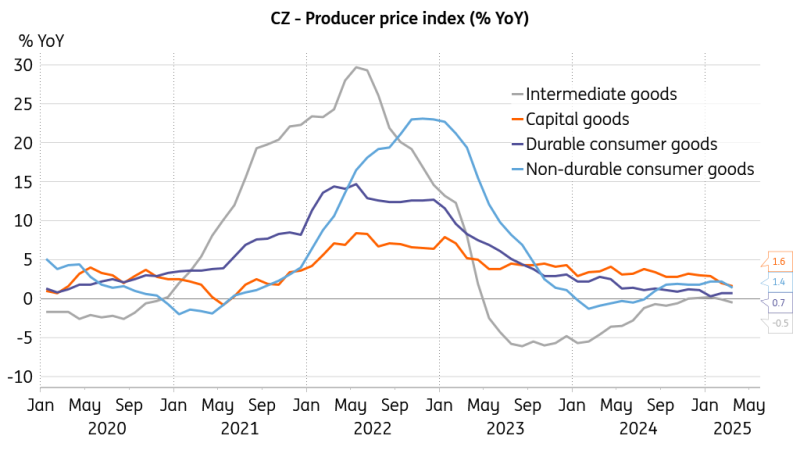

Looking at the main industry groups, prices of non-durable consumer goods gained 1.4% YoY in March while durable consumer goods prices added a mediocre 0.7% YoY. Annual growth in capital goods prices softened to 1.6% YoY, reflecting the anaemic investment activity, while prices of intermediate goods shed 0.5% YoY in line with lacklustre demand. Energy prices for manufacturers lost 2.6% YoY in March, while the annual dynamic in industrial prices without energy slowed to 0.6%, roughly half the February pace.

Intermediate goods prices suggest limping demand

The decline in producer prices indicates fierce price competition, with demand struggling to recover. The recent upheaval in global trade has heightened uncertainty, prompting manufacturers to be more cautious and make tough decisions about inventories and investment plans. Soft industry pricing is likely to squeeze profit margins and complicate the process of maintaining strong wage increases.

As uncertainty grows, the challenge of negotiating wage hikes will intensify for both employees and employers, despite a relatively tight labour market. The soft pricing in the production sector may also influence a policy rate cut at the Czech National Bank (CNB) meeting in May.

Prices in agriculture maintain growth momentum

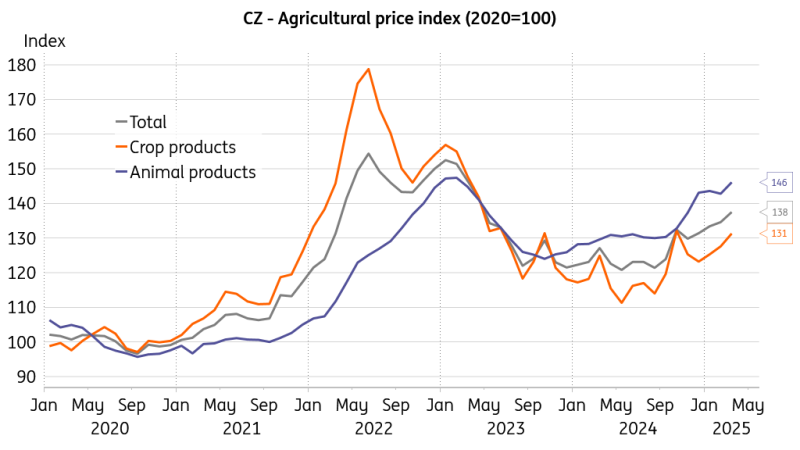

The annual price dynamic of agriculture producers eased somewhat in March, mainly due to the softer annual price growth of crop production that is more affected by shifts in seasonal patterns. Meanwhile, the price growth of animal production picked up to 12.7% annually, representing the more robust part of the overall index.

Moreover, when looking at the index level, it is obvious that prices maintained quite a robust growth momentum in March, with monthly gains recorded across all segments except for vegetables. That said, prices in agricultural production suggest that there is still quite some potential for the final consumer price tags to be lifted in the coming months despite a slowdown in the annual pace of production prices.

Agriculture prices to feed through to consumer price tags

Looking ahead, the very recent drop in Brent crude and natural gas prices will somewhat mitigate the upward momentum in food price dynamics, as transport and fertiliser costs will ultimately decline too. At the same time, prices tend to be sticky, especially when it comes to passing through reduced production costs to the consumer, also depending on the level of competition in the food retail segment, which is not groundbreaking in the Czech Republic. So, consumer food prices will be closely followed by Czech policymakers.

