US politics: Trump weathers the storms

- 27 September 2019

- United States

As Donald Trump faces the biggest test of his presidency so far, we take a fresh look at the chances of his re-election in 2020. In this latest update to our in-depth report, US Politics Watch: Four Scenarios for 2020 and Beyond, we have again teamed up with Oxford Analytica to examine how the race for the White House could play out

A series of shocks over the summer leave President Trump and the Republicans lagging in the polls. Even with the Democrats moving towards impeachment, most experts still generally believe that the election is Trump’s to lose.

It is still far from clear who Trump's opponent will be. The summer failed to deliver a knockout blow to any of the key Democrat contenders, but that could soon change as the electorate assesses their responses to heightened geo-political tensions, rising economic uncertainty and controversial domestic policy debates.

Where things stand

House Democrats have called for President Trump to be impeached following reports that he withheld state aid to Ukraine before calling on Ukrainian President Volodymyr Zelensky to investigate the son of former Vice President Joe Biden.

However, the odds of Trump being removed from office (20 Republican Senator votes would be needed), or voluntarily leaving, are extremely low. President Trump thus remains set to be the Republican nominee in 2020, with his ability to win re-election reliant on a positive economy and the creation of any trade or foreign policy successes. After all, the latest developments make it even less likely there will be any bipartisan agreements in areas such as gun reform or infrastructure spending.

Other developments since our July update have offered both pluses and minuses for Donald Trump in his quest for re-election. In terms of foreign policy, the ongoing dispute with North Korea remains unresolved while tensions with Iran have been heightened following the imposition of additional sanctions after explosions at Saudi ARAMCO facilities in mid-September. The trade conflict with China has also seen little progress in terms of de-escalation, with the US imposing $125 billion in new tariffs on 1 September. New talks are due in October but there is little optimism that a formal “deal” will be agreed.

Despite these challenges, the US economy remains relatively strong. There are clearly headwinds from weaker global growth and worries about geo-political tensions, but the domestic economy is robust for now and wages are rising. Equity markets have regained nearly all of their August losses and with mortgage rates hitting new cycle lows, households are confident in the outlook and willing to spend. It is a different story in the manufacturing heartlands with the ongoing threat that weakness here spreads more broadly within the economy.

'Experts' versus the polls

Despite polling in the low 40s and facing impeachment, many experts continue to predict a Trump victory in November 2020, creating a disconnect between current public sentiment, which seems to point towards a Democratic victory, and expert predictions. Several factors explain this, including the perceived value by analysts of a strong economy in a presidential election, and some overcompensation by analysts for misjudging the 2016 election.

Incumbent presidents are generally favored to win re-election, particularly when the economy is performing well; no incumbent has lost re-election during periods of economic growth in the last 40 years. As the US economy has continued to grow during Trump’s presidency, many analysts are factoring in that performance when predicting his re-election, although they may be overestimating the importance of this, or discounting the potential that the economy will slow.

President Trump’s polling numbers also do not take into account his challenger's level of popularity. Support for President Trump could rise or fall depending on the Democratic nominee and the press this person receives. We also have to consider that some of the electorate may regard the impeachment push as a partisan attack. This could mean the Democrats actually lose some support in key swing districts while solidifying support for President Trump and boosting his campaign funding.

After incorrectly predicting his defeat in 2016, many experts are now also potentially overestimating his strengths, hoping to avoid the same mistakes made during the previous election. While hard to measure, this inherent bias against underestimating President Trump is adding to the general favored position he already occupies as the incumbent.

The Democrat race – back to where we started

While some issues- primarily enhanced national gun control legislation- have garnered support from across the spectrum, the key issues of the primary have yet to be decided; the debate between favoring electability and progressive policy priorities continues to split primary voters.

