US downturn delayed

- 6 July 2023

- United States

The US economy has proven to be more resilient than we expected, but the threat of recession lingers on due to lagged effects of rate hikes and tighter lending conditions while the restart of student loan repayments could come as a financial shock for millions of Americans. Inflation is subsiding and this will open the door to looser Fed policy next year

Upward revisions to near-term growth and Fed view

We have made major changes to our US forecasts this month, which see us revising up the near-term growth profile while also inserting a July Federal Reserve rate hike. Inflation is still set to slow sharply, but interest rate cuts, which we have long been expecting, are unlikely to happen before the end of this year.

We expected the economy to have been more impacted by the cumulative 500 basis points of interest rate hikes and a reduction in credit availability than it has been. Certainly, the banking stresses seen in March/April appear to have stabilised thanks to massive support for small and regional banks from the Federal Reserve. Employment creation has been robust, while residential construction has been stronger than expected despite the surge in mortgage rates. The lack of existing homes for sale is keeping prices elevated and is generating demand for new homes.

Inflation is slowing, but not quickly enough for the Federal Reserve and with the jobs market remaining firm officials are taking no chances. The Fed signalled that June’s decision to leave interest rates on hold should be seen merely as a slowing in the pace of rate hikes rather than an actual “pause”. Consequently, a 25bp July rate looks likely, but we doubt the Fed will carry through with the additional 25bp hike outlined in its latest forecasts.

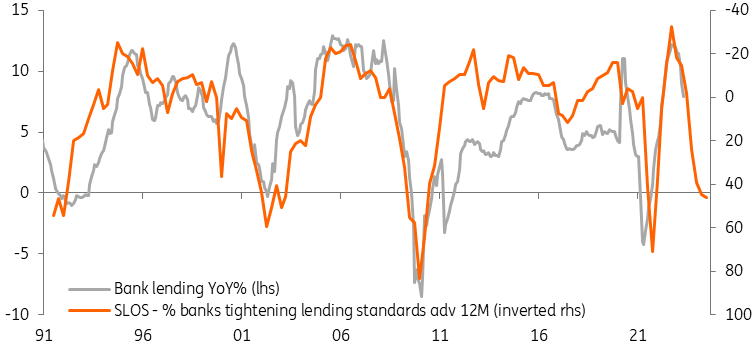

Bank nervousness points to a contraction in lending

Recession threat delayed, not averted

This all appears to tally with the Federal Reserve’s own soft landing thesis, but we still see a high probability of a recession. Lending growth is slowing with the Fed’s Senior Loan Officer survey suggesting it could turn negative before the end of this year. Business confidence remains in recession territory based on data from the Conference Board and the National Federation for Independent Businesses, and we know that monetary policy operates with lags with the full effects of higher interest rates yet to be felt.

A key reason that the economy has proved to be more resilient than we expected was consumers’ willingness to run down savings they had accumulated during the pandemic. We suspected they may choose to maintain larger savings buffers, while a $150bn surge in credit card borrowing since mid-2021, bringing the outstanding total to nearly $1tn, has additionally financed consumer largesse. But household savings and banks' willingness to lend are a dwindling finite resource and for many millions of Americans, the financial challenges are going to increase significantly over the next few months. That’s because as part of the deal to raise the US debt ceiling, the pandemic support for 43 million student loan borrowers has ended.

From 1 September, interest is once again being charged on $1.6tn of outstanding debt and from 1 October payments restart. With the Supreme Court throwing out President Biden’s plans to forgive up to $20,000 of an individual borrower’s debt this means that from the start of the fourth quarter around 30 million of those 43 million borrowers will have to find an average of $350 per month to cover the loans - current students don't pay while some other borrowers have defaulted or have deferred. That works out at around $130bn in aggregate for a year in interest and repayment, equivalent to around 0.75% of consumer spending.

Rate cuts are coming as inflation fears subside

With monetary policy set to get tighter, fiscal policy also becoming fractionally more restrictive, external demand looking weak and this student loan story set to hit quite hard, we are struggling to find a positive story that can offset these intensifying headwinds. As such, our narrative is one whereby recession has been delayed rather than averted.

Inflation looks set to continue slowing and we expect headline CPI to end the year below 3% with core inflation running close to 3.5%. The slowdown in housing costs is a key driver, but weakening corporate pricing power means we think even the Fed’s 'super core' measure of non-energy services excluding housing will be showing meaningful evidence of moderation.

We are also expecting the data discrepancies – for example, Gross Domestic Product pointing to growth yet Gross Domestic Income indicating recession, nonfarm payrolls rising yet household employment falling, ISM surveys pointing to falling output while official data points to rising output – to reconverge. Unfortunately, by the first quarter of 2024, we suspect it will be coalescing around the weaker trend. With inflation at or close to target by then, we argue this would justify the Fed moving policy to a more neutral setting, which means lower interest rates by quarter-end and through 2024.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: The economic twilight zone

- This bundle contains 13 Articles