US: Why Georgia should be on all our minds

- 4 January 2021

- United States

The final pieces of the election 2020 jigsaw get slotted into place this week and will have major implications for Joe Biden's planned legislative agenda and the momentum of the US economic recovery

Back with a bang

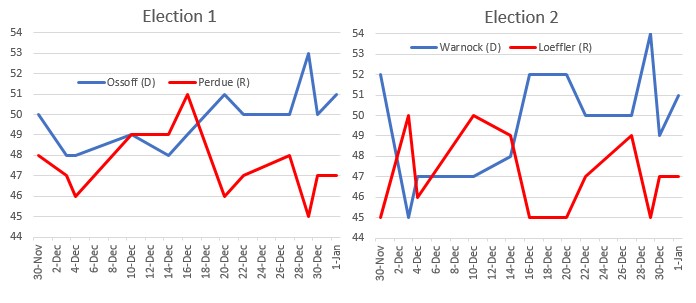

The first working week of 2021 brings the 2020 election saga to a conclusion - at long last - with Congress confirming Joe Biden’s Presidential victory. But before that, on Tuesday, we have the run-off elections for the two Senate seats from Georgia – stemming from the fact that local law requires the victor to win at least 50% of the popular vote, which no candidate achieved back in November.

Too close to call…

It will be a straight battle between the Democrat challengers and Republican incumbents in both seats. If the Democrats pull-off victory in both this will leave the parties with 50 seats each in the Senate. Vice-president Kamala Harris would then hold the casting ballot in the event of a tie on any vote. Should the Republicans win just one of the seats they would retain their thin majority.

The polls are very narrowly favouring Democrat victory in both seats, but given the margin of polling error we would have to say the race is effect still neck and neck.

Polls for the Georgia Senate elections

Critical for Biden’s plans…

The outcomes in Georgia will have massive implications for Joe Biden’s legislative ambitions. Should the Democrats win both seats they will have control of the Senate as well as the House, thereby giving Joe Biden the scope to push ahead with a broad package of policies aimed at boosting jobs, investment and green energy in the US economy.

Lose in just one and Biden will have to make compromises with Senate Republicans that could stall and limit his agenda. It would also make it more difficult for the Democrats to write into law proposals on higher taxes for corporates and wealthy households.

… with major implications for the speed of the recovery

The path of Covid and the scale and timing of economic re-opening is going to be the most critical determinant of how the US economy performs this year and next. Nonetheless, how speedily and aggressively Joe Biden can unleash his legislative programme will determine the momentum it subsequently has.

The so-called "Blue Wave" of the Presidency and Democrat control of Congress would open the door for Joe Biden to set in motion his ambitious “build back better” agenda. It would facilitate a swifter and more aggressive spending package in 2021 than can help propel the recovery more rapidly than under the split Congress scenario.

Promised tax hikes for corporates and high-income households will be implemented and specific industries will come under greater regulatory focus, but given the hugely disruptive nature of the pandemic, they would likely be eased in, rather than rapidly and aggressively enacted.

Given 2021 will see a focus on growth and regaining all the lost jobs we suspect tax hikes may be delayed until 2022/23. With the Fed assuring us of ongoing loose monetary policy, a more benign trade backdrop and the prospect of a vaccine it looks to be a recipe for very vigorous economic activity later this year.

Should the Democrats fail to win both seats the narrative of a constrained Biden returns. Given the re-emergence of fiscal conservatism amongst many Republicans this promises a less aggressive fiscal package with consequently less growth, but also less near-term debt. It also diminishes the chances of aggressive subsequent tax hikes, which would help to move the government finances onto a more solid footing. Growth would still be very robust under this scenario.

Both scenarios would of course see improved trade relations, particularly with Europe and other allies (although less so with China and Russia), than were experienced under Donald Trump. This means less disruption for supply chains relative to what businesses have faced in the past few years.

Moreover, with Covid vaccinations likely to be gaining steam the prospects of a return to normality and a full re-opening of the economy mean that the outlook for growth and risk assets in 2021 looks very positive.

Final, final confirmation of Biden’s victory

The following day a joint session of Congress, presided over by Vice President Pence, will formally count the Electoral College votes that have Joe Biden beating Donald Trump 306-232. Normally this would be a formality, but with several House Republicans and now Republican Senators Ted Cruz and Josh Hawley, amongst others, objecting in writing to the certification on the grounds of their claims of voter fraud and election interference/irregularities, it will go to a vote.

For the objection to be upheld both the House and the Senate need a simple majority, but this is unlikely to happen in the Senate based on comments from numerous leading Republicans and will certainly fail in the House given the Democrat majority there. All this does is hold up the final, final confirmation by a couple of hours.

A tricky week for markets?

With several Trump supporting groups holding protests that day in Washington the tensions in Congress could further inflame passions, especially if we do see a Blue Wave following the outcome of the Georgia elections. Potentially violent scenes at a time when Covid vaccinations are proceeding at a slower than hoped pace coupled with the prospect of weak data through the week will underline the task that President Elect Biden has on his hands.

There is the very real prospect of a soft US December labour report on Friday with surveys, such as the Homebase report and initial jobless claims, pointing to a possible fall in employment. The leisure and hospitality sectors are suffering particularly badly, as the chart below shows, with restaurants and bars forced to close while warnings about the risks from travelling are increasingly heeded by the broader population.

Homebase survey shows jobs downturn

The spike in Covid cases is looking deeply troubling too, especially with the threat of the new, more infectious mutated strain gaining a foothold, with hospitals already struggling to cope with the number of patients. We continue to see the prospect of a challenging few months which risks more Covid containment measures that will come with a significant economic cost.

So while our medium term outlook remains very positive – even more so than the consensus - we continue to see downside risks in the very near (2-4 month) term that could be somewhat challenging for financial markets.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more