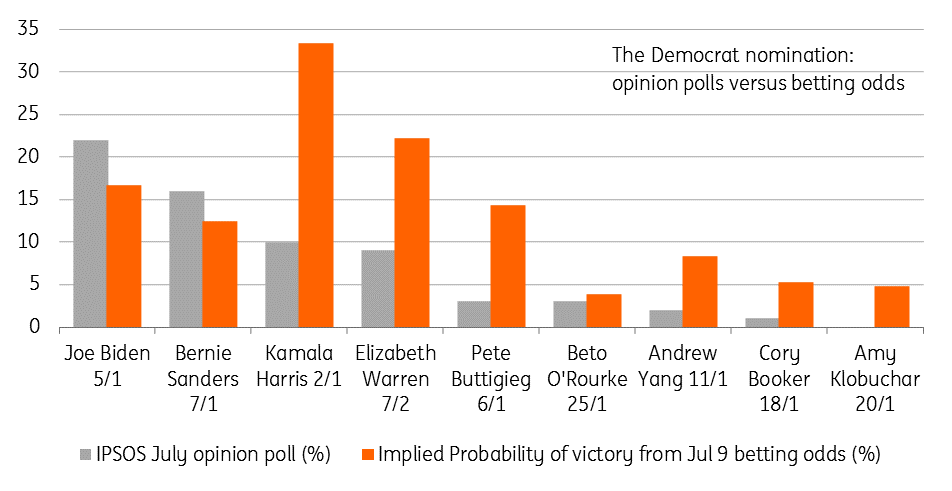

For the Democratic primary candidates, the summer has seen some significant ups and downs. Vice President Biden and Senators Bernie Sanders and Elizabeth Warren appear to be strengthening their grip on the contest following the third primary debate on 12 September. The surge Senator Kamala Harris experienced in July was short-lived, with her numbers returning to the figures prior to the first Democratic debate. It is yet to be seen how impeachment proceedings against President Trump impact this dynamic.

The movement in the betting market has been more marked with odds suggesting it is very much a three-horse race. The latest pricing implies a 40% chance of victory for Warren versus 22% in July. Biden’s implied probability of victory has risen from 16% to 27%, while Bernie Sanders remains around 14%. Andrew Yang is still getting some backing, presumably reflecting expectations that his strong online presence can somehow turn around low name recognition scores. The betting odds of victory for Harris, like her polling, have plummeted. They stand at below 10% today versus 33% in July.

September 2019 Scenario Updates

With 13 months to go until the Presidential election, three possible scenarios are most likely: a Trump re-election, the election of a centrist Democrat, and the election of a populist Democrat. The foundational report published by ING and Oxford Analytica in April 2019 also discussed a fourth scenario, that of another Republican winning the election. However, while such an outcome is not yet completely ruled out, particularly if impeachment proceedings sway moderate Republican Senators, the likelihood of this scenario occurring is too small to warrant an update.

Scenario 2 – a non-Trump Republican suddenly in the spotlight, but still unlikely

Impeachment proceedings against President Trump might, in theory, raise the odds of another Republican challenger winning the 2020 primary race- and the subsequent Presidential election. But in reality, this is unlikely to be the case.

With a two-thirds majority in the Senate required for President Trump to be removed from office, the chances of this happening are low. No Republican Senator has yet expressed support for such action and 20 Republican votes would be needed. Only clear evidence of wrongdoing which significantly sways public opinion is likely to change the vote in the Senate.

Senators would need to be convinced that Trump has less chance of winning re-election than President Pence. Given that the odds of being removed from office are slim, it is also unlikely that President Trump would resign or withdraw from the race. As he has yet to face a serious primary challenge, and the Republican National Committee has sought to limit the ability for him to be challenged, it is similarly unlikely that he would be defeated in a primary contest.

Barring a significant turn of events, this means that President Trump will, in all likelihood, be the Republican nominee in 2020.

Taking into account the lack of progress on trade and domestic politics over the summer months, the start of impeachment proceedings, and the drivers of the different election outcomes outlined in our foundational report, the following descriptions seek to show a narrative of how different scenarios may play out in practice.

Scenario 1 – Looking back from January 2021: How Donald Trump was re-elected

Concern about a slowdown in the economy and the refusal of the Federal Reserve to cut interest rates aggressively see President Trump place greater emphasis on securing a trade deal with Beijing during the first half of 2020. He also seeks to pass popular pieces of domestic legislation, such as infrastructure spending, to satisfy moderate voters. Still, given the tensions in Washington following the launch of impeachment proceedings, his efforts fail. Moreover, the move backfires on Democrats with many swing voters viewing impeachment as a partisan attack, which has also helped to boost campaign funding and support for Donald Trump.

The US-China trade deal, agreed during the spring, leads to an immediate rebound in business and financial market sentiment with stock prices bouncing on the back of it. The White House uses this as a measure of the President’s deal making skills – skills that he will use to extract concessions from other trade partners in a second term. Meanwhile, surprisingly successful cross-party legislation on gun control allows President Trump to tout some bi-partisan domestic policy achievements during the early stages of the Democratic Party primary.

With the economy experiencing modest growth during the early primary contests, Democratic voters remain divided over whether to prioritize electability or progressive policy ideals. The primary therefore becomes a long and drawn out contest that ultimately turns negative, with the vote split between four or five candidates past Super Tuesday. A nominee is not chosen until the party convention in July.

The end of a protracted Democratic primary in the summer of 2020 coincides with a strong uptick in US economic performance stemming from the trade deal concluded in the first quarter of 2020. This allows the White House to set the narrative of the general election around President Trump’s leadership of the economy and the ultimate success of his trade policy.

