US: Beware of the risks

- 5 December 2019

Financial markets remain in a positive mood, but with the headlines on trade looking less encouraging and the global backdrop and strong dollar acting as headwinds for growth, we are less sanguine on the economic outlook. We continue to forecast sub-consensus growth of 1.4% and expect the Federal Reserve to cut rates twice more in the first half of 2020

Markets accentuate the positive

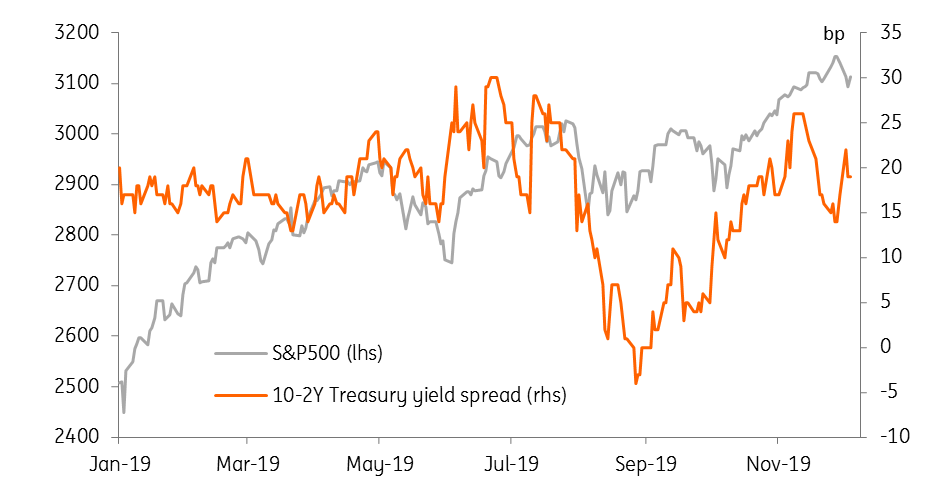

Just four months ago equities were selling off, the yield curve was inverted - historically a strong predictor of recession - and activity data was starting to soften. Since then we have had three interest rate cuts from the Federal Reserve totalling 75 basis points and there has been talk of a phase one trade deal with China. With the economic data seemingly having stabilised we have seen a major turnaround in market sentiment with the yield curve re-steepening and equities rising more than 10% from those August lows.

There has been a shift in sentiment at the Federal Reserve too, with officials suggesting that after their “insurance” policy easing, the economy is in a good place and they are happy to wait and see the effects of those rate cuts in July, September and October. The market agrees, pricing in just one more rate cut in this cycle (and not until late 2020).

US equities versus the 10-2Y yield curve

But we can't eliminate the negative...

We are less sanguine. Instead, we see significant threats to this narrative and prefer to stay on the softer side of consensus, predicting 2020 GDP growth of 1.4% versus the 1.8% the market expects. We also see the risks skewed towards two further 25bp interest rate cuts in the first half of 2020. After all, global activity remains subdued, inflation is benign and the latest news on trade is hardly encouraging, so we struggle to see where meaningful upside momentum is going to materialise from.

Regarding trade policy, via a tweet, President Trump promised to restore tariffs on steel and aluminium imports from Brazil and Argentina in response to his perception that they have generated “massive depreciation of their currencies, which is not good for our farmers”. At the same time tensions are escalating with France and the EU. The US has threatened tariffs on $2.4 billion of French exports to the US in retaliation for a digital tax imposed by France (replicated elsewhere) that is primarily raising revenues from American tech companies.

Additionally, the prospects for a phase one trade deal with China, which was initially announced all the way back in October, are looking less positive. President Trump suggested that he has no deadline and would be prepared to wait until after the 2020 election. This implies a diminished prospect that some of the already enacted tariffs will be rolled back and raises the threat that another wave of 15% tariffs on $156 billion of consumer goods from China will go ahead as scheduled on 15 December. With China likely to respond in kind, trade looks set to remain a major headwind for growth in 2020 by disrupting supply chains, hurting profitability and damaging sentiment.

