UK: What Brexit means for the economy in 2021

We think it's unrealistic to expect a sudden plunge in GDP once the transition period ends. But whether there's a deal or not, the change in UK-EU trade terms will push costs up for businesses in a range of sectors, potentially compounding the Covid-19 hit. That leaves the UK at risk of a slower and more turbulent recovery relative to its peers

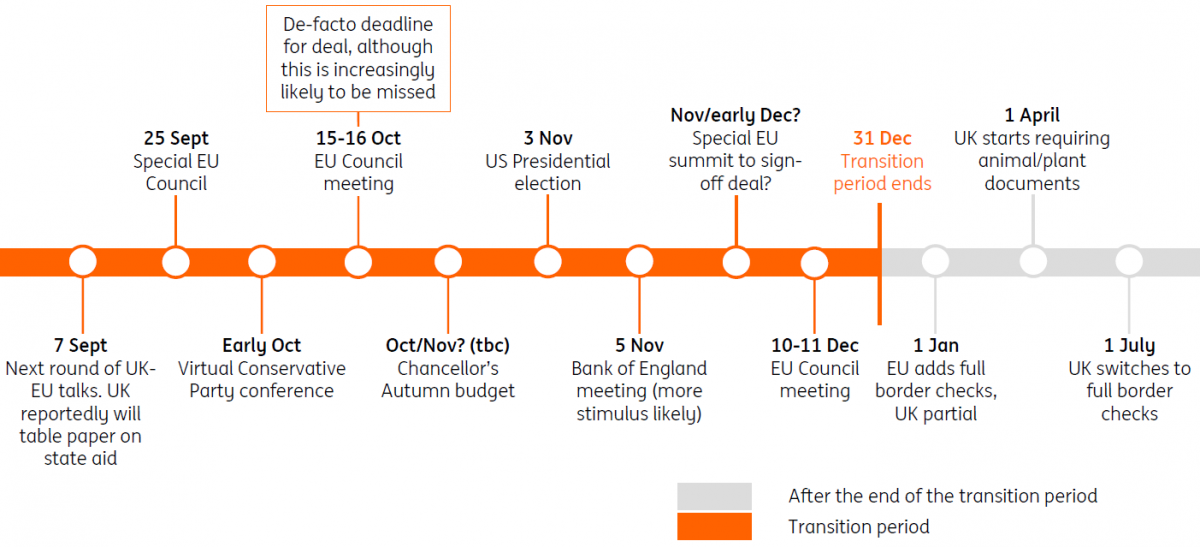

Time is running out on trade talks

There are now less than four months to go until the end of the post-Brexit transition period, and with negotiations stuck in deadlock, there are renewed fears that there won’t be a trade agreement in place to replace it. The de-facto October deadline for negotiations to be wrapped up looks increasingly likely to be missed.

But what does all of this mean in practice for the economic outlook in 2021?

The latest Brexit timeline

A sudden plunge in GDP next year seems unlikely

A common hypothesis is that we should expect a sharp and sudden drop in GDP in early 2021. After all, even with a free-trade agreement (FTA) in place, the change in UK-EU trade terms will be significant.

For that to happen though, we’d need to see a plunge in consumer spending, which makes up almost two-thirds of the UK economy. This currently seems unlikely. Evidence from the Brexit deadlines in 2019 suggested consumers were unfazed by the prospect of 'no-deal', and unlike businesses, there wasn’t much evidence of stockpiling. Toilet rolls remained in plentiful supply, anyway.

Instead, the path for spending over the winter will be much more heavily determined by developments in the jobs market, and of course how the government’s support package evolves once the furlough scheme ends in October.

Costs will go up for businesses, and that'll keep the brakes on the recovery

That’s not to say there will be no impact once the transition period ends, and we don’t think it’s true to say that the enormity of the Covid-19 hit will make the Brexit effect indiscernible.

Firms will see their costs rise once the transition period ends, and this has the potential to compound the damage already done by the pandemic. These new costs are not necessarily the same as those already being incurred as a result of Covid-19.

Take the car industry, where production fell by 70% during the second quarter. Cars make up 7% of UK exports to the EU and would face a 10% tariff if there’s no free-trade agreement in place this year. Even if there is a deal, it seems reasonable to expect some initial disruption at the ports, and that’s likely to raise transport costs and slow down production. Companies could raise stockpiles again to compensate, but with cashflows already under heavy pressure as a result of the pandemic, and warehousing space increasingly occupied ahead of Christmas, this is likely to be a very unattractive option.

The switch to new UK-EU trade terms will also hit several sectors that have been among the least affected by Covid-19. Agricultural production slipped by less than 5% during the second quarter, but is the most vulnerable sector to tariffs, often in excess of 30%. The sector will also be among the most impacted by new border-related bureaucracy, with spot checks disproportionately focused on animal and plant certification.

A deal would reduce some, but not all, of the burden

The agreement of a trade deal would admittedly ease (but not eliminate) some of these new frictions. And despite the current standstill in negotiations, we think that a basic FTA is still narrowly the most likely scenario this autumn.

If that’s the case, tariffs would be avoided (although firms would still need to prove the origin of the product to qualify). Both sides might also agree to reduce the frequency of health checks on animal/plant products at the border, and could also look at introducing trusted-trader schemes, all of which could help reduce some of the pressure on the ports.

Despite the current standstill in negotiations, we think that a basic FTA is still narrowly the most likely scenario this autumn

And while a trade deal won't do much for services, it probably raises the chance of an EU decision on financial equivalence and data sharing.

There’s also still a lingering chance that a deal would unlock some form of additional, bare-bones transition period to help businesses adapt. This would be much more basic than the current environment and would be more legally-complex and time-consuming to agree. But an agreement to, say, allow the UK to remain in a customs union for an extended period, in exchange for budget payments, would potentially ease some of the initial bureaucratic burdens on firms. This could be particularly beneficial for UK traders sending goods to the EU (the UK government is already planning some unilateral steps to stagger the initial changes for importers).

How likely is some form of additional transition, or 'off-ramp' as some are calling it? The jury's still out on that one.

Expect more stimulus from the Bank of England

Still, the key point is that, with or without a deal, the bureaucratic and cost burden on firms will be materially higher next year.

So while we’re unlikely to see a sudden hit to GDP from Brexit in the early stages of next year, the additional strain on firms will inevitably put the brakes on the overall post-Covid recovery. The consequence may be that the spike in unemployment we’re likely to see (potentially 8-9% by year-end) persists for longer, and broadens out to a wider range of sectors than might have otherwise been the case.

For the Bank of England, this is just another reason to expect a further round of stimulus in November. We suspect this will involve more quantitative easing, but the jury is still out on negative rates. We think policymakers might initially be more inclined to adjust the interest rate on the term-funding scheme (designed to encourage lending to small businesses) as a first step.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

3 September 2020

Covid-19: The virus, the vaccine and what next for the global economy? This bundle contains 10 Articles