US economy back on top

- 29 July 2021

- United States

2Q GDP growth of 6.5%, while disappointing, means that the US economy has now recovered all of the lost pandemic output and marks another key milestone in the recovery. The next target, given all the stimulus sloshing around, is to end the year with an economy larger in size than would have been the case had the pandemic not struck

| 6.5% |

(annualised 2Q21 GDP growth) |

Supply chain struggles hold back growth

Second quarter GDP growth has come in at 6.5% annualised, quite significantly below the 8.5% annualised consensus expectation. The positive is that this confirms that the level of real economic output is now back above the level of 4Q19 before the pandemic started, by 0.8 percentage points, and is a key milestone in the recovery process. Nonetheless, the core story is one whereby supply chain bottlenecks are holding back activity and creating inflation pressures with the PCE deflator rising at a 6.4% annualised rate with nominal GDP growing a remarkable 13%!

Inventory rundown and construction weakness offsets consumer strength

The US consumer continues to fire on all cylinders with personal consumer spending rising an annualised 11.8% rate.

The details show that the US consumer continues to fire on all cylinders with personal consumer spending rising an annualised 11.8% rate while non-residential fixed investment grew 8% as companies seek to expand to take advantage of the strong demand environment. However, residential investment contracted 9.8% as rising building material costs and a lack of workers stifled construction – although we saw better numbers toward the end of the quarter that point to a strong 3Q figure from this component.

The big drag was from inventories though, which subtracted 1.1 percentage points from growth while net exports subtracted a further 0.44ppt as robust consumer spending sucked in imports while ongoing pandemic weakness elsewhere in the world heard back exports. Government spending fell 1.5% after its recent surge.

Expectations have been pared back over recent weeks – we had, at one point, been looking for 10%+ growth – as it became increasingly evident that supply chain bottlenecks and labour market shortages have meant that the economy’s supply capacity has not been able to keep pace with demand. This explains the sharp rundown in inventories with the backlog of orders continuing to rise throughout the economy and supplier delivery times lengthen. In consequence, today’s output figure is much lower than it could have been, but we remain confident that the economy can catch-up again as the supply chain issues are rectified and capacity is rebuilt to cope with demand.

What pandemic???

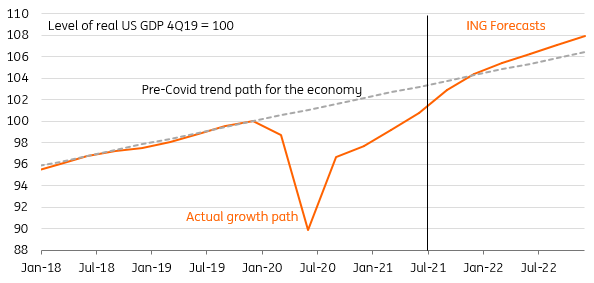

The next key milestone that we see is for the economy to overtake where it would have been had the pandemic not struck. The chart below shows the level of economic output (the orange line with our forecasts) versus the trend path of the US economy based on 2015-2019 GDP growth (the grey dotted line). We expect to see the blue line overtake the orange pre-Covid trend line in the fourth quarter of the year.

US GDP is back to pre-virus levels but remains below its pre-Covid trend

This would be a remarkable success story, but then again we have to remember that the Trump and Biden Administrations have thrown around $5tn of stimulus and support at the economy – equivalent to 20% of GDP – and the Fed has slashed rates to zero and continues to buy financial assets at an annualised rate of $1.44tn. More government spending is on its way with a $550bn infrastructure plan inching towards approval and President Biden’s social spending plan also showing signs of traction and these should provide ongoing economic momentum over several quarters.

Inflation pressures keep building

We see the Fed announcing a tapering of QE purchases in December 2021 and the first rate hikes coming in late 2022.

This situation is also inflationary. Costs have risen throughout the economy as re-opening frictions lead to bottlenecks and we see demand outpacing supply as an ongoing theme for at least the next few quarters. Given the strength of demand and the appetite for households and businesses to return to normal life, consumers appear prepared to pay more to experience things they haven’t done for many months. As such, corporate pricing power is on the rise and is a key reason why we think inflation at high levels is going to be long lasting than the Federal Reserve believes. It also explains why we expect a shift change in the Fed thinking through the second half of the year with a tapering announcement of QE purchases in December 2021 and the first rate hikes coming in late 2022.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more