How far will the US Fed push back against market expectations?

With the US economy experiencing a Goldilocks period of firm growth and benign inflation, the focus this coming Wednesday will be on how far the Fed pushes back against the market view that they will be forced to cut rates later this year

Fed caution = market fear

Concern over global growth, a deterioration in financial conditions and a subdued inflation backdrop led the Federal Reserve to adopt a much more cautious stance at the start of the year. Those uncertain “cross-currents” prompted Fed officials to signal in March that the central bank can afford to be “patient” with no rate hikes in 2019 seen as the most likely scenario versus the two 25bp moves officials were anticipating back in December.

This much more dovish prognosis led to yield curve inversion (3M-10Y) with financial markets pricing in the prospect of interest rate cuts before the end of 2019. Indeed, even today futures' contracts imply a 60-70% chance of an interest rate cut before the end of the year despite Fed officials still pencilling in a 2020 rate hike. Consequently, the main focus of interest for Wednesday’s FOMC policy meeting will be how hard the Fed pushes back against market pricing in light of the recent more positive macro newsflow.

The market was too dismissive of a good performance

Since the March FOMC meeting, the economic outlook has undoubtedly improved. For instance, 1Q19 GDP growth came in significantly above expectations at 3.2% annualised versus 2.2% in 4Q18. The market, we think, was too dismissive of this good performance given the strong contributions from trade and inventories which may only be temporary in nature. As such we will be looking to see the Fed’s take and whether, as we believe, they will emphasise other data releases that have suggested the economy is in good shape. Indeed, the recent retail sales and durable goods orders figures suggest firm momentum that point to a much stronger consumer spending and investment story for 2Q19.

Since the March FOMC meeting, the economic outlook has undoubtedly improved

The corporate earnings season has also been a positive one, helping to push US equity prices to new highs, which will help confidence. Then there is the growing prospect of a US-China trade deal, that if signed can help lift more of the uncertainty hanging over the global economy. At the same time, the labour market looks resilient and wage growth is on an upward trend – we expect it to return to 3.4%YoY on Friday. These are all points the Fed could highlight as reasons for optimism.

The plunge in mortgage rates is helping to stimulate housing demand and construction spending is accelerating, with the prospect that residential investment could positively contribute to GDP growth for the first time in over a year. Credit conditions also don’t appear to have been impacted in a meaningful way from last year’s market volatility based on evidence within the Senior Loan Officer’s survey. Taking this all together, we continue to look for the US economy to expand by 2.4% over the full year.

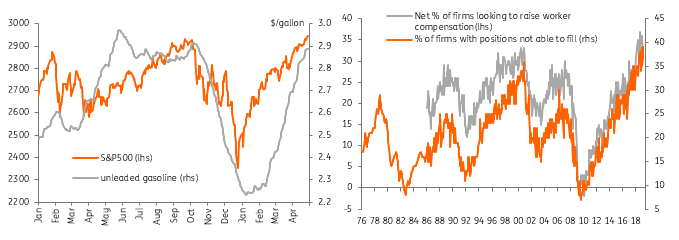

Equities, fuel and pay all on the rise

Inflation to grind higher too... so why cut rates?

We also expect inflation pressures to gradually build thanks to rising labour costs and improving corporate pricing power in an environment of firm demand. Rising oil prices will add to those inflation pressures with gasoline prices having jumped 30% from $2.23/gallon in mid-January to $2.89 today. This will also be felt in rising transportation and logistics prices. Consequently, we still look for core inflation numbers to move higher over the summer, especially with the pickup in wages.

Given this positive growth story, the improvement in financial conditions and the prospect of rising inflation we see little reason for the Federal Reserve to cut interest rates this year. This week’s FOMC meeting could see the Fed emphasise these points as it tries to reintroduce two-way risk into market pricing. The key question is will the market listen?

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more