US mid-term elections: Feeling Blue?

- 1 November 2018

- United States

The mid-term elections are less than a week away and opinion polls continue to suggest the Republicans are under pressure. The loss of Congressional control would make life increasingly difficult for President Trump and have major implications for policy. Here we revisit the possible election scenarios and assess their market implications

Scenarios and market implications

We see four broad scenarios for the post-November landscape and it is through a prism of fiscal, monetary and protectionist policy that we should view the market impact.

Setting the scene

The 6 November mid-term election offers the electorate the opportunity to give their assessment on the first two years of Donald Trump’s presidency. Does the “Make America Great Again” policy thrust continue to resonate to the same degree, have legal issues taken their toll, or is it still all down to “the economy, stupid”? The outcome will have major ramifications for economic and trade policy, which will set the battleground for the 2020 presidential election.

Currently, the Republicans hold the Presidency and majorities in both the House of Representatives and the Senate, but Democrats will be looking to break this stranglehold. All 435 House of Representative seats are up for grabs along with 35 of the 100 Senate seats[1].

The Republicans hold 235 seats in the House of Representatives versus the Democrats’ 193 while there are seven vacant positions. This means the Democrats need to make a net gain of 25 seats to wrestle control of the House from the Republicans

In the Senate, the Republicans have a wafer-thin majority. They currently hold 51 of the 100 seats (plus the Vice President’s vote if needed in a tied vote) while the Democrats have 47 and there are two independents, who vote with the Democrats. However, of the 35 seats being contested in November, the Democrats have 24 up for election along with the two independents, while the Republicans only have nine. As such, the Democrats need to win two of the nine Republican-controlled Senate seats, while holding on to all of the seats they currently occupy to gain control of the Senate.

National polls have remained broadly stable over the last month or so, showing Democrats ahead by 8-9%, though President Trump's approval rating has improved slightly (but his net approval remains negative). This points to a solid but not insurmountable advantage for Democrats in the House race, while Republicans remain favoured in the Senate thanks to the advantageous map.

Betting odds and polling analysts continue to believe the most likely outcome is that the Democrats will win control of the House of Representatives, but fall short in their quest for the Senate. The odds of a Democratic Senate majority have lengthened materially, with no more than a 10-15% probability now ascribed to that outcome. Democrats would need to win every close race in the Senate to make it to 51 seats (or perhaps score a surprise win in Texas or Tenessee).

Betting odds and polling analysts believe the most likely outcome is that the Democrats will win control of the House of Representatives, but fall short in their quest for the Senate

Still, even if the most likely outcome is a Democratic House and a Republican Senate, there is a fairly large chance of a surprise outcome. That's because there is virtually no chance of a Democratic Senate and a Republican House, so the probability of the two less likely outcomes (Democrats win the Senate, or Republicans hold the House) are cumulative. That means there is a 30-40% chance of a different outcome from the central expectation. To the extent that markets are expecting a Democratic House/Republican Senate, there may be scope for a sudden adjustment on the morning of November 7th if there is a different outcome.

Odds of Democratic control of Congress after 2018 Mid-terms

(Figures as of 1 November in BOLD, and as of 26 September IN BRACKETS)

|

|

FiveThirtyEight |

PaddyPower |

PredictIt |

|

House of Representatives |

85% (80%) |

4/9 ~69% (4/11 ~64%) |

70% (66%) |

|

Senate |

15% (31%) |

12/1~ 8% 5/1 (~17%) |

12% (31%) |

[1] Members of the House of Representatives serve two-year terms whereas the President has a four-year term and a Senator has a six-year term. Senators terms are staggered so one-third of the 100-member Senate are up for re-election every two years. This year there are 33 Senate seats being voted on in regular elections with two additional special elections due to Senators resigning before their term ended.

Key issues for the next two years

Donald Trump’s first two years as President have seen a big win for him on tax reform, but a defeat on healthcare. He is fully immersed in trade right now and can also celebrate a strong jobs market, but he has made little progress on his infrastructure spending plan. Certainly, the economy is performing very well, and interest rates continue to rise in a “gradual” fashion.

