UK’s energy cap U-turn risks higher inflation and deeper recession

- 18 October 2022

- United Kingdom

The UK government has announced it will make its energy price cap less generous from April next year. That could add 3pp to inflation for much of 2023, and depending on how the changes are made, could deepen the recession we're forecasting this winter. We now expect a 'smaller' 75bp rate hike from the Bank of England in November

The UK Chancellor has reversed much of the ill-fated growth plan

UK bond markets reacted well to new Chancellor Jeremy Hunt’s announcement that large parts of the so-called "mini" Budget will be reversed. That said, there is undoubtedly further work to be done. For debt to fall as a share of GDP, the government needs to find £72bn a year by 2026/27, according to leaked reports from the Office for Budget Responsibility over the weekend. Recent U-turns have roughly halved that shortfall.

That inevitably leaves more to be announced by the time of the 31 October Medium-Term Fiscal Plan. We expect a revenue cap on renewable energy generators, and cuts to public sector investment, to do some of the leg work (we wrote more on the different options yesterday). The Chancellor will also hope the fall in Gilt yields will enable the OBR to lower its estimate of future debt-servicing costs.

But by far the most consequential announcement for the UK economy on Monday was that the government’s energy price guarantee will change from next April. At present, this guarantee has fixed consumer gas/electric unit prices such that the average household’s annual bill is capped at £2500 for the next two years. The Chancellor has signalled that will no longer be the case from April, and instead will become more targeted.

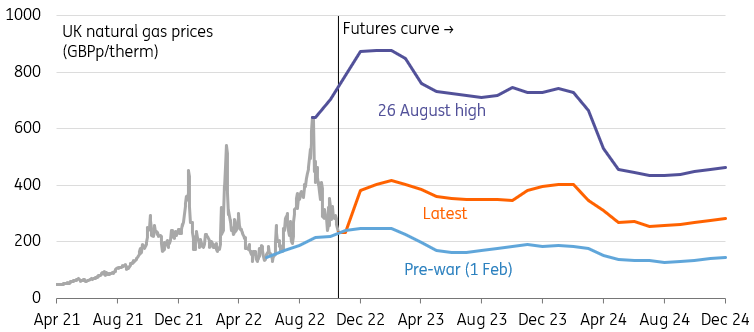

The government is getting a helping hand from a plunge in gas prices

The fact that the energy guarantee currently applies equally to all households does suggest some room to make the policy more targeted, though in practice that’s complicated. Any policy needs to recognise a) that energy usage doesn’t vary hugely across the income spectrum, but b) it does vary considerably within different income brackets (owing to varying household sizes).

At present, the government only really has two ways to means-test its energy price cap. The most obvious option is to offer all households the same energy price but to temporarily raise higher rates of income tax to make the system fairer. That would probably be the most accurate and therefore cost-effective option, but would most likely be politically untenable. The alternative would simply differentiate between those on Universal Credit (welfare benefits) - around 15-20% of energy-using households - and those that aren’t. This is effectively what former Chancellor Rishi Sunak did before the summer.

Barring the Treasury finding a more innovative solution, this option could conceivably see most households move back onto the price set quarterly by the regulator Ofgem from April 2023. Using current gas/electricity futures prices, we estimate that the average household electricity bill would total £3700 in fiscal year 2023, peaking at £4250 on an annualised basis between April and June next year.

The cost of the energy price guarantee has more than halved

This could save the Treasury roughly £25bn in FY2023 and a further £6bn in FY2024, if we make the simple assumption that those on Universal Credit continue to have their bills fixed for the full two years. If that doesn’t sound like that much, it’s because gas prices have fallen considerably in recent weeks. By our estimates, the cost of the household energy cap has more than halved since its inception.

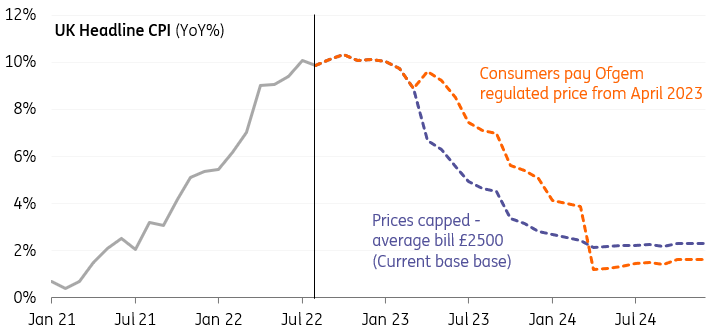

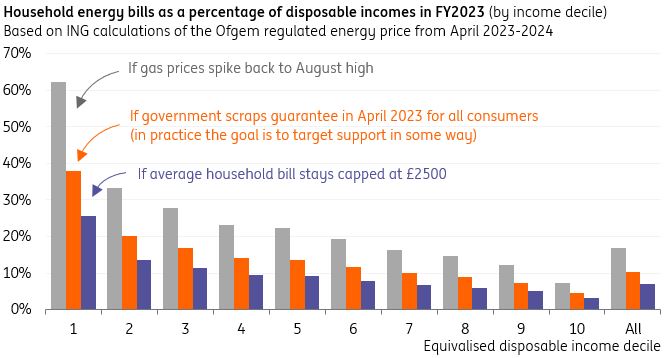

Of course, this sort of policy would inevitably come at a cost to both growth and inflation. The chart below shows that inflation would be roughly 3 percentage points higher through much of 2023 if energy prices revert to those set by the regulator Ofgem. Households across the income spectrum would in most cases be spending close to, or in excess of, 10% of their disposable incomes on energy bills in FY2023. That would be 15%+ if energy prices were to return to their August high – and it’s worth saying that our Commodities team forecasts gas prices to end up higher next winter than during the coming one.

Inflation could be 3pp higher through much of 2023 if most households revert back to the Ofgem price

That kind of hit to disposable incomes would inevitably deepen what would otherwise hopefully be a reasonably mild recession this winter. The Chancellor will be hoping that energy prices continue to fall, lessening the blow to households. Indeed for now his focus is on reducing the OBR’s borrowing estimates as much as possible in its forecast due on 31 October. He’ll also be hoping a scaled-back support package will reduce the need for the Bank of England to tighten aggressively.

But in practice – and especially if gas prices start rising again – we think the Treasury may well need to offer extra support in one form or another before April next year.

Households could spend around 10% of disposable income on energy without the government guarantee

Fiscal U-turns give Bank of England a route to less aggressive tightening

For the time being though, the moves by the Chancellor will reduce the need for the Bank of England to act as aggressively. Having pencilled in a 100 basis-point rate hike in November, we now think that’s more likely to be 75bp.

Markets are still expecting Bank Rate to peak at 5.2% next summer, albeit this pricing has been pared back since the fiscal U-turns. This leaves the Bank with a difficult decision: meet those expectations, and bake in what are now very uncomfortable mortgage and corporate borrowing rates. Undershoot investor expectations, and the pound could fall materially.

But in practice a weaker pound – and the extra imported inflation that might bring – is probably more desirable than the current strains that are starting to emerge as a result of ultra-high borrowing costs. The challenge for policymakers will be to gradually talk down market rate expectations without causing abrupt pressure on the currency. Ultimately, we think a 75bp hike in November will be followed by another 50-75bp hike in December. We think Bank Rate will peak somewhere between 3.5-4%.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more