US inflation slows, but higher savings mean a resilient consumer

- 29 September 2023

- United States

The Fed's favoured measure of inflation undershot expectations and has boosted the case for the Fed not hiking rates in the current quarter. But huge upward revisions to houshold savings suggests the consumer can remain more resilient than we thought likely and supports the case for the Fed keeping monetary policy tighter for longer

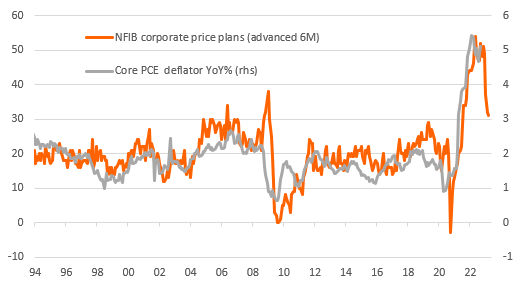

The US personal income and spending report contains lots of numbers, but the August 0.1% month-on-month core PCE deflator print catches the eye. The consensus was 0.2% and we had been fearing a 0.3% outcome given what we saw from core CPI. There are quite a lot of revisions, but now we have three consecutive 0.2% or 0.1% MoM prints for what is the Fed's favoured measure of inflation. That should argue against the need for a fourth quarter rate hike, especially if we aren't going to get much data over the next month due to the strong likelihood of a government shutdown.

The year-on-year rate remains elevated at 3.9%, but we are hopeful of ongoing declines over the next few months given we have 0.5% MoM and 0.4% MoM readings from September and October 2022 dropping out of the annual comparison. The three-month annualised rates are already getting close to the Fed's 2% target and assuming we see 0.2% MoM prints for the rest of the year we would have annual core inflation near to 3% YoY by year-end, which should calm some of the fears of the hawks on the Fed.

US core personal consumer expenditure deflator (% change)

Huge revisions to income and spending mean households have more residual savings than thought

Meanwhile household incomes rose 0.4% MoM and spending increased 0.4%, but for GDP growth we are interested in the real, inflation-adjusted numbers. This had real spending increase 0.1% MoM after a 0.6% gain in July, meaning we are on track for real consumer spending growth of around 3.7% annualised in the third quarter, which would help to get GDP growth of around 3.5%.

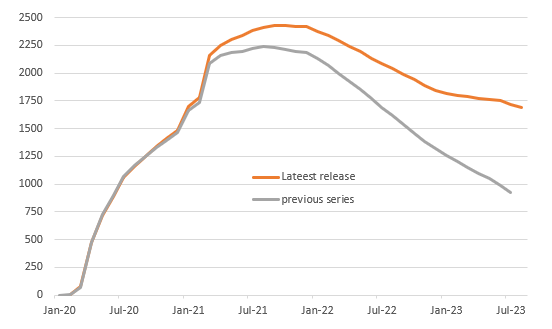

There were significant revisions to the history though with incomes revised higher and consumer spending revised lower. This is important as it suggests that the household sector accrued more savings during the pandemic and have run down less than previously thought. These aren’t insignificant numbers either. We are talking upwards of $700bn of pandemic-era accrued savings being available to households over and above what we previously thought, which could keep consumer spending more resilient than we had been thinking.

Stock of excess savings accrued since the pandemic ($bn)

No fourth quarter hike, but interest rates could indeed be higher for longer

The proviso is we don’t have a breakdown on who has these savings and the assumption has to be that many low-income households have already burnt through most of them. This was an assertion made within the Federal Reserve’s Beige book which stated that “some Districts highlighted reports suggesting consumers may have exhausted their savings and are relying more on borrowing to support spending”.

The challenges being faced by the household sector are growing, be it from low real income growth, difficulty obtaining credit, rising gasoline prices eroding spending power, student loan repayments restarting and strike/government shutdowns hitting paychecks. But if there are residual savings out there then consumer spending could end up being more resilient, which would justify the market’s belief in Federal Reserve monetary policy staying tighter for longer.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more