In the run-up to mid-term elections, global investors are quite heavily positioned; long dollars, long US equities and short US Treasuries even after recent market wobbles. The context here is a pump-primed US economy, whose loose fiscal and tight monetary settings have driven US rates and the dollar higher, while at the same time pressure testing the external balance sheets of some of the largest emerging market economies. Trade and infrastructure plus further tax and healthcare reform are likely to be his key policy thrusts in the second half of his term, but he will need support from Congress. This underlines the significance of these mid-term elections.

In this regard, we feel that there are three major issues we should focus on before diving into the scenarios since they will have a major influence on the likely successes and the market reaction.

1) What happens to fiscal policy and fiscal sustainability?

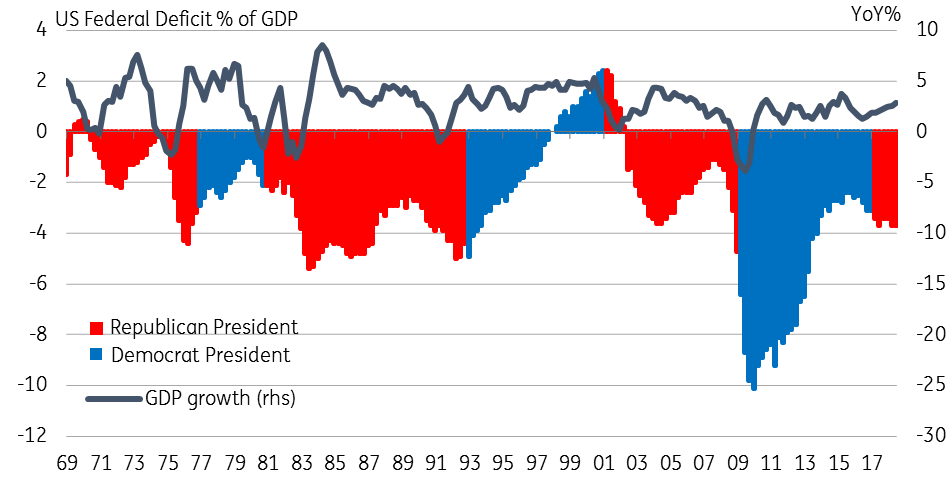

Historically the trend has been Federal budget deficits widens out during Republican presidencies and narrows under Democrat Presidents. President Trump has not bucked that trend with the Federal fiscal deficit approaching 4% of GDP despite the economy growing 3% this year. Even without any further fiscal boost, the Congressional Budget Office believes the Deficit will hit 4.6% of GDP in 2019 at a time when unemployment is approaching 50-year lows.

