US inflation details ease concerns of energy spillover effects

- 10 June

- United States

While US headline inflation was lifted by sharp gasoline and airline fare increases, other components were better behaved, leading to a softer-than-anticipated core inflation print. June's inflation rate should be pulled lower by a reversal in gasoline, but inflation remains vulnerable to ongoing volatility in energy costs

Core inflation better behaved than expected

The May consumer price inflation report rose 0.5% month-on-month/4.2% year-on-year at the headline level, as expected, but core inflation was a touch softer at 0.2%MoM/2.9%YoY versus the 0.3% consensus forecast and the 0.4% print from April. To three decimal places it was a 0.208% core CPI MoM print.

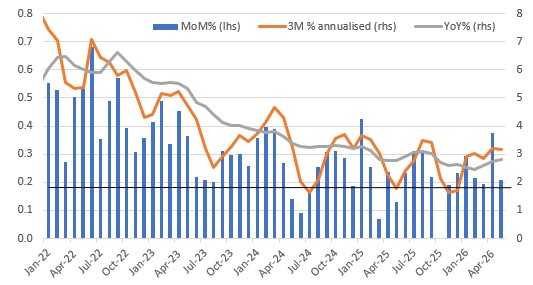

Prior to the release, there was a clear skew in economists’ forecasts towards the prospect of a 0.2% outcome being more likely than a 0.4% outcome. Nonetheless, the chart below shows that the MoM rates continue to run hot relative to the 0.17% MoM trend that is needed to bring the annual rate of inflation back down to 2%. As such, market reaction is fairly muted though, with 10Y yields down around 3bp and Fed rate hike expectations for 2026 being pared back to 25bp from 28bp.

Core consumer price inflation metrics (MoM%, 3M annualised, YoY%)

Government shutdown effects unwind

The details show a 7% MoM jump in gasoline prices did the damage at the headline level, but this should reverse in the June CPI report given that gasoline prices nationally are back down to $4.15/gallon after averaging $4.50 through May. Airline fares were also a strong upward influence, rising 2.7% while education rose 0.8% and other goods and services rose 1%.

Counteracting these components, we saw a 0.3% price drop for new vehicles while housing, which has a 44% weighting within the inflation basket, rose just 0.2% MoM. Remember it had jumped 0.7% MoM last time due to survey methodology that uses a sample panel that rotates on a six-month time frame. Because the Bureau of Labor Statistics entered a 0% outcome for October – when the government shutdown prevented any survey from being conducted – there was 'payback' in the April report. That effect has now unwound.

Waning tariff, rents and wage rates can help to mitigate energy threats

Looking ahead, the housing components should show inflation pressures moderating further with private rent surveys (realtor.com, apartments.com, Zillow) pointing to outright declines in a growing number of states. Meanwhile, the Dallas Federal Reserve Bank estimates that tariffs are currently lifting the annual rate of core PCE inflation by 0.9ppt. Tariffs are a one-off step change in prices and we have since transitioned to a lower tariff regime, that includes many exemptions, following the Supreme Court’s decision to strike down 'Liberation Day' tariffs. The refunds of those tariffs will provide relief for corporate America and should go some way to covering increases in energy/transportation costs they may be facing.

Remember too, that the biggest cost input for corporate America is the cost of the workforce and with wage growth continuing to slow, that should also help take some of the steam out of core inflation, even if headline inflation remains vulnerable to volatility in energy prices. This should all help to keep inflation expectations in check, so while we no longer expect the Fed to cut interest rates this year given improved economic momentum, we don’t expect a rate hike either.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more