Growth outlook in the fog of global trade war

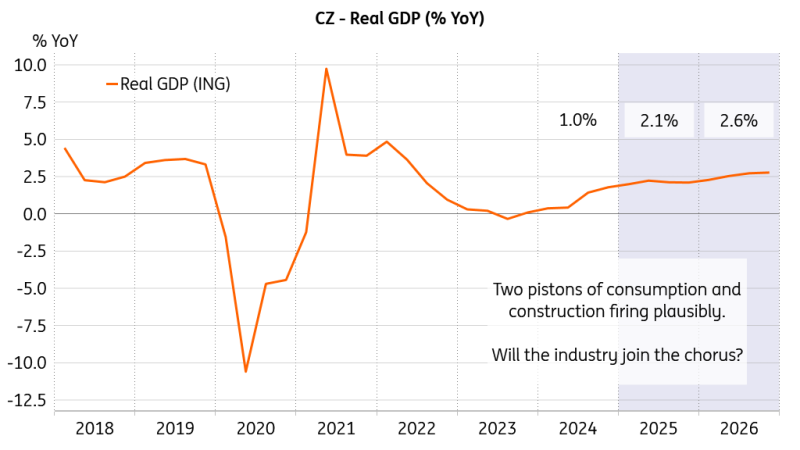

Given the recent changes in the global trade landscape, we utilise our econometric model to assess the impact on the Czech economy, primarily using US economic expansion as the key variable to indicate a negative shock.

We see a direct adverse effect of up to 0.2pp of GDP and an indirect impact via confidence channels of another 0.2pp. Keeping in mind that the tariff negotiations will carry on for some time, we have reduced this year’s Czech GDP growth by 0.3pp to 2.1% and next year’s by 0.1pp to 2.6%. This estimate may be subject to future revisions as we gain more clarity once the fog of the trade war has somewhat lifted.

Growth to remain solid despite some downward revision

After all, this is the most significant intervention in the modus operandi of global trade in decades. Whether we like it or not, we are in the midst of a negotiation process where things continuously shift until a new equilibrium is established. The willingness and skill of individual participants to navigate this reality and secure a strong position in the new framework remain to be seen, especially considering the environment is likely to be more dynamic than previously experienced.

Low investment appetite prompts cuts

Prohibitively high tariffs represent a clear risk to economic prosperity. Nevertheless, insufficient protection against unfair production and trade practices of competitors can be equally risky. That said, redundant Chinese production will likely find its way to Europe, often at dumping prices. Such a situation represents a significant risk to the Czech industrial base.

For example, considering the potential free trade agreement between the EU and the UAE poses a risk of Chinese capital producing at Indian and Pakistani labour costs and importing duty-free to Europe. Nowadays, such a type of externality has to be considered.

In any case, the cost of non-agreement is high, which should foster the motivation to set up a new and mutually beneficial trade landscape so that some gain sufficiently enough and others do not lose out too much, whether we focus on producers, traders, consumers, workers, or the state.

Incentives to postpone investments mount

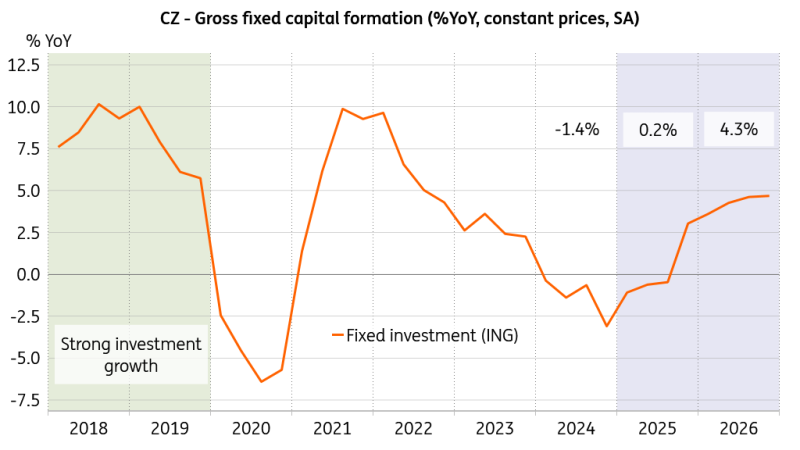

Subdued energy prices and increased uncertainty surrounding the global economic expansion pave the way to proceed with the expected rate reductions at the CNB meetings in May and August. The Czech economy is still operating below its potential, and fixed investment has remained flat for two-and-a-half years, dropping 2.4% QoQ at the end of last year.

The dichotomy between the sanguine consumer and anaemic industry gets even more obvious, and there is still space to support the investment appetite with a bit of reduced borrowing cost. Especially given the increase of overall uncertainty for the global growth outlook that may incentivise the firms to postpone their investment plans in a wait-and-see approach.

We also revise the Czech inflation projection marginally downward to 2.6% this year, mainly due to the observed steeper decline in fuel prices in March and the recently lower global Brent crude and natural gas prices. The recent appreciation of the koruna against the dollar results in cheaper imports. We apply a somewhat softer dynamic to regulated prices, as these would ultimately reflect the subdued global energy prices should these prevail. Meanwhile, the core inflation forecast remains almost unchanged, given that households would see more relaxed budget constraints due to the lower energy bills and shift the extra money to non-mandatory expenses.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article