Strong economic performance in swing states such as Ohio and Pennsylvania leading up to November 2020 allows President Trump to then expand upon his electoral map from 2016 and win a second term.

Scenario 3 – Looking back from January 2021: How a centrist Democrat was elected

With little progress having been made in the trade dispute with China at the start of 2020, and impeachment proceedings drawing significant public attention, President Trump’s behavior and his trade policy are at the center of national politics. Responding to this, the Democratic party primaries and caucuses become overt contests over electability, supplanting policy as the main driver of primary votes. This allows a centrist Democrat to consolidate their position, based upon their perceived ability to attract votes in swing states away from President Trump, and emerge from Super Tuesday as the clear front runner for the nomination.

As the economy slides towards recession in the first half of 2020 and the government's policy comes under increased scrutiny, President Trump is forced to end the trade conflict with minimal gains. While hoping this would alleviate concerns over his handling of trade and allow the economy to rebound prior to the election, the narrative instead focuses on the relatively modest gains made compared to those promised, making his leadership style and poor relationships abroad key issues in the general election campaign.

As concerns over the direction of trade and foreign policy persist, and public approval over congressional handling of impeachment proceedings worsens, the number of moderate Republicans retiring from Congress steadily grows during the first half of 2020. They are replaced by candidates more closely aligned with President Trump, alienating some moderate suburban Republican voters, who are also increasingly concerned with the information presented during the impeachment inquiry.

In the run up to November 2020, the centrist Democratic candidate is able to consolidate these voters and frame the election as a national ‘reset’ away from President Trump’s bombastic style. This allows the centrist Democrat to carry key states Trump won in 2016 and the election.

Scenario 4 – Looking back from January 2021: How a populist Democrat was elected

2019 ends with intensified sanctions against the Chinese economy, as trade talks break down once more. As the economy heads towards a recession, President Trump remains committed to the conflict, blaming poor economic performance on the intractability of the Federal Reserve to aggressively cut interest rates.

President Trump is unable to pass significant legislation during the first half of 2020, with Democrats in the House denying him any political gains prior to the election. Impeachment proceedings past the first quarter 2020 see the White House end negotiations with the Democratic leadership on numerous pieces of legislation.

Senator Mitch McConnell delays the Senate hearing of the House's articles of impeachment, stymying the process and further enflaming public opinion. Many consider this unconstitutional, giving greater strength to Democratic candidates who argue that structural change is needed. Support for impeachment rises above 55%.

With the economy faltering prior to the Iowa Caucus in February 2020, populist Democratic candidates seize upon the growing public concern to promote increasingly progressive policies on welfare, education, taxation and healthcare. Forcing the primary to the left before Super Tuesday, the main populist candidates become the frontrunners for the Democratic nomination, with the post Super Tuesday contests decided between them.

As the second half of 2020 begins, the trade conflict with China remains unsolved, while the new European Commission has pursued increased fines for American technology firms and implemented sanctions as a result of its case against Boeing at the World Trade Organization. Doubling down on his approach, President Trump pushes through strong economic reprisals, further worsening the overall economic outlook prior to the election.

Increased public concern over the economy creates support during the early fall for flagship populist policies such as Medicare for All, cancelling student debt and free public universities. Forced to campaign against these positions, President Trump is unable to repeat his electoral success in the Midwest and loses by large margins in major urban areas, allowing the populist Democratic candidate to win the election.

The economic implications

The scenarios are driven by very different economic and political factors and will yield different outcomes for the US and global economies. For example, under scenario 1, President Trump may find that his domestic legislative agenda is curtailed by opposition lawmakers if Democrats retain control of the House. This could see him re-focus his attention back to trade where he has more leeway. In an environment of ongoing weak global growth, renewed tensions could see market and economic sentiment come under downward pressure once again, exacerbating the risks for the US economy.

Conversely, while the centrist Democrat scenario stems from economic weakness, tax cuts and increases in infrastructure spending could be pushed through (if Democrats retain control of the House), which could provide a boost to growth in 2012/2022. Moreover, better relations with trade partners or a more conciliatory tone towards Europe with the aim of extracting concessions from China could be helpful.

A clean sweep for the Democrats under a populist president could see a more substantial fiscal stimulus package that delivers a sharp rebound in growth. However, lingering concerns about higher corporate taxes and greater regulatory oversight, particularly for Big Tech, could limit the upside for equities and the dollar. Moreover, it is possible that a Populist Democrat picks up where Donald Trump left off regarding aggressive trade protectionism, leading to renewed geopolitical and economic tensions.

These scenarios highlight the high stakes involved in the 2020 elections. There is plenty of time for surprises along the way and we will continue to watch developments closely and update our views accordingly.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

In case you missed it: Two tribes go to war

- This bundle contains 7 Articles