US Housing in 2018: From strength to strength

- 24 January 2018

- United States

The US housing market looks in robust shape going into the new year and should support GDP growth in 2018

Supply constraints support prices

2017 was a bumper year for US housing. Prices rose steadily, increasing by nearly 7% as of November, which is strong but well short of the unsustainable double-digit increases seen before the 2007 crash. Sales of existing homes continued to increase, reaching 5.57m annualised in December.

Construction of new homes continued to rise throughout the year. But new construction failed to keep pace with increasing demand; as of December, the inventory of homes for sale compared to the current rate of sales stood at the lowest level since 2005.

Homes available for sale fall to lowest level since 2005

Continuing momentum

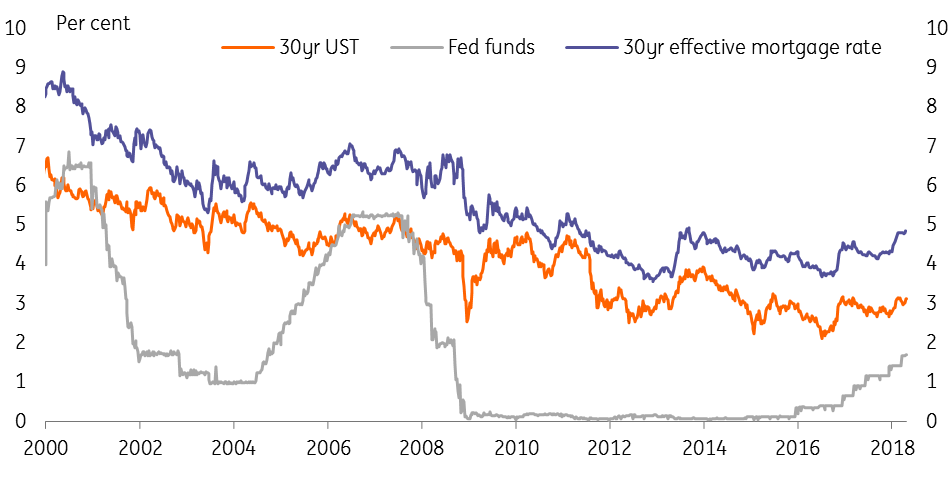

Given continued strong momentum in the overall economy and tight supply in the housing market, these trends are likely to continue in 2018. 30-year mortgage rates are likely to drift up in 2018 as bond markets react to an anticipated increase in inflationary pressures, strong growth and the prospect of the Fed hiking short-term rates plus some potential concern about the impact of tax reform on government finances. But mortgage rates won’t increase as rapidly as the Fed funds rate, leading to a flatter yield curve. Indeed, mortgage rates remained broadly unchanged in 2017, and have risen only marginally since the Fed started raising rates in late 2015.

Mortgage rates compared to Fed Funds and 30yr USTs

Still space for increased housing investment

There are two key channels through which the housing affects the overall economy:

- The ‘wealth effect’: as house prices rise, household wealth increases which boost consumer spending. And second,

- Investment in new homes boosts employment directly in the construction sector and throughout the supply chain for building materials and construction-related services.

The wealth effect from the housing market is probably a bit less prominent than in the past. Lending against housing equity is, sensibly, more restrictive than before the financial crisis (when many Americans used borrowing against their home equity finance consumption). And the current pace of house price increases pales in comparison with recent gains in stock market values.

Residential investment has made a positive contribution to GDP growth since the housing market troughed in late 2011. But the increase in housing construction has been gradual and, as a share of GDP, it remains quite a bit below the historical average. That suggests there is space for a further pick-up in investment, which could help support economic growth in 2018.

Housing investment remains below historical average

Tax reform a potential snag

The tax bill Congress passed in December could impact the prospects for US housing in 2018. Among the changes to the US tax code are two important provisions that will affect the housing market:

- The mortgage interest deduction (MID), which allows homeowners to offset interest payments against their tax bill, has been limited to mortgages below $750,000 (from $1m previously), though only for new mortgages.

- The maximum amount of state and local tax (including property tax) deductible from federal taxes has been limited to $10,000.

Both these changes will affect the top-end of the market the most and will hit states and cities with relatively high taxes and/or property values (e.g. California and New York) particularly hard. That may limit price increases in those markets in the near term. Set against that, buyers at the high-end of the market are more likely to be high-income earners who will see the largest gains from the overall tax cuts, which may offset some of the negative impact on prices.

In addition, the tax bill increases the standard deduction to $24,000 for a couple and $12,000 for a single filer, which means fewer homeowners will file using itemized deductions (including MID). The effect is to reduce the tax incentives for homeownership since taxpayers using the standard deduction gain little tax advantage from owning a house rather than renting.

It is difficult to say how much this will affect demand for homes. Even without the tax advantage, homeownership is still likely to remain attractive both financially (as the value tends to appreciate over time) and psychologically (as it provides security of tenure and, for many, a sense of accomplishment).

Support for prices

Overall, the US housing market is on a positive trajectory and looks set to continue that way in 2018. Tight supply and robust momentum in the economy will support prices, though gently rising mortgage rates and the recent tax changes are likely to moderate price growth compared to 2017 and 2016. We expect construction to increase further, helping the economy towards another year of strong growth.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more