US inflation keeps a final rate hike on the table

- 12 October 2023

- United States

Headline inflation was a touch higher than the market expected while the “super core” measure of services ex-shelter, ex-energy came in at a fairly hot 0.6% MoM. This was primarily hotels and motor insurance, which will subside, but the Fed will want to see clear evidence of this softening before it will be comfortable that monetary policy is tight enough

| 3.7% |

Annual rate of US inflation |

Headline inflation remains 3.7%

US consumer price inflation for September shows headline prices rose 0.4% month-on-month, and 3.7% year-on-year. The consensus forecast ahead of time was 0.3% MoM and 3.6% YoY. Meanwhile, the core rate, which excludes food and energy, came in at 0.3% MoM and 4.1% YoY as expected. This was the outcome we were forecasting, believing the consensus was a little low for headline inflation given the moves in gasoline prices (which rose 2.1% on the month).

US core (ex-food and energy) CPI % changes

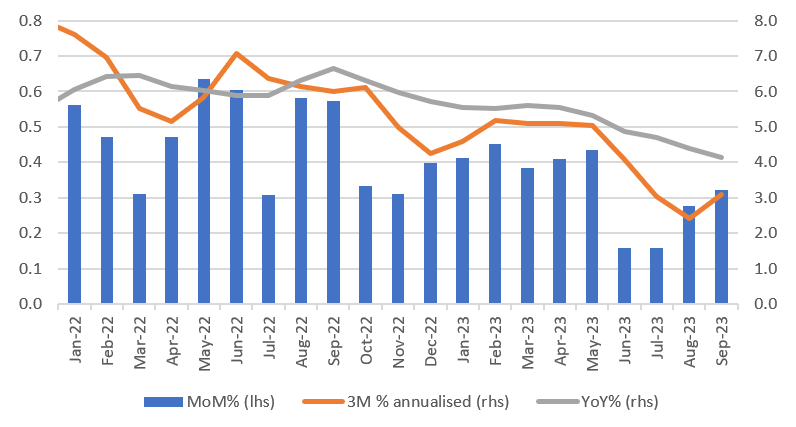

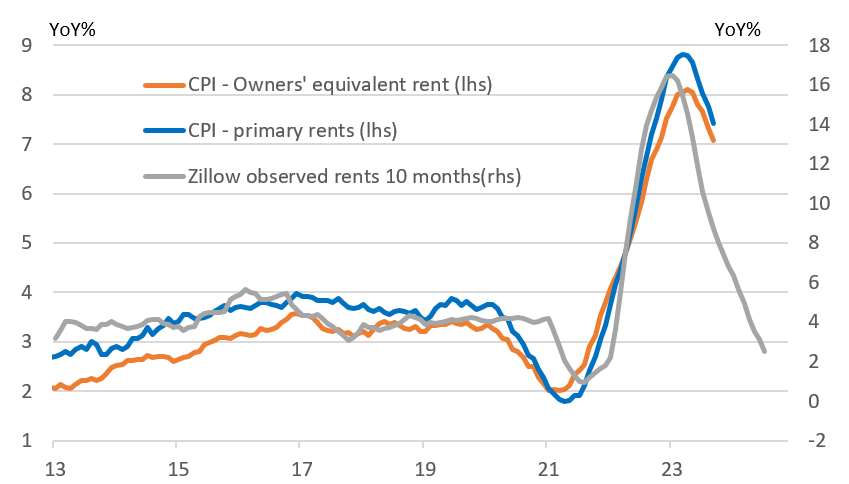

Housing will pull inflation lower

We’ve seen Treasury yields tick higher in the wake of the numbers, which is understandable given the 25bp drop in the 10-year since the end of last week caused by a combination of geopolitical worries and dovish Federal Reserve commentary. The market shouldn’t be too upset though. Housing is still running hot, rising 0.6% MoM, but we know that the relationship with housing rents data means this will slow meaningfully in coming months.

Housing CPI components and rent changes

Super core inflation remains hot, but monetary policy is probably tight enough

Medical care (0.2%), education/communication (0.1%), apparel (-0.8%), and used vehicles (-2.5%MoM) are clearly in a good place. OK, recreation remains quite strong at 0.4% MoM, but this may well be tied to the summer strength in activity related to Taylor Swift, Beyonce and Barbie, and we don’t expect it to persist given concerns about the prospects for consumer discretionary spending. Hotel prices were also strong, rising 3.7% MoM while motor vehicle insurance rose another 1.3%, reflecting the lagged effects of rising vehicle prices and higher motor thefts. Hotels and insurance were a large part of why the super core rate (services ex-shelter and ex-energy), which the Fed is keeping a careful eye on given this is going to be driven more by wage pressures in a tight jobs market, rose 0.6% MoM. Again, we don’t see strength here lasting much longer.

The market pricing around the possibility of a rate hike by December has increased marginally, but we doubt it will happen. Fed officials have been emphasising the importance of the increase in Treasury yields as a factor that will tighten financial conditions and reduce the need for another rate hike. With mortgage rates at 23-year highs and credit card borrowing costs at all-time highs, monetary policy looks restrictive enough. Moreover, with corporate pricing surveys, such as in the NFIB small business optimism report, pointing to a gradual softening ahead, we see inflation continuing to moderate slowly over the next couple of quarters.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more