Why an impending US downturn may simply be delayed

- 31 August 2023

- United States

The US confounded 2023 expectations that it would fall into recession as households used pandemic-era savings and their credit cards to maintain lifestyles amidst a cost-of-living crisis. But with loan delinquencies on the rise, savings being exhausted, credit access curtailed and student loan repayments restarting, financial stress will increase

Robust resilience in the face of rate hikes

At the beginning of the year, economists broadly thought the US economy would likely experience a recession as the fastest and most aggressive increase in interest rates inevitably took its toll on activity. Instead, the US has confounded expectations and is on course to see GDP growth of 3%+ in the current quarter with full-year growth likely to come in somewhere between 2% and 2.5%. What makes this even more surprising is that this has been achieved in the face of banks significantly tightening lending conditions while other major economies, such as China, are stuttering and even entering recessions, such as in the eurozone.

Consumers still happy to spend with the jobs market looking so strong

So why is the US continuing to perform so strongly? Well, the robust jobs market certainly provides a strong base, even if wage growth has been tracking below the rate of inflation. Maybe that confidence in job security has encouraged households to seek to maintain their lifestyles amidst a cost-of-living crisis by running down savings accrued during the pandemic and supplementing this with credit card borrowing.

The housing market was another source of concern at the start of the year, but even with mortgage rates at 20-year highs and mortgage applications having halved, prices have stabilised and are now rising again nationally. Home supply has fallen just as sharply, with those homeowners locked in at 2.5-3.5% mortgage rates reluctant to sell and give up that cheap financing when moving to a different home and renting remains so expensive. This has helped lift new home construction at a time when infrastructure projects under the umbrella of the Inflation Reduction Act are supporting non-residential construction activity.

But lending is stalling and savings have been run down

The Federal Reserve admits monetary policy is now restrictive, and while it could raise interest rates further, there is no immediate pressure to do so. With inflation showing encouraging signs of slowing nicely, this is fueling talk of a soft landing for the economy. With less chance of an imminent recession, financial markets have scaled back the pricing of potential interest rate cuts in 2024, with the resiliency of the US economy prompting a growing belief that the equilibrium level of interest rates has shifted structurally higher. This resulted in longer-dated Treasury yields hitting 15-year highs earlier this month.

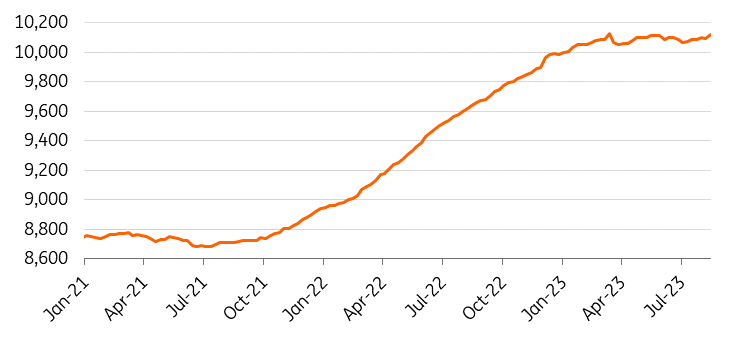

Outstanding commercial bank lending ($bn)

Nonetheless, the threat of a downturn has not disappeared. We estimate that around $1.3tn of the $2.2tn of pandemic-era accumulated savings has been exhausted and at the current run rate all will be gone before the end of the second quarter of 2024. At the same time, banks are increasingly reluctant to lend to the consumer with the stock of outstanding bank lending flat lining since the banking stresses in March, having increased nearly $1.5tn from late 2021. We suspect that financial stresses have seen middle and lower income households accumulate the bulk of the additional consumer debt and have run down a greater proportion of their savings vis-à-vis higher income households so a financial squeeze for the majority is likely to materialise well before the second quarter of 2024.

Rising delinquencies will accelerate as student loan repayments resume

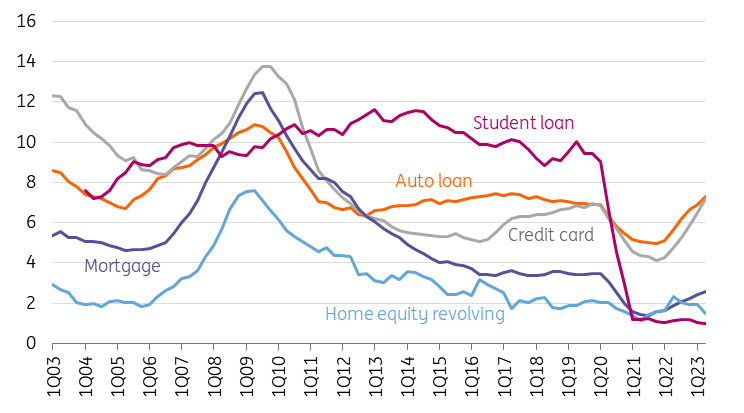

Indeed, consumer loan delinquencies are on the rise, particularly for credit card and vehicle loans with the chart below showing data up until the second quarter of this year. Since then the situation has deteriorated further based on anecdotal evidence with Macy’s CFO expressing surprise at the speed and scale of the rise in delinquencies experienced through June and July on their own branded credit card (Citibank partnered). With credit card interest rates at their highest level since 1972 and with household finances set to become more stressed with the imminent restart of student loan repayments, something is likely to give. We see the risk of a further increase in delinquencies, which will hurt banks and lead to even further retrenchment on lending, together with slower consumer spending growth and potentially even a contraction.

Percent of loans 30+ days delinquent

4Q moving sum

Downturn delayed, not averted

The manufacturing sector is already struggling and we see the potential for consumer services to come under increasing pressure too. On top of this there are the lingering worries about the demand for office space and the impact this will have on commercial real estate prices in an environment where there is around $1.5tn of loans needing to be refinanced within the next 18 months. With small banks the largest holder of these loans, we fear we could see a return to banking concerns over the next 12 months.

Consequently, we are in the camp believing that it's more likely that the downturn has been delayed rather than averted. Fortunately, we think inflation will continue to slow rapidly given the housing rent dynamics, falling used car prices and softening corporate pricing power and this will give the Federal Reserve the flexibility to respond swiftly to this challenging environment. We continue to forecast the Federal Reserve will not carry through with the final threatened interest rate rise and instead will switch to policy loosening from late first quarter 2024 onwards.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: Summertime sadness

- This bundle contains 13 Articles