US Federal deficits: Republicans vs Democrats

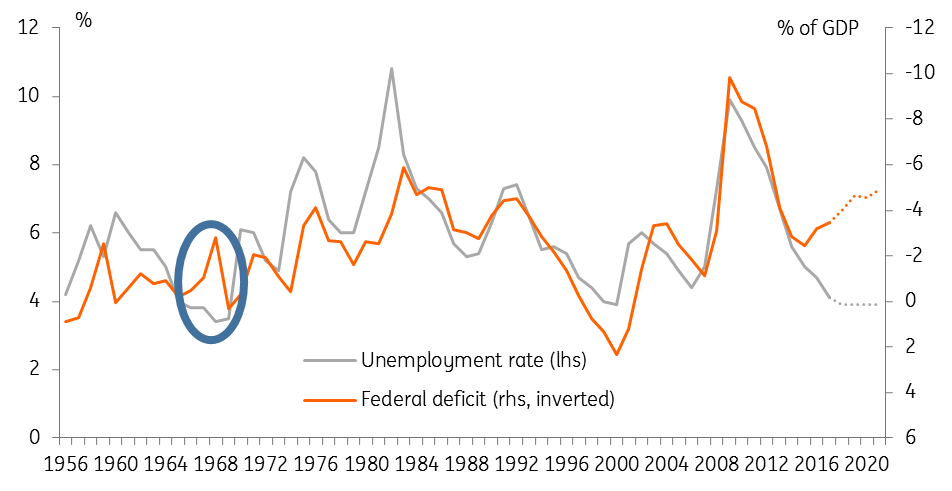

As the chart below shows, the last time this divergence between a strong economy and weak government finances existed was 1968 when the US was spending nearly 10% of GDP on the Vietnam War – a very different situation to how the US finds itself today. If for whatever reason, growth starts to disappoint, questions about US government debt sustainability may start to adversely affect financial markets and feed into economic sentiment, possibly creating a vicious downward cycle.

The Federal Deficit and unemployment 1956-2018

Loss of Republican control of Congress would limit Trump’s ability to pass legislation, making further fiscal stimulus such as his $1.5 trillion infrastructure spending plan or changes to the US healthcare system less likely. However, if the Republicans retain control of Congress (both the House and the Senate), then there is scope for further fiscal expansion, which could put an additional strain on the medium- and longer-term government finances.

2) What happens to trade policy?

President Trump has been very vocal on trade, calling out what he believes are unfair practices and levying significant tariffs. China has received much of his ire, with a demand to more than half the current bi-lateral deficit of $370 billion, but the EU and Nafta partners are not immune.

The latest round of tariffs on $200bn of Chinese imports, combined with the threat that tariffs could be extended to all Chinese imports, reinforces the message that he will not back down until China changes its position. But this doesn't look its happening anytime soon with China’s retaliation measures already coming into force.

The Democrats have a history of being more protectionist and may well back President Trump to some degree on his attitude toward China

Though, after the mid-term elections, pro-trade Republican politicians and corporates, who have been quiet in the lead up to polling, may be prepared to make a more forceful stand against protectionist measures. The President may well listen if there is growing evidence of a negative impact on the economy – so long as he can still portray the result as a “big win”. However, Democrats have a history of being more protectionist and may well back the President to some degree on his attitude toward China. They are likely to advocate a softer approach to US allies such as Canada, Mexico and the EU though.

The alternative argument is that Trump instead chooses to double down and implement further protectionist measures. In the near term at least he may feel that a strong economy and buoyant asset prices will act as a backstop to becoming more aggressive on trade and protecting intellectual property. But if concessions are not forthcoming and the trade war intensifies this would risk hurting growth and also equity markets, which he often views as a key barometer of his performance. A weaker economy and falling US household wealth would not stand him in good stead for a defence of his presidency in 2020.

3) Could the President be impeached?

This is a topic that is never far from the lips of media commentators. The most plausible scenario is if the investigation of Russian interference in the 2016 election by special Counsel Robert Mueller shows direct and incontrovertible evidence to support impeachment.

Even with a Republican electoral “win”, President Trump would, of course, remain vulnerable to new evidence from the Mueller investigation

A simple majority in the House in favour of starting proceedings would result in a Senate trial. Given this would require a supermajority of 67 out of 100 Senators who are likely to vote on party lines largely, Trump would survive unless a substantial number of Republican senators turn on him. If the Democrats were to fail to make any gains in the Senate, it would require 18 Republican Senators to cross the floor and vote with the Democrats. This sounds unlikely, especially if they believe President Trump can pardon himself - as he has stated.

Even with a Republican electoral “win”, President Trump would, of course, remain vulnerable to new evidence from the Mueller investigation. And the campaign for 2020 will in effect start as soon as the mid-terms end. That suggests political tension will remain high in the US.

Republicans control both the House and the Senate: Trump Unbound (medium probability)

If the Republicans maintain control of both the House and the Senate, this will be seen as a major victory and would be taken as an explanation of President Trump’s current policies. The President would push on with the ‘America First’ policy-mix, and with another electoral win under his belt could well get stronger support from the Republican party. This may lead to further tax cuts and deregulation, a more hard-line stance on immigration and trade, and a generally a more aggressive approach to politics both at home and abroad.

