US: More inflation upside to come

- 13 April 2021

- United States

US inflation rose more than expected in March and is likely to push up to 4% as price levels in a vibrant, stimulus fuelled economy constrast starkly with those during the lockdown 12 months ago. There are also a growing number of reasons to think inflation will stay higher for longer with risks increasingly skewed towards a 2022 Fed rate hike

| 2.6% |

YoY rate of US inflation |

Another upside inflation surprise

US March CPI came in a tenth of a percentage point higher than consensus – headline 0.6% month-on-month/2.6% year-on-year while core rose 0.3% MoM/1.6% YoY. Energy rose 5% on higher gasoline prices with transportation rising 2.7% MoM on higher vehicle prices, insurance and fares. Meanwhile, recreation rose 0.4% after a 0.6% MoM gain in February and truck and car rental prices increased 11.7% and lodging away from homes (hotels) rose 3.8% MoM. These are perhaps signs that the higher demand on re-opening is giving entertainment/travel companies some pricing power to expand profit margins.

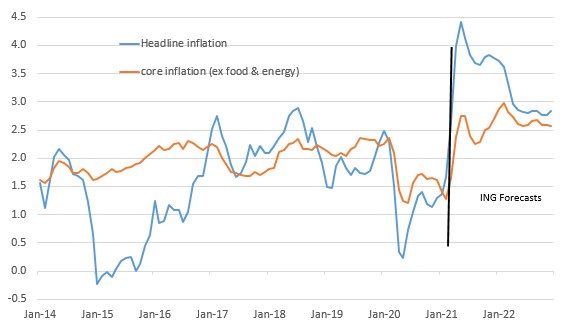

The YoY rate for headline inflation will continue to climb over the next few months as prices levels in a vibrant, stimulus fuelled, re-opened economy contrast starkly with those of 12 months before when lockdowns led to companies slashing prices in a desperate search for sales and cashflow. We think headline inflation could temporarily move above 4% YoY with core (ex food and energy) CPI potentially breaching 3%.

US CPI with ING forecasts (YoY%)

Corporate pricing power is improving

The Federal Reserve is fully expecting to see some strong readings over the next few months, but they have been arguing that significant spare capacity in the economy means that this is unlikely to last with inflation set to drop back again towards the 2% target relatively swiftly.

We are more wary and see scope for a more protracted period of above target inflation. Pipeline price pressures are continuing to build with annual producer price inflation already running at a 10-year high of 4.2% while tomorrow’s import price inflation is expected to rise to 6.5% YoY, which would be the fastest since January 2012.

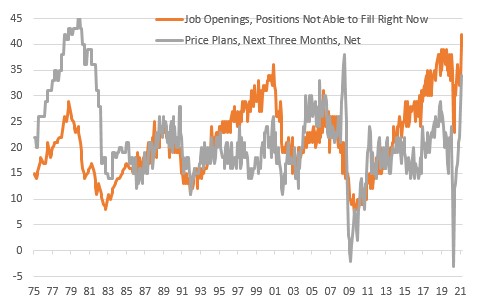

At the same time companies are seemingly more able to pass higher costs on. This morning’s National Federation of Independent Business survey reported the strongest intentions to raise prices since mid-2008 (briefly) – you need to go back to the late 1970s/early 1980s to see consistent readings at these levels. We also know from the ISM reports the orders are close to record highs while customers’ inventories are at record lows. This suggests companies have strong pricing power that could allow them to expand profit margins after several years of margin compression, which could keep inflation higher for longer.

NFIB survey on job openings and pricing intentions

Housing is the component to watch

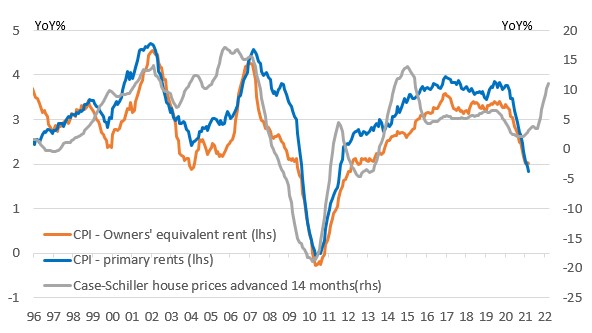

We also think that the housing components will be an increasingly important story over the next twelve months. Primary rents and owners’ equivalent rent account for a third of the CPI basket. Movements in these components tend to lag 12-18 months below house price developments, as the chart below shows, which means that the housing components may well be the story to watch through the second half of this year.

US housing components look set to swing sharply higher in 2H 2021

If these housing components do swing higher, as we suspect, this means inflation could stay closer to 3% for much of the next couple of years. In an environment of strong growth and rapid job creation it adds to our sense that risks are increasingly skewed towards a late 2022 rather than 2024 as the Fed currently favours.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more