US fiscal package: Signed, sealed, delivered?

- 25 March 2020

A $2 trillion fiscal package has been agreed and will be voted on today. A clear positive development that the economy desperately needs, but with recession unavoidable the US fiscal position will deteriorate markedly. A deficit well in excess of 10% of GDP is inevitable this year… 20% is possible

Deal done

A deal has been reached between President Trump’s administration and Congress on a $2 trillion fiscal package. Equivalent to just under 10% of GDP, it dwarfs the Global Financial Crisis plan, which amounted to around $800bn. While final drafting is ongoing, a vote is expected today.

It contains measures that offer direct support to both households and businesses – focusing on efforts to incentivise businesses to keep workers on their payrolls and for those employees that do lose their job or have had hours cut, it provides better financial support. Unemployment insurance has been extended by 13 weeks that include four months of enhanced benefits with more workers covered.

Another major thrust is a cheque of $1200 for low and middle-income households. Anyone earning below $75,000 gets the full amount before it is phased out to zero for those earning more than $99,000. Families receiving this money would also qualify for an extra $500 per child.

Concessions were key

The main sticking point to getting a deal had been Democrats insisting on greater oversight as to who benefits and by how much and on what terms from the hundreds of billions of dollars available for loans and bailouts. There will now be an inspector general with a five-person Congress-appointed panel with rules stating that companies receiving support cannot implement any share buybacks during the period they benefit from government assistance. There would also be limits on executive remuneration during the period with steps needing to be taken to limit lay-offs while companies owned or run by the families of Donald Trump and Vice President Mike Pence would be barred from receiving support.

On top of this there would be another $130bn for hospitals and $150bn extra for state and local governments to help them deal with the healthcare crisis. There is also $350bn to fund a lending programme for small businesses set up in a way to incentivise keeping workers on the payroll.

Getting House approval

Unlike the Senate, the House is not in session and therefore a large proportion of members are not in Washington to participate in a vote. One option being considered is passing by “unanimous consent” whereby, assuming no objections, it would be written into law. However, that runs the clear risk that just one person could be unhappy with one small aspect of the bill and reject it, bringing down the entire legislation. Nonetheless with all sides, the White House, the Senate and the Democrat leadership in the House all happy, we expect it to pass.

Astonishing numbers

The economic data underlines the need for dramatic support for the economy. We know tomorrow’s initial jobless claims will be truly awful given the scale of lay-offs in the wake of city and state lockdowns that have shuttered countless businesses. We are forecasting a figure of two million people, but even this probably underrepresents the true picture given anecdotal news of jammed phone lines and crashed websites as people registered. Millions more will file in coming weeks.

Over the past 24 hours, we have seen business surveys collapse and mortgage applications plunge, which points to a sharp fall in housing activity in the months ahead. As such, not only is government spending surging, but tax revenues are plummeting and will continue to fall relative to the budget.

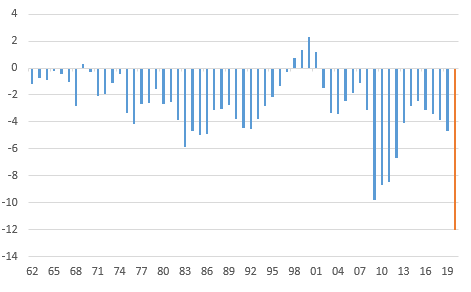

The US fiscal deficit and where we could be in 2020 (% of GDP)

The US fiscal deficit was already on course to top $1 trillion this year. We will be publishing updated global economic forecasts that will include different scenarios next week, but even in a best-case situation where President Trump gets his wish and we start to see the economy tentatively re-opening at some point in 2Q 2020, we will still likely have some form of social distancing and restrictions. Either way this means the economy still contracts sharply this year and implies a possible deficit in excess of $2.5 trillion.

In arguably the most benign case whereby the economy contracts around 3%, that still implies a fiscal deficit of around 12% of GDP. A deeper, more prolonged economic dislocation that requires significantly more fiscal support can quickly get you up to a fiscal deficit well in excess of 20% of GDP.

This truly is comparable with wartime. Unfortunately, the demographic situation will make lowering deficits and debt levels much more challenging relative to post World War 2, which raises questions as to what happens to all this debt? That is obviously not the focus while fires are being fought, but we will be addressing this in upcoming notes.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Covid-19 crisis: What you need to know

- This bundle contains 14 Articles