Under this scenario, President Trump is likely to push on with the ‘America First’ policy-mix, and with another electoral win under his belt could well get stronger support from the Republican party

In the near term, this could provide a renewed boost to equity markets and domestic demand, but concerns will likely increase around the US fiscal deficit, the impact from trade wars, and perhaps around the geopolitical environment and the role America chooses to play. As such we see this as something of a boom-bust story, which risks an increasingly aggressive response from the Federal Reserve in the form of higher interest rates, which could put Fed Chair Jerome Powell on a collision course with the President.

Longer-dated yields will also rise in response to wage gains and higher inflation resulting from stronger growth, while the question of longer-term fiscal sustainability could add further upward pressure. This will be a tricky situation to manage before the inevitable bust when we see longer-dated yields drop on expectations of a policy reversal from the Fed. Likewise, the dollar could strengthen further into 2019 under this scenario. However, investors will become increasingly concerned by growing twin deficits and will be looking to sell dollars at the first signs that the fiscal stimulus is wearing off and the US is left with the baggage of higher deficits. Putting timings on this is difficult, but if the economy holds up until 2020, it may be enough to secure a second term for President Trump.

Democrats win control of the House but fall short in Senate: Trump tapered (high probability)

In this scenario – which betting markets and pollsters suggest is the most probable outcome - Democrats win control of the House with a modest majority but fall just short in the Senate. President Trump was already somewhat limited by congressional deadlock, but this situation becomes even more challenging for him, and he struggles to pass major legislation. Bi-partisan action may be possible in areas such as infrastructure spending, but for the most part divisions between and within the two parties remain material. Faced with this President Trump focuses on areas executive powers give him more leeway to set the agenda, such as trade policy.

This makes the outlook for trade policy difficult to call. If trade is the only real source of authority the President has, he could continue pushing hard for China to make concessions to get the bi-lateral deficit lower. Given China’s response so far, this is unlikely to happen quickly. While trade is not necessarily a critical issue for the Democrats, it is unlikely they will support a trade war with traditional allies like the EU.

Likewise, withdrawal from the WTO is unlikely to get a lot of support from Democrats, so overall Congress is likely to put up more resistance regarding trade policy than it did previously. Our trade team believes that if Trump does attempt to pull out of the WTO, this will be challenged in court by Congress with the decision potentially settled by the Supreme Court.

This scenario will probably make things more challenging for President Trump as he'd struggle to pass major legislation. Faced with this, he's likely to focus on areas executive powers give him more leeway to set the agenda, such as trade policy

Given there is a reduced prospect of additional fiscal expansionary policy in a split Congress, the fears on debt sustainability may subside. We are also likely to hear more Trump criticism of the Federal Reserve if the central bank continues raising interest rates, but given the strong growth environment and with inflation above target we expect the Fed to continue with their “gradual” policy hikes. We think this scenario will be fairly neutral for the economy, but there is the risk of government shutdowns given differences of opinion on government funding.

In terms of financial markets, there is heavy long positioning regarding the US right now even after recent volatility. This means that perceptions of a more limited room for fiscal manoeuvre might trigger some mild profit-taking on the dollar and US equities, but probably not a sharp sell-off. Rest of the World economies do not have particularly compelling growth stories right now and unless Trump surprises by scaling down protectionism it is hard to see a dramatic rotation into overseas asset markets.

If the Democrat-controlled House were to vote in favour of impeachment, there would likely need to be overwhelming evidence from the Robert Mueller investigation to get the required number of Republican Senators to cross the floor and vote to impeach their President. Given this challenge, the Democrat leadership may be reluctant to act quickly, and if they do pull the trigger, there is a strong likelihood Trump would be found not guilty.

