US: a cold wind is blowing

This has been a disappointing year for the US economy with two consecutive quarters of falling output. It will be worse in 2023. Consumer spending and business capital expenditure look set to fall and unemployment will rise in response to the rapidly tightening financial conditions caused by dollar strength, rising rates and widening credit spreads

Tougher conditions ahead for consumers and businesses

The Federal Reserve’s delayed response to the obvious inflation threat means it is playing catch-up and raising interest rates faster than at any time since the late 1980s. This is contributing to considerable dollar strength while prompting rapid rises in borrowing costs throughout the economy. This significant tightening of financial conditions is a clear headwind to growth and comes at a time when consumer and business confidence is already under immense pressure from the rising cost of living and falling equity, bond and real estate prices.

Housing market set for sustained weakness

Unfortunately, our worst fears about falling transactions and the prospect of sharp price falls in the US residential property market appear to be coming true. Mortgage rates have doubled since the start of the year leading to a 44% collapse in mortgage applications for home purchases while the supply of new and existing homes is up 64% and 50% from their respective lows.

Ratio of US existing home prices to median household income ratios (1999-2022)

This rapidly changing dynamic means the 45% jump in home prices since the start of the pandemic looks unsustainable. After all, the median house price-to-income ratio is more stretched than at the peak of the 2005/06 housing bubble. Consequently, July’s first monthly price fall in more than 10 years looks set to be the start of many with even Fed Chair Jerome Powell publicly acknowledging the need for a correction. This will be bad news for construction activity as well as spending on furniture, furnishings, electronics and building supplies.

Labour market shows signs of softening

Consumer weakness is already spreading beyond the property market. We had hoped the plunge in gasoline prices would free up cash that would translate into stronger consumer activity elsewhere. There was a temporary lift to restaurant dining numbers, air passenger traffic and google mobility data, but it hasn’t shown up in consumer spending more broadly.

On top of this, we are seeing a growing number of firms freeze hiring plans with job vacancies falling by more than one million in August. The one consolation is that most firms are experiencing labour shortages so there will be a reluctance to fire staff. The Fed is predicting a 0.9ppt rise in the unemployment rate over the next year, which would work out as 1.2 million people losing their jobs assuming the labour supply remains unchanged.

Inflation will soon turn lower

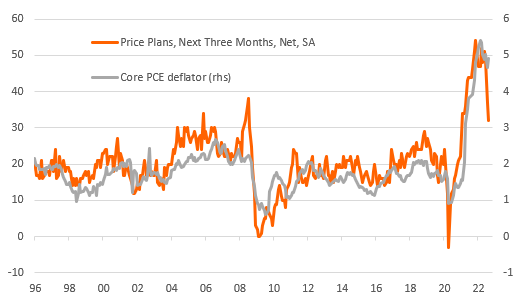

While core inflation rates have been moving higher recently, we are increasingly confident in our call that we could see inflation head towards 2% by the end of 2023 as recessionary forces erode corporate pricing power. The chart below of the National Federation of Independent Businesses’ price plan series is already offering very encouraging news for a potential slowdown in US inflation with fewer firms anticipating price hikes due to weakening sales growth and rising inventories.

Corporate pricing power appears to be weakening: NFIB price plans and the core PCE deflator inflation measure

Moreover, weightings for shelter costs and vehicle prices are far, far higher in the US inflation calculation than in Europe – a combined 40% for the US basket of goods and services versus 12% for Europe. With the US housing rent components lagging house price changes by around 12-14 months, we expect to see shelter go from contributing more than 2ppt to the headline inflation rate to contributing nothing next year. Meanwhile, auction prices for used cars are down 15% from their peak and are set to fall sharply as the supply of new vehicles ramps up now as supply chain strains are easing.

Fed rate hikes to give way to cuts in the second half of 2023

We are forecasting that the Federal Reserve will raise the policy rate by another 75bp in November, but the intensifying economic headwinds look set to result in a more modest 50bp hike in December which will mark the peak at 4.25-4.5%. This would mean real interest rates turning positive in the second quarter based on our inflation forecast – a key metric that the Fed wants to achieve.

Once the Fed has hit the pause button on rate hikes the market will swiftly move to anticipate rate cuts. We expect them to start coming through from the third quarter of 2023 as the Fed seeks to prevent a more prolonged downturn that could result in inflation falling well below 2% over the medium term. Robust household balance sheets and a still-tight labour market offer hope that once lower borrowing costs materialise and risk assets stabilise, the recovery can come relatively quickly and vigorously.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

6 October 2022

ING’s October Monthly: bracing for a tough winter This bundle contains 14 Articles