Weak jobs report reignites prospect of imminent US rate cuts

- 1 August 2025

- United States

While jobs growth was disappointing in July, it is the huge downward revisions to May and June that have put a completely different light on the health of the US economy

| -258,000 |

Downward revisions to payrolls for May & June |

Job creation much weaker than thought

It is impossible to deny that the July jobs report is weak with non-farm payrolls rising 73k versus 104k consensus, but the most striking thing is the huge 258k downward revision to the past two months of data. June job gains, which were originally 147k are now 14k and May's initially reported gain of 144k is now 19k. This puts a completely different light on what has been happening in the US economy post the 2 April 'Liberation Day' announcements.

Contributions to US monthly change in non-farm payrolls (000s)

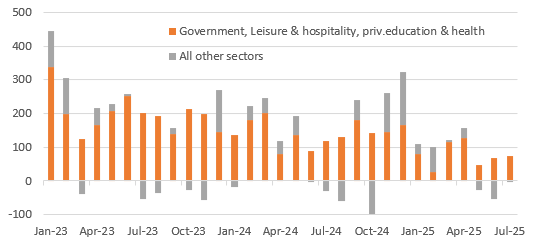

US growth engine sectors have lost jobs for three consecutive months

The details show manufacturing employment fell 11k, government fell 10k, professional business services fell 14k with, once again, all the strength in private education and healthcare services, which rose 79k.

In fact 89% of all jobs added in the past 31 months (since January 2023) have now come from private education & healthcare services, government and leisure & hospitality. All other sectors - which make up the bulk of the US economy - have been negative for three consecutive months (-28k in May, -53k in June and -1k in July) and in fact they have been negative in 13 of the past 31 months. The average monthly gain over the past 31 months has just been 18.9k for the US "growth driving" sectors.

In terms of the household survey the unemployment rate rose to 4.2% from 4.1% with employment falling 260k and the number of people classifying themselves as unemployed rising 221k. The underemployment rate rose to 7.9% from 7.7% while wage growth was broadly in line with expectations at 0.3% month-on-month/3.9% year-on-year.

September cut looks increasingly likely even with rising inflation

The mediocre headline figure for July is one thing, but the huge revisions suggest that the jobs market has lost momentum earlier than thought and the pressure from the President for Fed action is only going to intensify after this. The statements from the two Fed Governors who voted for rate cuts this week – Chris Waller and Michelle Bowman – commented that they felt the Fed was being “overly cautious” with the risk that policy is “falling behind the curve”. This sentiment is likely going to be felt more broadly within the Fed after today’s numbers, especially with tariffs set to eat into household spending power and corporate profits, thus creating a major headwind for growth.

We do have another jobs report before the September FOMC meeting and two more inflation releases, but this has reignited expectations of a September Fed rate cut - the implied pricing for a September rate cut is now back up to 20bp versus 10bp ahead of the data. If we get another soft jobs report on 5 September, we would have to expect a rate cut later that month given the Fed’s dual mandate. This would heighten the chances of follow up 25bp cuts in October and December despite a temporary rise in inflation on tariffs.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more