US resilience boosted by the insatiable appetite for tech

- 12 May

- United States

The US economy continues to outperform thanks to surging AI/tech-related investment spending and its position as a net energy producer. Nonetheless, there are signs of some stress in a few parts of the economy

Tech and high-income households continue to drive growth

The US economy posted 2% annualised growth in the first quarter of 2026, and we expect to see growth of around 2.6% in the second quarter with a decent contribution from net trade and the usual drivers of high-income household consumer spending and AI/technology-related investment.

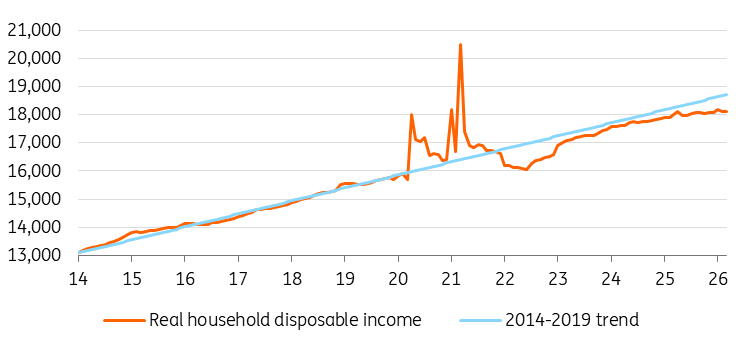

Nonetheless, consumer confidence is at or close to all-time lows, depending on the measure used, and despite the recent strength in non-farm payrolls, the US has averaged only 20k job growth per month over the past year. Real household disposable income is flatlining and higher gasoline prices are likely to create more headwinds by eating into spending power.

Meanwhile, business capex outside of technology has contracted for six consecutive quarters. So, while the US continues to post decent economic numbers, we acknowledge that it is quite concentrated in relatively small but fast-growing sectors. We see the potential for a modest slowing in the overall growth rate in second-half 2026 to around 1.8% annualised due to the headwinds tied to the economic and geopolitical headwinds being generated by the Middle East stand-off.

Real household disposable income has tailed off (RHDI chained to 2017 US dollars)

Inflation is likely to be transitory

Inflation will very likely rise above 4% at the headline level due to the higher transport fuel costs, but this is a narrower supply shock than in 2022, when global supply chains were heavily disrupted post-pandemic and the price of everything was rising.

So far, there appears to be little spillover into other inflation components and the lack of demand impetus means we are seeing this as a transitory story that the Fed can “look through”. We do not predict broad and persistent inflation that would justify higher Federal Reserve policy rates, especially with the Fed having to optimise policy for two very different goals – price stability and maximising employment.

But the Fed will have to sound hawkish over the coming months

Nonetheless, Kevin Warsh is taking over a more divided Federal Reserve with a growing element wanting to sound more neutral on where interest rates may be heading. Arch-dove Stephen Miran will be making way on the committee to allow room for Warsh, given Jerome Powell’s decision to remain on the Board of Governors for now. With longer-dated yields rising, pushing up household, corporate and government borrowing costs, we would expect a more hawkish stance from Fed officials in order to try and anchor inflation expectations and preserve the central bank's inflation-fighting credentials. A rate cut in September, which had been our call, now looks unlikely.

Assuming a gradual de-escalation that results in an improved flow of product through the Strait of Hormuz, we predict energy prices to gradually start falling back later in the year, with cooler month-on-month price increases observed within the inflation data. A better balance to energy markets in 2027 following energy inventory rebuilding in Europe and Asia means lower oil prices next year with a decent chance inflation drops below 2%. This should still allow the Fed to move policy rates that little bit closer to neutral, which we see as being 3.25%, with the 10Y Treasury yield also set to drift lower. We are predicting 25bp cuts in December this year and March 2027.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more