US: Shock January jobs reports confounds the doubters

- 4 February 2022

- United States

The Omicron wave has depressed economic activity and this was meant to translate into weak hiring. It hasn't. 467k jobs created and massive upward revisions suggests a fundamentally very strong economy. With companies desperate to hire and the biggest issue being the lack of suitable staff, wages are rising sharply and the Fed will respond

| 467,000 |

The number of jobs created in January |

Jobs surge despite Omicron headwinds

Well, that was a turn up for the books! Non-farm payrolls rising 467k versus the 125k consensus with a net 709k upward revisions to the past couple of months. Completely out of line with belief that we could see a drop following the ADP, Manpower and Homebase surveys and the increase in initial jobless claims. The narrative was that the Omicron wave was depressing activity and hiring while the Census Bureau’s estimate that 8.8mn worker absences due to Covid would compound the risks to the downside.

It is what it is, but there will be scepticism – the BLS provide no explanation for why it is so strong. For example, the 151k increase in leisure and hospitality is hard to fathom given restaurant dining is down more than 20% on “normal” based on Opentable data. Only mining & logging (-4k) and motor vehicle and parts (-4k) saw falls. Instead, retail jumped 61k, transportation and warehousing was up 54k and professional business surveys increased by 86k.

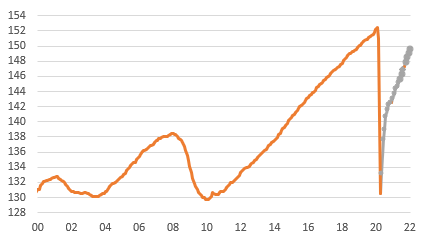

US payroll levels (mn)

The rest of the report is strong with labour participation rate rising three tenths of a percentage point to 62.2% (although still well down on the typical 63% figure reported pre-pandemic) and average hourly earnings rising 0.7% month-on-month to take the annual pay rate increase to 5.7% year-on-year. So strong activity, strong inflation pressures and this is when Omicron is holding back the economy!

The unemployment rate rose to 4%, but this reflects the jump in new entrants to the labour market given the household survey used to calculate it (separate to the establishment survey that gives us the payrolls number) showed employment rising 1.2mn.

Record vacancies suggest worker demand will continue outpacing supply

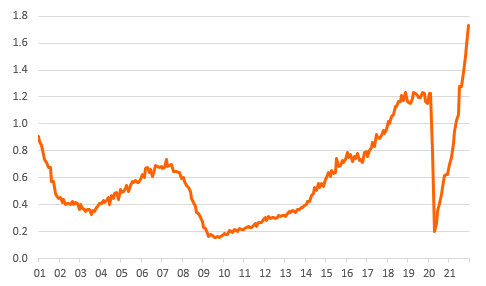

So where do we go from here? Well, we wouldn’t be surprised to see revisions lower in time, but the outlook remains very positive. In December there were 1.7 vacancies for every unemployed person in America, an all-time high as the chart below shows. This suggests the demand for workers is strong and as Covid cases and Covid caution subsides we expect employment growth to be even stronger than what we saw today – remember the first chart shows there are still 2.875mn fewer people in work than before the pandemic struck yet the economy is actually 3.1% larger.

Ratio of job vacancies to unemployed has never been higher

Wage pressures continue to build

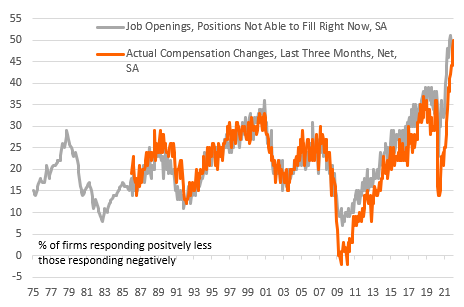

There will still be labour market constraints though with the participation rate remaining stubbornly low (not withstanding today’s improvement) and trying to fix this should be a priority. In the near term it means upward pressure on wages as companies desperate to hire pay more to attract workers while elevated quit rates mean they are also incentivised to pay more to existing staff to retain the ones they have. This was highlighted by the National Federation of Independent businesses labour report from yesterday which showed a net 47% of companies had vacancies they couldn’t fill and a net 50% raised worker compensation in the past 3 months.

NFIB surveys shows companies can't find enough workers and are paying more to attract and retain employees

More ammunition for the Fed hawks to push hard

Whether higher pay is enough to attract people back to the workforce only time will tell. Nonetheless, the narrative of intensifying labour market inflation pressures and strong employment growth when Omicron is supposedly depressing activity only makes it more likely that the Fed will embark on an aggressive series of interest rate increases. We are doubtful on the idea of a 50bp hike in March as a signal of intent to get inflation under control, given comments from officials, but fully expect five 25bp hikes this year, starting in March.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more