US manufacturing supports firm third quarter, but construction highlights fourth quarter challenges

- 1 September 2022

- United States

Decent manufacturing activity, improved trade and inventory contributions and the cashflow boost from falling gasoline prices mean the US is set for a strong third-quarter GDP reading of around 3%, but another decline in residential construction reinforces the worries about what might happen later in the year

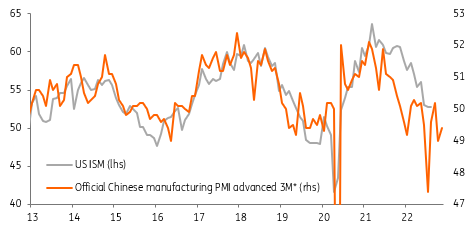

ISM holds up as rising orders and falling prices offer hope for the sector

The ISM manufacturing index held up better than expected in August, coming in at 52.8, unchanged from July and better than the 51.9 consensus. Mixed regional indicators and a softer China PMI had raised warning flags, but instead new orders moved back into positive territory at 51.3 from 48 while employment rose to a five-month high of 54.2, boosting hopes of a decent manufacturing contribution to Friday's jobs number. Regarding jobs, the ISM reported that “companies continued to hire at strong rates in August, with few indications of layoffs, hiring freezes or head-count reductions through attrition. Panelists reported lower rates of quits, a positive trend”.

US and Chinese manufacturing purchasing managers' indices

There was also a rise in the backlog of orders which suggests that the dip in the production component to 50.4 from 53.5 is just a temporary blip and that manufacturing output can continue growing at a firm pace over coming months. Indeed, the ISM cite the better lead time for supplier deliveries and the falling prices paid component as factors that “should bring buyers back into the market, improving new order levels” The Fed will also take some comfort from the prices paid component declining to 52.5. This index was above 80 as recently as May and reflects the steep falls in energy and key commodity prices.

Putting it together, with the better trade and inventory numbers and the massive support to consumer spending power and confidence from the falls in gasoline prices we look for 3% annualised GDP growth in the third quarter after the technical recession in the first half of the year. This should be supportive of our Fed funds call of 3.75-4% rates for year end.

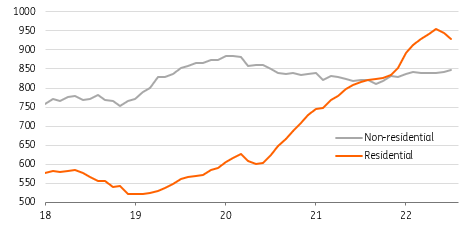

Construction highlights the weakening medium-term outlook

There was less positive news in the construction data, which fell 0.4% month-on-month in July after a 0.5% fall in June. Residential construction was the main reason with the slowdown in housing activity set to translate into falling home building over at least the next six months.

Annualised US residential and non-residential construction spending ($bn)

Declining housing transactions implies big declines in residential construction and weakness in some retail sales components such as building supplies, furniture and home furnishings. Falling house prices would compound the downside risk for confidence and spending so while 3Q activity overall looks pretty good, 4Q will be much more challenging, especially with China under pressure and Europe facing an energy catastrophe.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more