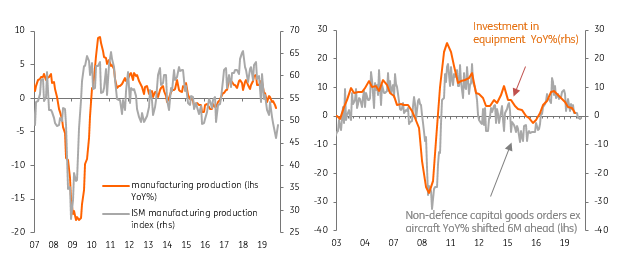

Industrial output and capex continue to weaken

Slowdown set to continue, but recession avoided

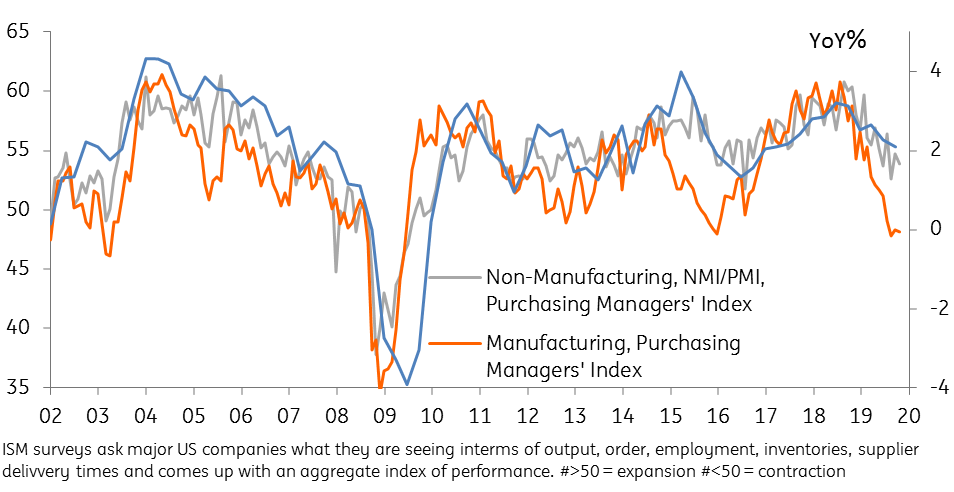

Domestically, the economy’s growth rate is slowing. Payrolls growth that averaged 233,000 per month in 2018 is now averaging 168,000 while the ISM manufacturing index has been in contraction for four consecutive months. Moreover, the production sub-component is at levels consistent with output falling 5% year-on-year.

Capital expenditure fell in both 2Q and 3Q with lead surveys, such as the durable goods report, suggesting a third consecutive contraction in the fourth quarter. With trade worries set to linger and firms seemingly willing to “wait and see” given divergent political policies and priorities of the respective presidential candidates, we are doubtful of a major rebound in capex in 2020.

There has also been evidence of a slowing in service sector output and in consumer spending despite confidence holding up relatively firmly. Retail sales have been disappointing in recent months with auto sales also looking like they have peaked. This may be temporary, but with the economic news looking subdued, politics remaining divisive and mortgage rates on the rise again the outlook is, at best, uncertain. Consequently, we suspect 4Q GDP and 1Q 2020 GDP will come in below the 2.1% rate of 3Q19, especially if firms begin to run down some of the inventories they have built up in recent quarters.

ISM business surveys point to GDP slowdown

Downside risks for interest rates

With the inflation backdrop looking benign, the Federal Reserve is able to offer more support to the economy with a couple more interest rate cuts. Recent comments suggest a strong reluctance at present, but with the trade backdrop looking less favourable, the key ISM series on a downward trend and the global backdrop and strong dollar hurting export performance and business confidence, we think they will. It is probably going to be later than we had previously been thinking, straddling 1Q and 2Q 2020 rather than concentrated in 1Q. We also see downward risk for longer-dated Treasury yields, targeting 1.40% for the 10-year yield in the first half of next year.

Election uncertainty continues

In terms of politics, the impeachment process against the President is gaining pace with the House of Representatives having published its report which concluded that Trump had abused his position to pursue “personal and political interest above the national interests of the US” in regard to dealings with Ukraine. The Democrat-controlled House looks set to vote in favour of impeachment, which will lead to a trial in the Senate. Nonetheless, with 20 Republican Senators required to vote in favour to get a two-thirds majority for conviction this looks highly unlikely given none have hinted at voting in favour so far. As such Donald Trump will get to stand for re-election.

The field of Democrat candidates remains sizeable with fifteen still in the race. In terms of noted names, early front runner Kamala Harris has dropped out while former New York mayor Michael Bloomberg has entered the fray. Former Vice President Joe Biden remains the lead, but he is closely followed by the more progressive (and interventionist) Elizabeth Warren and Bernie Sanders, according to recent polling.

Opinion polling suggests the election will be close, but that a centrist Democrat is more likely to defeat President Trump than a progressive. If this is the case we will likely see more emphasis on infrastructure spending versus tax cuts from Trump as the key policy thrust, with more regulatory oversight of tech industries and a focus on greener energy to boot. Another four years under Donald Trump would likely result in broader use of tariffs as a tool for generating trade “wins”. Under a centrist Democrat, we suspect that the US would be prepared to work more closely with Europe to get a re-orientated global trade policy with less emphasis on tariffs as the starting point. Please click on this link for a collection of our latest views on US politics.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

December Economic Update:Prepare to be disappointed in 2020

- This bundle contains 9 Articles