Democrats win control of at least the House: Grand Bargain (low probability)

If the Democrats win control of at least the House, their position will strengthen considerably. One possibility, though an unlikely result, could be that President Trump and his Democratic opponents choose to bury the hatchet and work together. Further fiscal spending (including infrastructure and potentially more tax cuts targeted at lower-income household) is at least in theory appealing to both sides. Compromise on trade (where Democrats are not necessarily opposed to some of Trump’s ideas) is also plausible.

This scenario is likely to be positive for the domestic growth story with political risks dramatically scaled back - and little likelihood of impeachment

Further fiscal loosening with a benign backdrop may also lead to a slightly more aggressive Federal Reserve interest rate tightening cycle. Together with congressional consensus on the pursuit of the trade war with China, this should be a mild positive for US asset markets, but positioning probably restrains bigger moves. Worries about the medium-term fiscal sustainability could come more to the fore too with longer-dated yields pushing higher. Given these compromises, there would be little likelihood of impeachment.

Democrats win big in the House and Senate: All-out war in D.C. (medium probability)

If the Democrats win big in the House and the Senate, Trump’s legislative position is in tatters as they can block the majority of the President’s agenda. This means complete gridlock, frequent risk of government shutdowns, and an even more volatile political environment ahead of the 2020 presidential campaign, which in effect begins as soon as the mid-terms are over. President Trump would be limited to Executive Powers only.

This scenario is not necessarily negative for growth but could pose major headwinds for risk assets given greater political uncertainty. If Robert Mueller does find evidence of a Russian link, the Democrats may use the resulting political momentum to start impeachment proceedings against the President. A strong Democrat majority in the House would likely vote in favour, but it would still need several Republican Senators to vote against the President to reach the 67 votes required to force him out.

This scenario could leave President Trump’s legislative position in tatters as the Democrats could block the majority of the President’s agenda. This might not necessarily be negative for growth but could pose major headwinds for risk assets given greater political uncertainty

The Federal Reserve may at the margin take a more cautious approach to policy tightening, particularly if the threat of shutdowns and impeachment are realised. Trump would also likely push his executive powers on trade, which may add to the headwinds for growth. However, he would likely be more restricted under this scenario.

Complete gridlock in Washington and a higher risk of government shutdowns and impeachment proceedings argue that the correction in US asset markets is more aggressive than under the Trump-tapered scenario. Impeachment may be more an issue of noise for the dollar (Clinton's impeachment process took over a year before being dismissed), but more impact would be felt were the Fed to acknowledge these headwinds and go slow/re-assess the need for future policy tightening.

An additional point to consider is that if Republicans lose their majority in the Senate as well as the House, Democrats will be able to block Trump’s appointments to federal courts or any new cabinet members. Further appointments to the Federal Reserve would also be at risk, though historically Fed appointments have been less of a partisan issue.

Final thoughts

President Trump has primarily targeted healthcare, taxation and trade in the first half of his Presidential term. January’s State of the Union address suggested infrastructure and further tax reform would be the main thrust of the second half. The upcoming mid-terms could easily scupper that plan assuming the Democrats perform as well as pollsters expect.

Our base case is that a split Congress will mean his legislative agenda is curtailed, but not completely blocked though this will require working with the Democrats, such as on infrastructure. Trade policy will remain in focus, but if he can forge a united front with the EU, Canada and other key partners regarding China, there are more likely to be concession he can label a “win” for his stance. Further tax reform is possible, but new initiatives would need to be focused at the lower end of the income distribution to get Congressional support.

This is a relatively benign story for the economy and asset markets. However, the challenges the US economy faces will intensify. The fading support from the fiscal stimulus, the strong dollar and higher interest rates together with growing concerns about the prospects for emerging markets are all likely to weigh on activity. An all-out trade war would compound these problems and risk a downturn in US growth prospects and asset markets. Such a situation would pose even bigger challenges for President Trump if, as most analysts expect, he seeks re-election in 2020.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

In case you missed it: Change of guard

- This bundle contains 9 Articles